Margin Considerations for IB LLC Commodities Accounts

Introduction

As a global broker offering futures trading in 19 countries, IB is subject to various regulations, some of which retain the concept of margin as a single, end of day computation as opposed to the continuous, real-time computations IB performs. To satisfy commodity regulatory requirements and manage economic exposure in a pragmatic fashion, two margin computations are performed at the market close, both which must be met to remain fully margin compliant. An overview of these computations is outlined below.

Overview

All orders are subject to an initial margin check prior to execution and continuous maintenance margin checks thereafter. As certain products may be offered intraday margin at rates less than the exchange minimum and to ensure end of day margin compliance overall, IB will generally liquidate positions prior to the close rather than issue a margin call. If, however, an account remains non-compliant at the close, our practice is to issue a margin call, restrict the account to margin reducing transactions and liquidate positions by the close of the 3rd business day if the initial requirement has not then been satisfied.

In determining whether a margin call is required, IB performs both a real-time and regulatory computation, which in certain circumstances, can generate different results:

Real-Time: under this method, initial margin is computed using positions and prices collected at a common point in time, regardless of a product’s listing exchange and official closing time; an approach we believe appropriate given the near continuous trading offered by most exchanges.

Regulatory: under this method, initial margin is computed using positions and prices collected at the official close of regular trading hours for each individual exchange. So, for example, a client trading futures listed on each of the Hong Kong, EUREX and CME exchanges would have a requirement calculated based upon information collected at the close of each respective exchange.

Impact

Clients trading futures listed within a single country and session are not expected to be impacted. Clients trading both the daytime and after hours sessions of a given exchange or on exchanges located in different countries where the closing times don’t align are more likely to be impacted. For example, a client opening a futures contract during the Hong Kong daytime session and closing it during U.S. hours, would have only the opening position considered for purposes of determining the margin requirement. This implies a different margin requirement and a possible margin call under the revised computation that may not have existed under the current. An example of this is provided in the chart below.

Example

This example attempts to demonstrate how a client trading futures in both the Asia and U.S. timezones would be impacted were that client to trade in an extended hours trading session (i.e., outside of the regular trading hours after which the day's official close had been determined). Here, the client opens a position during the Hong Kong regular hours trading session, closes it during the extended hours session, thereby freeing up equity to open a position in the U.S. regular hours session. For purposes of illustration, a $1,000 trading loss is assumed. This example illustrates that the regulatory end of day computation may not recognize margin reducing trades conducted after the official close, thereby generating an initial margin call.

| Day | Time (ET) | Event |

Start Position |

End Position | IB Margin | Regulatory Margin | |||

| Equity With Loan | Maintenance | Initial | Overnight | Margin Call | |||||

| 1 | 22:00 | Buy 1 HHI.HK | None | Long 1 HHI.HK | $10,000 | $3,594 | $4,493 | N/A | N/A |

| 2 | 04:30 | Official HK Close | Long 1 HHI.HK | Long 1 HHI.HK | $10,000 | $7,942 | $9,927 | $4,493 | N/A |

| 2 | 08:00 | Sell 1 HHI.HK | Long 1 HHI.HK | None | $9,000 | $0 | $0 | $0 | N/A |

| 2 | 10:00 | Buy 1 ES | None | Long 1 ES | $9,000 | $2,942 | $3,677 | N/A | N/A |

| 2 | 17:00 | Official U.S. Close | Long 1 ES | Long 1 ES | $9,000 | $5,884 | $7,355 | $9,993 | Yes |

| 3 | 17:00 | Official U.S. Close | Long 1 ES | Long 1 ES | $9,000 | $5,884 | $7,355 | $5,500 | No |

注文のプレビュー / 証拠金の確認

概観:

注文のプレビュー/証拠金の確認機能を利用して予想されるコストや手数料、また証拠金への影響を、注文発注前に確認することができます。 この機能はTWSとウェブ・トレーダーの両方からご利用可能ですが、TWSバージョンの方がより細かい詳細を含んでいます。

トレーダー・ワークステーション(TWS)

TWSの証拠金確認機能を利用すると、計画中の注文による証拠金への影響を既存のポジションから分離することができ、また注文が約定された場合の新しい必要証拠金を確認することができます。委託証拠金および維持証拠金の必要額を含める証拠金の残高を表示し、流動性資産価値としてレポートします。この機能を利用するには注文のラインにカーソルをあて、右クリックしてドロップダウンのメニューから証拠金確認を選択してください。

例: 2012年6月が限月のES先物を1枚1387.25にて購入

注文プレビューの最初の項目にはこの有価証券のビッド、アスクそして最終取引価格が表示されます。

2つ目の項目には注文の基本的な内容が表示されます。

金額の項目には注文の価値と手数料の見積もりが表示されます。

証拠金への影響の項目には、下記の内訳が表示されます;

現在 = この注文の発注を除いた状態での、現在の口座価値

変化 = 口座内にあるポジションはすべて無視した状態で、この注文が発注された場合の影響

取引後 = 発注された注文が約定し、口座のポートフォリオに組み込まれた後に予想される口座価値

WebTrader

WebTraderの注文プレビュー機能には、TWSで取引後の口座価値として表示される情報のみが表示されます。

弊社からの資金借り入れ状況の判別方法

口座の現金残高の合計がマイナスになる場合には資金を借りることになり、借入は利子の対象となります。 借入は合計の現金残高がプラスの場合にも残高の清算やタイミングによっては存在することがあります。 下記はこういったケースの最もよくある例になります:

1. ロング対ショートの通貨バランス – ある通貨建ての現金を、別の通貨の残高で用立てることができる場合です。 例えば米ドルを基準通貨とする口座が、ロングで決済済みUSD 10,000の残高、ショートで決済済みEUR 5,000の残高を、ユーロと米ドルの為替レート1.38:1で保有しているとします。ここではステートメントの報告および金利計算の観点より、全体的な現金残高はUSD 3,088(10,000 –(5,000 x 1.38))になります。 資金調達や再投資に関し各通貨にはそれぞれの取り決めがあるため、ショートの残高は適用されるベンチマーク・レートや段階に基づく資金調達コストの対象となり、このコストはロングの残高に適用されるベンチマーク・レートや段階に基づいて受け取る金利に相殺されることがあります。

2. セグメントごとの総残高 – IBKRのユニバーサル口座には複数のサブ口座やセグメントが含まれ、これらには規制や顧客保護のためそれぞれのポジションおよび担保があり、合わせての運用はありません。 この分離によりすべてのセグメントからの残高を合計することはないため、あるセグメントの残高でその他のセグメントの残高の負債を相殺することはありません。 例えば、IBLLC口座に有価証券とコモディティのポジションがあり、このうちの有価証券のセグメントにはUSD 3,000の負債があり、コモディティのセグメントにはUSD 8,000の残高があるとします。両方の口座の残高を合わせるとプラスUSD 5,000になり、不足分の残高には金利が発生しますが、プラスの残高につく金利によって部分的な相殺の可能性があります。

3. 空売り – 空売りは証拠金による取引であり、口座名義人は現金ではなく株式を借入れします。 空売りからの利益は口座の現金残高になりますが、株式の貸し手に対して株の返却を保証するため、こういった資金は担保として扱われます。この結果および借入取引が独自の融資取り決めの対象となる事実を踏まえ、証拠金の借入があることを明確にするために、借入の担保となる現金は残高とみなされません。

例として、現金残高は4,000、ロングの株式価値が10,000、およびショートの株式価値が5,000の、流動性総資産(残高はすべてUSD)は9,000になる口座を見てみます。株式のロングポジションが借入によるものであるかどうかを明確にするため、株式の貸し手に対し担保になっている5,000分が4,000の現金残高から差し引かれ、結果として1,000の負債になります。 この負債は金利の対象となり、また借入困難な株式の借入に対する現金は金利の対象、または借入がしやすく再投資レートが十分に高い株式の借り入れに対する現金は空売り株リベートの対象になる可能性があります。

4. 未決済資金- 借入は決済済みの資金に基づいて決定され、特定の取引に対する支払いや受け取り期限の時間枠は商品によって異なります。(通常、株式は3営業日、スポット通貨は2営業日、またデリバティブは1営業日以内の決済になります) ステートメントおよび取引プラットフォーム上の理由により、現金残高の報告は決済日ではなく取引日に基づくものとなり、決済が完了したように扱われます。

この結果、残高のあるように見える口座が未決済の借入資金で購入された株式の売却からの収益を含んでおり、実は証拠金の借入を保有している可能性もあります。 同様に、取引日に基づく負債残高のある口座が 、取引がまだ決済されていないために証拠金の借入および金利の負担をしていないという可能性もあります。

金利の計算に関しての詳細は金利の計算方法をご参照ください。

IB発行株式CFDに関する概要

以下の記事はIB発行の株式ベースの差金決済取引(CFD)に関する概略をご提供することを目的としています。

IB株価指数CFDに関する情報はこちらをクリックしてください。Forex CFDに関する情報はこちらをクリックしてください。

ここでは以下のトピックを取り上げます:

I. CFDの定義

II. CFDと原資産株式の比較

III. 費用および証拠金に関する留意点

IV. 例

V. CFDのリソース

VI. よくあるご質問

リスク警告

CFDはレバレッジによる損失のリスクが高い複雑な商品です。

62%の個人投資家口座に、IBKR(UK)とのCFD取引による損失が発生しています。

お取引を開始される前に、CFDの機能の仕方および損失の際のリスクをご理解ください。

CFDに関わるESMAルール(リテールクライアントのみ)

欧州証券市場監督局(ESMA)は2018年8月1日より有効となるCFDルールを実施しました。

ルールには以下が含まれます: 1) CFDのポジションを建てるにあたってレバレッジの上限; 2) 口座ごとの証拠金解約; および 3) マイナス残高に対する口座ごとの保護。

ESMAによる決定はリテールクライアントのみに適用されます。特定投資家のお客様への影響はありません。

詳細はIBKRにおけるESMA CFDルールの実施をご参照ください。

I. 株式CFDの定義

IB CFDは配当およびコーポレートアクション(CFDコーポレートアクションに関する詳細)を含む、原資産株式のリターンを生むOTC取引です。

これは言い方を変えれば、株式の現在と将来の価値の差額を交換するという、購入者(お客様)と弊社間における合意になります。お客様がロングポジションを保有し差額がプラスの場合には、弊社がお客様にお支払します。差額がマイナスの場合にはお客様にお支払いただくことになります。

IB株式CFD取引は証拠金口座を通して行われるため、ロングおよびショートのレバレッジ・ポジションを建てることができます。CFD価格は原資産株式の取引所クオート価格になります。実際にIB CFDクオートは、トレーダー・ワークステーションで見ることのできる株式用のスマートルーティング・クオートと同じであり、IBではダイレクト・マーケット・アクセス(DMA)をご提供しております。株式同様に、成行とならない(指値の)注文の原資産ヘッジは、取引されている取引所の 板画面に直接表示されています。 これはまたCFDを原資産のビッド価格で購入しオファー価格で売る注文の発注ができるということになります。

弊社の透明性のあるCFDモデルをマーケット上にある他社のものと比較される場合にはCFDマーケットモデルの概要をご覧ください。

IBでは現在、米国、ヨーロッパおよびアジアの主なマーケットをカバーする約6500の株式CFDご提供しております。 下記にリストされている主要指数の構成銘柄は、現在IB株式CFDとしてご利用可能です。IBではまた多くの国で流動小型株の取引もご提供しております。これは最低5億米ドルの時価総額の浮動株を持ち、また平均最低60万米ドルに値する日次の取引を行う株式です。 詳細はCFD商品リストをご覧ください。ご利用可能国は近い将来、さらに追加される予定です。

| 米国 | S&P 500, DJA, Nasdaq 100, S&P 400(中型株), 流動小型株 |

| イギリス | FTSE 350 + 流動小型株 (IOBを含む) |

| ドイツ | Dax, MDax, TecDax + 流動小型株 |

| スイス | Swiss portion of STOXX Europe 600 (48 shares) + 流動小型株 |

| フランス | CAC Large Cap, CAC 中型株 + 流動小型株 |

| オランダ | AEX, AMS 中型株 + 流動小型株 |

| ベルギー | BEL 20, BEL 中型株 + 流動小型株 |

| スペイン | IBEX 35 + 流動小型株 |

| ポルトガル | PSI 20 |

| スウェーデン | OMX Stockholm 30 + 流動小型株 |

| フィンランド | OMX Helsinki 25 + 流動小型株 |

| デンマーク | OMX Copenhagen 30 + 流動小型株 |

| ノルウェー | OBX |

| チェコ | PX |

| 日本 | Nikkei 225 + 流動小型株 |

| 香港 | HSI + 流動小型株 |

| オーストラリア | ASX 200 + 流動小型株 |

| シンガポール* | STI + 流動小型株 |

| 南アフリカ | トップ40 + 流動小型株 |

*シンガポール居住者にはご利用いただけません

II. CFDと原資産株式の比較

お客様の取引目標と取引スタイルにより、株式に比べてCFD取引にはメリットもあればデメリットもあります:

| IB CFDのメリット | IB CFDのデメリット |

|---|---|

| 印紙税や金融取引税はありません(英国、フランス、ベルギー) | 所有権がありません |

| 株式に比べ手数料や証拠金が一般的に低めです | 複雑なコーポレトアクションがいつでも反映されるわけではありません |

| 配当金は租税条約レートの対象となり、請求の必要がありません | 収益に対する税金は株式への税金と異なる場合があります(専門の税理士にご相談ください) |

| デイ・トレーディング規制の対象外です |

III. 費用および証拠金に関する留意点

IB CFDは、IB提供のすでに競争性のある株式と比較しても効率的なヨーロッパ株式の取引方法です。

先ず、IB CFDにかかる手数料は株式と比べて低額ですがスプレッドは同じです:

| ヨーロッパ | CFD | 株式 | |

|---|---|---|---|

| 手数料 | GBP | 0.05% | GBP 6.00 + 0.05%* |

| EUR | 0.05% | 0.10% | |

| 金利** | ベンチマーク +/- | 1.50% | 1.50% |

*注文につき+ 50,000英ポンドを超える場合は0.05%の超過金

**ポジションの合計価値に対するCFD金利、借入額に対する株式金利

CFDの手数料は取引が増えるほど低額になり、0.02%まで下がります。借入金利はポジションが大きいほど減少し、0.5%まで下がります。 詳細はCFD手数料およびCFD借入金利をご覧ください。

次に、CFDの必要証拠金は株式と比べて低額です。リテールクライアントは欧州証券市場監督局ESMAによる追加の必要証拠金の対象となります。詳細はIBKRにおけるESMA CFDルールの実施をご参照ください。

| CFD | 株式 | ||

|---|---|---|---|

| すべて | 標準 | ポートフォリオ・マージン | |

| 維持証拠金率* |

10% |

25% - 50% | 15% |

*ブルーチップ用に一般的な証拠金です。リテールクライアントは最低20%の委託証拠金の対象となります。株式には標準的な25%の日中維持証拠金、オーバーナイトは50%。 表示されているポートフォリオ・マージンは維持証拠金です(オーバーナイトを含み)。ボラティリティの高い場合には必要証拠金額も上がります

詳細はCFD必要証拠金をご参照ください。

IV. 例(プロフェッショナル・クライアント)

例を見てみましょう。Unilever’s Amsterdamリストからの過去一ヶ月(2012年5月14日から20取引日)のリターンは3.2%となり、今後のパフォーマンスも良好に見えます。200,000ユーロのエクスポージャーを建て、5日保有したいとします。取引を10回行って蓄積した後、さらに10回行って相殺します。かかる直接の費用は以下のようになります:

株式

| CFD | 株式 | ||

|---|---|---|---|

| 200,000ユーロのポジション | 標準 | ポートフォリオ・マージン | |

| 必要証拠金 | 20,000 | 100,000 | 30,000 |

| 手数料(往復) | 200.00 | 400.00 | 400.00 |

| 金利(簡略化されたもの) | 1.50% | 1.50% | 1.50% |

| 提供される資金額 | 200,000 | 100,000 | 170,000 |

| 提供を受ける日数 | 5 | 5 | 5 |

| 支払利息(1.5% 簡略化されたもの) | 41.67 | 20.83 | 35.42 |

| 直接費用合計(手数料 + 金利) | 241.67 | 420.83 | 435.42 |

| 原価差異 | 74%上がる | 80%上がる | |

注意:CFD支払金利は取引ポジション全体に大して計算されますが、株式にかかる金利は借入量に対して計算されます。株式およびCFDに適用されるレートは同じです。

今度は証拠金資金として20,000ユーロのみ持ち合わせがあると考えてみます。 Unileverが前月と同じようなパフォーマンスを継続すると考えると、そこから期待される利益は以下のようになります:

| レバレッジ利益 | CFD | 株式 | |

|---|---|---|---|

| 利用可能な証拠金 | 20,000 | 20,000 | 20,000 |

| 合計投資額 | 200,000 | 40,000 | 133,333 |

| 総利益(5日) | 1,600 | 320 | 1,066.66 |

| 手数料 | 200.00 | 80.00 | 266.67 |

| 支払利息(1.5% 簡略化されたもの) | 41.67 | 4.17 | 23.61 |

| 直接費用合計(手数料 + 金利) | 241.67 | 84.17 | 290.28 |

| 純利益(総利益-直接費用) | 1,358.33 | 235.83 | 776.39 |

| 証拠金投資額に対するリターン | 0.07 | 0.01 | 0.04 |

| 差異 | 利益が83%下がる | 利益が43%下がる | |

| レバレッジリスク | CFD | 株式 | |

|---|---|---|---|

| 利用可能な証拠金 | 20,000 | 20,000 | 20,000 |

| 合計投資額 | 200,000 | 40,000 | 133,333 |

| 総利益(5日) | -1,600 | -320 | -1,066.66 |

| 手数料 | 200.00 | 80.00 | 266.67 |

| 支払利息(1.5% 簡略化されたもの) | 41.67 | 4.17 | 23.61 |

| 直接費用合計(手数料 + 金利) | 241.67 | 84.17 | 290.28 |

| 純利益(総利益-直接費用) | -1,841.67 | -404.17 | -1,356.94 |

| 差異 | 損失が78%下がる | 損失が26%下がる | |

V. CFDのリソース

以下はIB提供のCFDに関する詳細を記載したリンクです:

以下のビデオレッスンもご利用可能です:

VI. よくあるご質問

CFDとしてどのような株式が利用できますか?

米国、西ヨーロッパ、北欧および日本における大型および中型株です。 流動小型株の取り扱いのあるマーケットも多くあります。詳細はCFD商品リストをご覧ください。ご利用可能国は近い将来、さらに追加される予定です。

株式指数とFOREXにCFDは含まれていますか?

はい。詳細およびQ&AはIB株価指数CFD - 詳細およびQ&A and Forex CFD - 詳細およびQ&Aをご覧ください。

株式CFDクオートはどのように設定するのですか?

IB CFDのクオートは原資産株式に対するスマートルーティング・クオートと同じです。 IBではスプレッドを広げる、またはお客様に対抗するポジションを建てることはありません。 詳細はCFDマーケットモデルの概要をご覧ください。

取引所にての自分の指値注文は見ることができますか?

はい。IBではダイレクト・マーケット・アクセス(DMS)を提供しており、成行とならない(指値の)注文の原資産ヘッジは取引されている取引所の 板画面に直接表示されています。これはまたCFDを原資産のビッド価格で購入しオファー価格で売る注文の発注ができるということになります。また一般の市場よりも良い価格の注文が他のクライアントから出てきた場合、価格向上につながることもあります。

株式CFDの証拠金はどのように設定するのですか?

IBでは各原資産の過去のボラティリティに基づき、 リスク・ベースで証拠金を採用しています。最小証拠金は10%です。 IB CFDの証拠金はほとんどこのレートで設定されており、これによりCFDは多くの場合、原資産株式の取引に比べて効果的ですが、 リテールクライアントは欧州証券市場監督局ESMAによる追加の必要証拠金の

対象となります。 詳細はIBKRにおけるESMA CFDルールの実施をご参照ください。ポートフォリオ内の各CFDポジション間または個別のCFDポジションと原資産株式のエクスポージャー間のオフセットはありません。集中しているポジションや大型のポジションは追加の証拠金の対象の対象になる可能性があります。詳細はCFD必要証拠金をご参照ください。

売りの株式CFDは強制買い入れの対象になりますか?

はい。原資産株式の借入が困難または不可能になった場合、売りのCFDポジション保持者は買い入れの対象になります。

配当金やコーポレートアクションはどのように取り扱われますか?

一般的にIBでは、コーポレートアクションの経済的な影響を、原資産の有価証券の保持を同じようにCFDを保持しているお客様に対し反映させます。配当金は現金調整として反映され、その他のコーポレートアクションは現金またはポジションの調整、またはその両方として反映されます。例として、コーポレートアクションが株式数の変動につながった場合(株式分割や、株式の合併など)、CFD数も合わせて調整されます。アクションが上場株を持つ新法人の設立にいたり、IBがこれをCFDとして提供する場合には、これに適格な量で新規のロングおよびショート・ポジションが作成されます概要はCFDコーポレートアクションをご覧ください。

*合併などの複雑なコーポレートアクションに対しCFDが正確に調整されない場合もあることをご了承ください。このような場合、CFDは権利落ち日前に終了する可能性があります。

誰でもIB CFDの取引はできますか?

米国、カナダおよび香港以外の国の居住者はIB CFD取引が可能です。シンガポール居住者は、シンガポールに上場されている株式をベースとする以外のIB CFDをお取引いただけます。居住地に基づいて設定される例外で、特定の投資家タイプに適用されるものはありません。

IB CFDの取引はどのように始めればよいのでしょうか?

アカウント・マネジメントよりCFD用の取引許可を設定し、該当する取引開示に合意してください。 IB LLCの口座をお持ちの場合、この後、弊社が新規の口座セグメントを設定します(お客様のすでにお持ちの口座番号の末尾に「F」を追加します)。設定が承認され次第、お取引が可能になります。F口座に別途、資金をご入金いただく必要はありません。資金はCFDの必要証拠金に合わせてお客様のメイン口座より自動的に移動されます。

必要なマーケットデータはありますか?

IB株式CFD用のマーケットデータは、その原資産株式用のマーケットデータになります。 このため関連取引所に対するマーケットデータ許可が必要となります。株式取引に対し取引所のマーケットデータ許可をすでに設定されている場合には、それ以上必要なものはありません。現在マーケットデータ許可の持ち合わせがない取引所におけるCFD取引をご希望の場合には、原資産株式の取引に対する許可と同じ方法で許可を設定することができます。

CFD取引およびポジションはステートメントにどのように表示されますか?

B LLCの口座をお持ちの場合、 CFDポジションは主要口座番号の末尾に「F」を追加した形で別の口座セグメントに維持されます。アクティビティー・ステートメント上のFセグメントは、別途またはメイン口座と合わせて表示することができます。選択はアカウント・マネジメントのステートメント画面より可能です。その他の口座に関しては、通常の口座ステートメントと同じようにCFDもその他の取引商品と共に表示されます。

別のブローカーからのCFDポジションの移管はできますか?

別ブローカーとの合意の下、弊社にてCFDポジション移管作業を進めます。株式ポジションの移管に比べてCFDポジションの移管は複雑なため、通常、弊社では少なくとも100,000米ドル相当のポジションを条件としております。

株式CFDのチャートはありますか?

はい。

IBでのCFD取引にはどのような口座保護が適用しますか?

CFDはIB UKを取引先とする取引であり、取引所による取引や中央決済機関による決済はありません。IB UKをCFD取引の取引先とするため、クレジットリスクを含める、IB UKとの取引に関連する取引やビジネス上のリスクの対象となります。しかしながら、すべてのお客様の資金は法人クライアントも含め、完全に分離されています。IB UKは英国金融サービス補償計画(UK Financial Services Compensation Scheme「FSCS」)に参加しています。IB UKは、米国証券投資者保護公祉(「SIPC」)のメンバーではありません。CFD取引に関連するリスクの詳細はIB UK CFDリスク・ディスクロージャーをご参照ください。

個人、ファミリー、機関など、どのような種類のIB口座でCFD取引ができますか?

CFD取引はすべてマージン口座でご利用可能です。キャッシュまたはSIPPではご利用いただけません。

特定のCFDで保有可能の最大ポジションを教えてください。

事前に設定されている制限はありませんが、ポジションがかなり大型の場合、必要証拠金が増加する場合があることにお気をつけください。詳細はCFD必要証拠金をご参照ください。

電話によるCFDの取引はできますか?

いいえ。例外的にクロージング注文の処理をお電話にてお引き受けすることはありますが、オープニング注文はお受けしておりません。

CFDはレバレッジによる損失のリスクが高い複雑な商品です。

62%の個人投資家口座に、IBKR(UK)とのCFD取引による損失が発生しています。

お取引を開始される前に、CFDの機能の仕方および損失の際のリスクをご理解ください。

ESMAルール

欧州証券市場監督局(ESMA)は、2018年8月1日より有効となる一時的な介入策(ESMA Decision)をて発行しました。

これによる規制には以下が含まれます: 1) CFDのポジションを建てるにあたってレバレッジの上限; 2) 口座ごとの証拠金解約; 3) マイナス残高に対する口座ごとの保護; 4) CFD取引へのインセンティブに対する規制; および 5) 標準的なリスク警告。

ESMAによる決定はリテールクライアントのみに適用されます。 特定投資家のお客様への影響はありません。

CFDはレバレッジによる損失のリスクが高い複雑な商品です。

62%の個人投資家口座に、IBKR(UK)とのCFD取引による損失が発生しています。

お取引を開始される前に、CFDの機能の仕方および損失の際のリスクをご理解ください。

Allocation of Partial Fills

How are executions allocated when an order receives a partial fill because an insufficient quantity is available to complete the allocation of shares/contracts to sub-accounts?

Overview:

From time-to-time, one may experience an allocation order which is partially executed and is canceled prior to being completed (i.e. market closes, contract expires, halts due to news, prices move in an unfavorable direction, etc.). In such cases, IB determines which customers (who were originally included in the order group and/or profile) will receive the executed shares/contracts. The methodology used by IB to impartially determine who receives the shares/contacts in the event of a partial fill is described in this article.

Background:

Before placing an order CTAs and FAs are given the ability to predetermine the method by which an execution is to be allocated amongst client accounts. They can do so by first creating a group (i.e. ratio/percentage) or profile (i.e. specific amount) wherein a distinct number of shares/contracts are specified per client account (i.e. pre-trade allocation). These amounts can be prearranged based on certain account values including the clients’ Net Liquidation Total, Available Equity, etc., or indicated prior to the order execution using Ratios, Percentages, etc. Each group and/or profile is generally created with the assumption that the order will be executed in full. However, as we will see, this is not always the case. Therefore, we are providing examples that describe and demonstrate the process used to allocate partial executions with pre-defined groups and/or profiles and how the allocations are determined.

Here is the list of allocation methods with brief descriptions about how they work.

· AvailableEquity

Use sub account’ available equality value as ratio.

· NetLiq

Use subaccount’ net liquidation value as ratio

· EqualQuantity

Same ratio for each account

· PctChange1:Portion of the allocation logic is in Trader Workstation (the initial calculation of the desired quantities per account).

· Profile

The ratio is prescribed by the user

· Inline Profile

The ratio is prescribed by the user.

· Model1:

Roughly speaking, we use each account NLV in the model as the desired ratio. It is possible to dynamically add (invest) or remove (divest) accounts to/from a model, which can change allocation of the existing orders.

Basic Examples:

Details:

CTA/FA has 3-clients with a predefined profile titled “XYZ commodities” for orders of 50 contracts which (upon execution) are allocated as follows:

Account (A) = 25 contracts

Account (B) = 15 contracts

Account (C) = 10 contracts

Example #1:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 10 am (ET) the order begins to execute2but in very small portions and over a very long period of time. At 2 pm (ET) the order is canceled prior to being executed in full. As a result, only a portion of the order is filled (i.e., 7 of the 50 contracts are filled or 14%). For each account the system initially allocates by rounding fractional amounts down to whole numbers:

Account (A) = 14% of 25 = 3.5 rounded down to 3

Account (B) = 14% of 15 = 2.1 rounded down to 2

Account (C) = 14% of 10 = 1.4 rounded down to 1

To Summarize:

A: initially receives 3 contracts, which is 3/25 of desired (fill ratio = 0.12)

B: initially receives 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: initially receives 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The system then allocates the next (and final) contract to an account with the smallest ratio (i.e. Account C which currently has a ratio of 0.10).

A: final allocation of 3 contracts, which is 3/25 of desired (fill ratio = 0.12)

B: final allocation of 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: final allocation of 2 contract, which is 2/10 of desired (fill ratio = 0.20)

The execution(s) received have now been allocated in full.

Example #2:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 11 am (ET) the order begins to be filled3 but in very small portions and over a very long period of time. At 1 pm (ET) the order is canceled prior being executed in full. As a result, only a portion of the order is executed (i.e., 5 of the 50 contracts are filled or 10%).For each account, the system initially allocates by rounding fractional amounts down to whole numbers:

Account (A) = 10% of 25 = 2.5 rounded down to 2

Account (B) = 10% of 15 = 1.5 rounded down to 1

Account (C) = 10% of 10 = 1 (no rounding necessary)

To Summarize:

A: initially receives 2 contracts, which is 2/25 of desired (fill ratio = 0.08)

B: initially receives 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: initially receives 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The system then allocates the next (and final) contract to an account with the smallest ratio (i.e. to Account B which currently has a ratio of 0.067).

A: final allocation of 2 contracts, which is 2/25 of desired (fill ratio = 0.08)

B: final allocation of 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: final allocation of 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The execution(s) received have now been allocated in full.

Example #3:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 11 am (ET) the order begins to be executed2 but in very small portions and over a very long period of time. At 12 pm (ET) the order is canceled prior to being executed in full. As a result, only a portion of the order is filled (i.e., 3 of the 50 contracts are filled or 6%). Normally the system initially allocates by rounding fractional amounts down to whole numbers, however for a fill size of less than 4 shares/contracts, IB first allocates based on the following random allocation methodology.

In this case, since the fill size is 3, we skip the rounding fractional amounts down.

For the first share/contract, all A, B and C have the same initial fill ratio and fill quantity, so we randomly pick an account and allocate this share/contract. The system randomly chose account A for allocation of the first share/contract.

To Summarize3:

A: initially receives 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: initially receives 0 contracts, which is 0/15 of desired (fill ratio = 0.00)

C: initially receives 0 contracts, which is 0/10 of desired (fill ratio = 0.00)

Next, the system will perform a random allocation amongst the remaining accounts (in this case accounts B & C, each with an equal probability) to determine who will receive the next share/contract.

The system randomly chose account B for allocation of the second share/contract.

A: 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: 0 contracts, which is 0/10 of desired (fill ratio = 0.00)

The system then allocates the final [3] share/contract to an account(s) with the smallest ratio (i.e. Account C which currently has a ratio of 0.00).

A: final allocation of 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: final allocation of 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: final allocation of 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The execution(s) received have now been allocated in full.

Available allocation Flags

Besides the allocation methods above, user can choose the following flags, which also influence the allocation:

· Strict per-account allocation.

For the initially submitted order if one or more subaccounts are rejected by the credit checking, we reject the whole order.

· “Close positions first”1.This is the default handling mode for all orders which close a position (whether or not they are also opening position on the other side or not). The calculation are slightly different and ensure that we do not start opening position for one account if another account still has a position to close, except in few more complex cases.

Other factor affects allocations:

1) Mutual Fund: the allocation has two steps. The first execution report is received before market open. We allocate based onMonetaryValue for buy order and MonetaryValueShares for sell order. Later, when second execution report which has the NetAssetValue comes, we do the final allocation based on first allocation report.

2) Allocate in Lot Size: if a user chooses (thru account config) to prefer whole-lot allocations for stocks, the calculations are more complex and will be described in the next version of this document.

3) Combo allocation1: we allocate combo trades as a unit, resulting in slightly different calculations.

4) Long/short split1: applied to orders for stocks, warrants or structured products. When allocating long sell orders, we only allocate to accounts which have long position: resulting in calculations being more complex.

5) For non-guaranteed smart combo: we do allocation by each leg instead of combo.

6) In case of trade bust or correction1: the allocations are adjusted using more complex logic.

7) Account exclusion1: Some subaccounts could be excluded from allocation for the following reasons, no trading permission, employee restriction, broker restriction, RejectIfOpening, prop account restrictions, dynamic size violation, MoneyMarketRules restriction for mutual fund. We do not allocate to excluded accountsand we cancel the order after other accounts are filled. In case of partial restriction (e.g. account is permitted to close but not to open, or account has enough excess liquidity only for a portion of the desired position).

Footnotes:

Overview of Dividend Payments in Lieu ("PIL")

Payment In Lieu of a Dividend (“payment in lieu” or “PIL”) is a term commonly used to describe a cash payment to an account in an amount equivalent to the ordinary dividend. Generally, the amount paid is per share owned. In addition, the dividend in most cases is paid quarterly (i.e., four times per year). The dividend payment is classified as follows: (1) ordinary dividend; and/or (2) payment in lieu of dividend. The former designation is for a payment received directly from the issuer or its paying agent. The latter designation is used when a cash payment is received from other than the issuer or the issuer’s agent.

Payment in lieu of an ordinary dividend may be received when the shares have been bought on margin, or when the account has a subsequent margin loan due to borrowing money to facilitate the payment for additional purchases of shares or as the result of a withdrawal from the margin account. Payment in lieu of a dividend may also be received when shares are owed to the brokerage firm and have not been received by the dividend record date.

To better understand the difference between an ordinary dividend and a payment in lieu, we will explain the steps taken by IB to comply with US regulations. Each business day, the Firm analyzes the positions in each customer account, every borrow, every loan, every pledge of shares for each security held by its customers to determine how many shares are held on margin and the associated margin loan balances. For each security that is fully paid, we are required to segregate those shares in a good control location (for example, a depository or a US bank. See KB1964). For shares that are held as collateral for a margin loan we are allowed to hypothecate and re-hypothecate shares valued up to 140 percent of the total debit balance in the customer account (See KB1967).

While the guidelines noted above for segregation of securities are clear, there are exceptions that are outside of the Firm's control. For instance, through no fault of its own, IB may have a deficit in segregated shares due to customer activity that changes the Firm’s overall segregation requirement for a security. This may be for a variety of reasons including a delay in receiving shares that have been loaned out to a counterparty after segregation requirements are recalculated and the Firm has issued a stock loan recall, sales of securities by one or more customers that reduce or eliminate margin loans, the deposit of cash by customers that similarly reduce or eliminate margin loans, or a failure of a counterparty to deliver shares for a trade settlement.

Upon issuing a recall of shares loaned, rules permit the borrower of the shares up to 3 business days to return them. The borrower of the shares is required to return them to us when we issue a recall, but if by business day 3 the shares have not been returned, IB may then issue a buy-in notice to begin the process of regaining possession of the shares. An additional 3 business days is generally needed for the purchased shares to settle and be delivered to the firm. Similarly if a counterparty fails to deliver by settlement date, shares to IB to settle a customer purchase, IB can issue a buy-in notice but the purchase of such shares are also subject to trade settlement in 3 days.

To summarize, if by the record date of a dividend certain shares have not been delivered to IB, the Firm will be paid an amount of cash that is equivalent to the dividend amount, but IB will not receive a qualified dividend payment directly from the issuer. In such cases, the Firm will receive PIL and will have no choice but to allocate such payment in lieu to customer accounts. The firm first allocates PIL to those accounts who hold the shares as collateral for a margin loan. If, after PIL is allocated to all shareholders whose accounts are not fully paid, any portion of PIL remains to be paid, it is allocated on a pro-rata basis to each remaining client account.

Account holders should be aware that a PIL may have different tax consequences than an ordinary dividend and should consult a tax advisor to understand such differences and whether they apply to their particular situation.

Exposure Fee Monitoring via Account Window

The Account Window provides the high-level information suitable for monitoring one's account on a real-time basis. This includes key balances such as total equity and cash, the portfolio composition and margin balances for determining compliance with requirements and available buying power. This window also includes information relating to the most recently assessed exposure fee and a projection of the next fee taking into consideration current positions.

To open the Account Window:

• From TWS classic workspace, click on the Account icon, or from the Account menu select Account Window (Exhibit 1)

Exhibit 1

.jpg)

• From TWS Mosaic workspace, click on Account from the menu, and then select Account Window (Exhibit 2)

Exhibit 2

.jpg)

After opening the window, scroll down to the Margin Requirements section and click on the + sign in the upper-right hand corner to expand the section. There, the "Last" and "Estimated Next" exposure fees will be detailed for each of the product classifications to which the fee applies (e.g., Equity, Oil). Note that the "Last" balance represents the fee as of the date last assessed (note that fees are computed based upon open positions held as of the close of business and assessed shortly thereafter). The "Estimated Next" balance represents the projected fee as of the current day's close taking into account position activity since the prior calculation (Exhibit 3).

Exhibit 3.jpg)

To set the default view when the section is collapsed, click on the checkbox alongside any line item and those line items will remain displayed at all times.

Please see KB2275 for information regarding the use of IB's Risk Navigator for managing and projecting the Exposure Fee and KB2276 for verifying exposure fee through the Order Preview screen.

Important Notes

1. The Estimated Next Exposure Fee is a projection based upon readily available information. As the fee calculation is based upon information (e.g., prices and implied volatility factors) available only after the close, the actual fee may differ from that of the projection.

2. Exposure Fee Monitoring via the Account window is only available for accounts that have been charged an exposure fee in the last 30 days

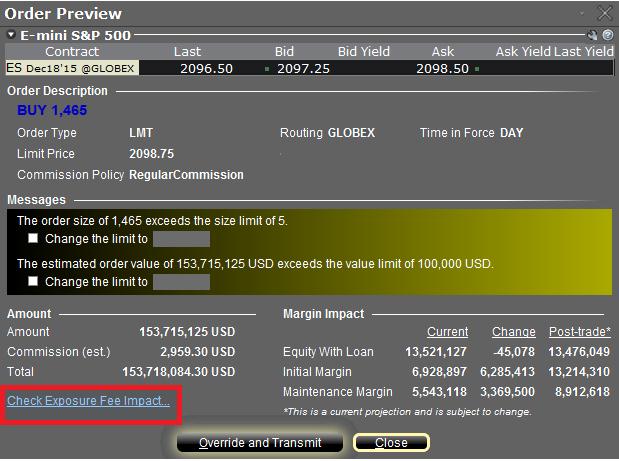

Order Preview - Check Exposure Fee Impact

IB provides a feature which allows account holders to check what impact, if any, an order will have upon the projected Exposure Fee. The feature is intended to be used prior to submitting the order to provide advance notice as to the fee and allow for changes to be made to the order prior to submission in order to minimize or eliminate the fee.

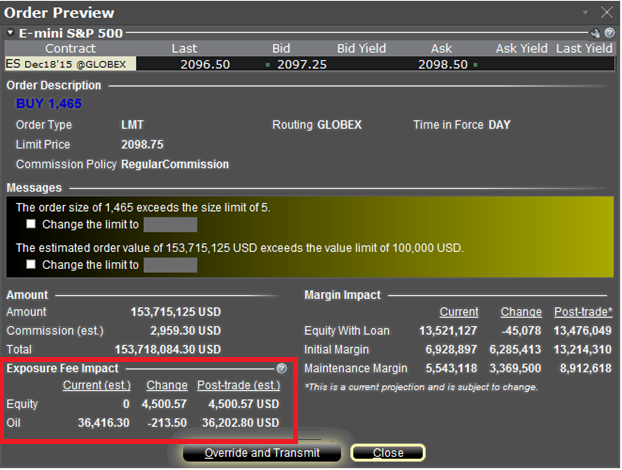

The feature is enabled by right-clicking on the order line at which point the Order Preview window will open. This window will contain a link titled "Check Exposure Fee Impact" (see red highlighted box in Exhibit I below).

Exhibit I

Clicking the link will expand the window and display the Exposure fee, if any, associated with the current positions, the change in the fee were the order to be executed, and the total resultant fee upon order execution (see red highlighted box in Exhibit II below). These balances are further broken down by the product classification to which the fee applies (e.g. Equity, Oil). Account holders may simply close the window without transmitting the order if the fee impact is determined to be excessive.

Exhibit II

Please see KB2275 for information regarding the use of IB's Risk Navigator for managing and projecting the Exposure Fee and KB2344 for monitoring fees through the Account Window

Important Notes

1. The Estimated Next Exposure Fee is a projection based upon readily available information. As the fee calculation is based upon information (e.g., prices and implied volatility factors) available only after the close, the actual fee may differ from that of the projection.

2. The Check Exposure Fee Impact is only available for accounts that have been charged an exposure fee in the last 30 days

Tools Provided to Monitor and Manage Margin

IB provides a variety of tools and information intended to provide account holders with real-time details as to their state of margin compliance so as to avoid forced liquidations. These include the following:

a. Account Window – The account window is available for real-time account activity monitoring. This window will display key values that update with every price change in the portfolio. Included are account balances (cash, Net Liquidation Value, Equity with Loan Value), margin requirements (current, look ahead, overnight and post expiration), and balances available for trading (Available Funds and Excess Equity).

b. Preview Order/Check Margin – Prior to transmitting an order it can be previewed including the impact upon the margin requirement were the order to be executed. Additional information may be found in KB644.

c. Communications – IB will act to send out communications via TWS bulletin and/or email when the margin cushion in an account reaches 10% and a margin deficiency is therefore approaching. Account holders may also create their own margin alerts based upon the margin cushion which, when triggered, may generate email or text message alerts, TWS pop-up messages and flashing rows, and sound alarms.

d. Reports – A Daily Margin Report is made available with Account Management which reflects key margin balances and for portfolio margin accounts, requirements broken down by security class.

In addition, IB provides a Last to Liquidate feature within the TWS Account window that allows customers to specify the positions they would prefer IB liquidate last in the event of a margin deficit. While IB will attempt on a best efforts basis to adhere to such requests, account positions and market conditions may make doing so impractical and IB therefore reserves the right to liquidate in the sequence it deems most optimal.

Trading on margin in an IRA account

IRA accounts, by definition, may not use borrowed funds to purchase securities and must pay for all long stock purchases in full, may not carry short stock positions and may not hold a debit cash balance (in any currency). IRA accounts are eligible to carry futures and option contracts. In addition, IB offers a specific form of IRA account referred to as a “Margin IRA” that allows the account holder to trade with unsettled funds, carry American style option spreads and maintain long balances in multiple currency denominations.

For additional information regarding trading permissions in an IRA account, refer to KB188.