Verplichte extra aflossing (cash sweep)

Achtergrond

Er zijn twee afzonderlijke subaccounts of segmenten onderliggend aan het IB Universalaccount, één voor de effectenposities en -saldi die onderworpen zijn aan de klantbeschermingsregels van de SEC en één voor de grondstoffenposities en -saldi die onderworpen zijn aan de klantbeschermingsregels van de CFTC. Deze Universal Accountstructuur is ontwikkeld om de administratieve overhead te verminderen die klanten anders zouden hebben als zij twee verschillende accounts zouden moeten aanhouden (bijv. overschrijvingen van contant geld tussen accounts, inloggen en bestellingen indienen via aparte accounts, meerdere afschriften, enz.) en tegelijkertijd de door de regelgeving vereiste scheiding te handhaven.

Deze regelgeving vereist dat alle effectentransacties worden uitgevoerd en marge ontvangen in het effectensegment van het universele account, terwijl grondstoffentransacties moeten worden uitgevoerd in het grondstoffensegment.1 Hoewel de regelgeving de bewaring van volgestorte effectenposities in het grondstoffensegment als margeonderpand toestaat, doet IB dit niet, waardoor de hypothecaire zekerheid ervan wordt beperkt tot de restrictievere regels van de SEC. Gezien de regelgeving en het beleid die de beslissing om posities aan te houden in het ene segment versus het andere bepalen, blijft contant geld het enige activum dat tussen de twee kan worden overgedragen en waarover de klant kan beslissen.

Hieronder volgt een bespreking van de aangeboden opties voor verplichte extra aflossing, de procedure voor het selecteren van een optie en de selectieoverwegingen.

Opties voor verplichte extra aflossing (cash sweep)

Klanten kunnen kiezen uit 3 opties voor sweeps, waarvan de beschrijvingen hieronder staan:

1. Geen sweep van overtollige middelen - bij deze keuze worden overtollige middelen niet van het ene segment naar het andere verplaatst, tenzij dit noodzakelijk is om:

a. een margetekort in het andere segment op te heffen/te verminderen;

b. een debetsaldo in contanten en dus rentelasten in een bepaald segment te minimaliseren. Let op: dit is de standaardoptie en de enige optie voor accounthouders met slechts één van de handelspermissies voor effecten of grondstoffen.

2. Sweep van overtollige middelen naar mijn IB-account voor effecten - hier worden kassaldi alleen in het segment grondstoffen aangehouden voor zover dat nodig is om aan de huidige margevereiste voor grondstoffen te voldoen. Alle contanten die hoger zijn dan de margevereisten en die worden gegenereerd als gevolg van hetzij een toename van de contanten (bijv. gunstige variatie en/of transactiegerelateerd), hetzij een afname van de margevereiste (bijv. wijzigingen in de SPAN-risicomatrixen en/of transactiegerelateerd), worden automatisch overgeboekt van het grondstoffensegment naar het effectensegment. Let op: de accounthouder moet toestemming hebben om effecten te verhandelen om deze optie te kunnen selecteren.

3. Sweep overtollige middelen naar mijn IB-account voor grondstoffen - hier worden kassaldi alleen in het effectensegment aangehouden voor zover zij, samen met eventuele andere effectenposities met leenwaarde, nodig zijn om aan de huidige margevereiste voor effecten te voldoen. Let op: de accounthouder moet toestemming hebben om grondstoffen te verhandelen om deze optie te kunnen selecteren.

Andere items om op te letten:

- Aangezien het Universal Account het mogelijk maakt kassaldi in verschillende valuta's aan te houden, bestaat er een hiërarchie om te bepalen welke bepaalde valuta eerst moet worden overgeboekt wanneer er lange saldi in meerdere valuta's bestaan In deze situaties worden eerst de saldi in de basisvaluta overgeboekt, vervolgens de USD en vervolgens de resterende lange saldi in ander valuta's, van hoog naar laag.

- Om de kans te minimaliseren dat een segment een margetekort oploopt na de overdracht van overtollige contanten naar het andere segment, wordt niet het volledige overschot overgedragen en wordt een buffer gelijk aan 5% van de onderhoudsmargevereiste aangehouden. Om de operationele overhead van de overdracht van nominale saldi tot een minimum te beperken, zullen saldi alleen worden overgedragen indien, na verrekening van de 5%-margebuffer, het eventuele overschot niet minder dan 1% van het accountvermogen of $ 200 bedraagt.

- Bij het uitvoeren van de kredietcontrole vóór de transactie om te bepalen of een account voldoende eigen vermogen aanhoudt om een nieuwe order te ondersteunen, wordt een overschot aan contanten in het ene segment in aanmerking genomen voor transacties in het andere segment (hoewel een sweep pas plaatsvindt nadat de transactie is uitgevoerd en alleen als het dan nodig blijft om aan de margeverplichtingen te voldoen). Accounts die zijn aangemerkt als Pattern Day Trader (patroondaghandelaar) en die zijn onderworpen aan een kredietcontrole vóór de transactie waarbij rekening wordt gehouden met het vermogen van de vorige en de huidige dag, dienen bijzondere aandacht te besteden aan het onderstaande onderdeel 'Selectieoverwegingen'.

Een sweep-optie selecteren

Als uw versie van Accountbeheer een reeks menu-opties aan de linkerkant bevat, selecteert u de menu-opties Accountadministratie en vervolgens Sweep van overtollige middelen. Als uw versie menu-opties heeft aan de bovenkant, selecteert u de menu-opties Beheer account/instellingen en vervolgens Configureer account/Sweep van overtollige middelen. Ongeacht uw versie krijgt u het volgende scherm te zien:

U kunt vervolgens het keuzerondje naast de optie van uw keuze selecteren en op de knop Doorgaan klikken. Uw keuze wordt van kracht vanaf de eerstvolgende werkdag en blijft van kracht totdat een andere optie is gekozen. Met inachtneming van de hierboven vermelde instellingen voor handelsrechten is er geen beperking op wanneer of hoe vaak u uw veegmethode mag wijzigen.

Selectieoverwegingen

Hoewel de beslissing om het ene segment te verkiezen boven het andere met het oog op het aanhouden van overtollige kasmiddelen kan worden beïnvloed door subjectieve keuzes en voorkeuren die uniek zijn voor elke klant (bv. klant houdt activa aan die aanzienlijk en geconcentreerd zijn in het ene segment vs. het andere), worden hieronder verschillende factoren beschreven die in overweging moeten worden genomen:

1. Pattern Day Trading Equity - De koopkracht van effecten van accounts die door de regelgeving zijn aangewezen als patroondaghandelaren (d.w.z. 4 of meer dagtransacties binnen een periode van 5 werkdagen) wordt beperkt door het laagste van de huidige of voorgaande dagwaarde in het effectensegment. Een keuze om overtollige middelen naar het grondstoffensegment over te dragen, voorkomt dat deze middelen in deze berekening worden opgenomen, waardoor de capaciteit om nieuwe orders in te voeren mogelijk wordt beperkt. Om het gebruik van eigen vermogen voor het invoeren van effectenorders te maximaliseren, zou men ervoor moeten kiezen om overtollige fondsen naar het effectensegment te vegen. Let op dat een keuze voor het effectensegment geen afbreuk doet aan de mogelijkheid om grondstoffenorders in te voeren, aangezien de regels voor patroondaghandel niet van toepassing zijn op dergelijke accounts.

2. Verzekering – SIPC-bescherming wordt verleend aan activa in het effectensegment en er is geen overeenkomstige verzekeringsregeling voor het grondstoffensegment. Saldi boven de SIPC-sublimiet van $ 250.000 in contanten (Lloyd-sublimiet van $ 900.000 in contanten, indien van toepassing) worden echter niet gedekt. Klanten van IB Canada en IB UK zijn ook onderworpen aan dekkingsregels zoals gespecificeerd door respectievelijk het CIPF en de FSCS.

3. Rente-inkomsten –als alle andere omstandigheden gelijk blijven, zullen klanten waarschijnlijk de meest optimale rente-inkomsten ontvangen op lange kassaldi die niet zijn opgesplitst tussen de segmenten effecten en grondstoffen, aangezien deze niet worden samengevoegd voor rentekredietdoeleinden (aangezien zij onderworpen zijn aan afzonderlijke segregatiepools en herbeleggingsregels). Dit, samen met het feit dat voor kredieten een minimaal kassaldo moet worden aangehouden en dat voor hogere saldi preferentiële tarieven gelden, zijn factoren waarmee rekening moet worden gehouden bij de keuze voor sweep.2

Andere relevante kennisbankartikelen:

A Comparison of U.S. Segregation Model (Een vergelijking van Amerikaanse segregatiemodellen)

A Comparison of U.S. Segregation Model (Een vergelijking van Amerikaanse segregatiemodellen)

Voetnoten:

11Aangezien OneChicago enkelvoudige aandelenfutures een hybride product zijn dat gezamenlijk door de SEC en de CFTC wordt gereguleerd, kunnen ze op beide accounttypes worden gekocht en verkocht. IB voert dergelijke transacties echter uit in het effectensegment van het Universal Account, omdat dit nodig is om de marge tussen de enkelvoudige aandelenfutures en elke kwalificerende aandelen- of optiepositie te verlichten.

22Neem bijvoorbeeld een account dat een lang USD-saldo van $ 9.000 aanhoudt in elk van de segmenten (effecten en grondstoffen). Afhankelijk van de benchmark Fed Funds Effective Rate, zou het account in aanmerking komen voor rente op $ 8.000 ($ 18.000 - $ 10.000) als de twee saldi in één segment zouden worden aangehouden, maar aangezien saldi onder $ 10.000 in een van de twee segmenten niet in aanmerking komen voor rente, zou het account niets kunnen opleveren zonder te kiezen voor een sweep-optie. Ook zou men in aanmerking komen voor rente op een hoger niveau als de accounthouder als gevolg van een sweep-keuze in een bepaald segment een lang USD-kassaldo van meer dan $ 100.000 zou bereiken. Voor aanvullende informatie over renteberekeningen, inclusief een link naar de actuele benchmarkrente, zie KB39.

Key Information Documents (KID)

Overview:

IBKR is required to provide EEA and UK retail customers with Key Information Documents (KID) for certain financial instruments.

Relevant products include ETFs, Futures, Options, Warrants, Structured Products, CFDs and other OTC products. Funds include both UCITS and non-UCITS funds available to retail investors.

Generally KIDs must be provided in an official language of the country in which a client is resident.

However, clients of IBKR have agreed to receive communications in English, and therefore if a KID is available in English all EEA and UK clients can trade the product regardless of their country of residence.

In cases where a KID is not available in English, IBKR additionally supports other languages as follows:

| Language | Can be traded by residents or citizens* of |

| German | Germany, Austria, Belgium, Luxembourg and Liechtenstein |

| French | France, Belgium and Luxembourg |

| Dutch | the Netherlands and Belgium |

| Italian | Italy |

| Spanish | Spain |

*regardless of country of residence

Are CDs purchased through IBKR FDIC insured?

Certificates of Deposit (CDs) offered by IBKR are not FDIC insured and are subject to the credit risk of the issuing bank.

Information Regarding SIPC Coverage

1. Interactive Brokers LLC is a member of SIPC.

2. SIPC protects cash and securities held with Interactive Brokers.

3. SIPC does not generally cover commodity futures or options on futures.

4. SIPC protects cash, including US dollars and foreign currency, to the extent that the cash was "deposited with Interactive Brokers for the purpose of purchasing securities."

5. SIPC does not generally cover cash or foreign currency that is not "deposited with Interactive Brokers for the purpose of purchasing securities." For example, SIPC does not generally cover cash in commodity futures trading accounts.

6. Interactive Brokers is not able to make any statements or representations about how cash deposited into a securities account in connection with forex trading or swept from a commodities account would be treated by SIPC. SIPC protection would depend in part on whether the cash was considered to be "deposited with Interactive Brokers for the purpose of purchasing securities." Interactive Brokers expects that at least one factor in deciding this would be whether and the extent to which the customer engages in securities trading in addition to or in conjunction with forex or commodities trading.

Account holders seeking further information should refer such inquiries to their own legal counsel or SIPC.

Excess Margin Securities

The term "excess margin securities" refers to margin securities carried for the account of a customer having a market value in excess of 140 percent of the total debit balance in the customer's account. These securities are in excess of the securities held in a customer's margin account that are pledged by the customer as collateral for the margin loan and can be used to support the purchase of additional securities on margin

Example:

A customer whose account equity consists solely of a cash balance of USD 10,000 on Day 1 purchases 400 shares of stock ABC at USD 50 per share on Day 2.

| Account Balance | Day 1 | Day 2 |

| Cash | $10,000 | ($10,000) |

| Stock | $0 | $20,000 |

| Total | $10,000 | $10,000 |

On Day 2, the customer's excess margin securities total USD 6,000. This is calculated by subtracting 140% of the margin debit or loan balance from the market value of the stock position ($6,000 = $20,000 - {1.4 * $10,000}).

The term is relevant from a regulatory perspective as the SEC requires that U.S. broker dealers segregate and maintain in a good control location (e.g., DTC or bank) all customer securities which are deemed excess margin securities. Such securities cannot be pledged or loaned to finance the activities of the firm or other customers without specific written permission from the customer. The portion of the securities classified as margin securities ($20,000 - $6,000 or $14,000 in this example) are subject to a lien and may be pledged or loaned by the broker to others to assist in financing the loan made to the customer.

Note that securities which were excess margin at the date of acquisition may later be reclassified as margin securities based upon the customer's subsequent trade and/or margin borrowing activity. For example, if the loan value of excess margin securities is subsequently used to acquire additional securities on margin, a portion of securities will then be reclassified as margin securities and subject to a lien. If the customer subsequently deposits cash or sells securities to reduce or eliminate the margin loan, the securities will be reclassified as excess margin or fully paid and are required to be segregated.

See also "fully paid securities".

Fully Paid Securities

The term "fully paid securities" refers to securities held in a customer's margin or cash account that have been completely paid for and are not being pledged as collateral to support the purchase of other securities on margin. The term is relevant from a regulatory perspective as the SEC requires that U.S. broker dealers segregate and maintain in a good control location (e.g., DTC or bank) all customer securities which are fully paid. Such securities cannot be pledged or loaned to finance the activities of the firm or other customers.

Note that securities which were fully paid at the date of acquisition may later be reclassified as margin or excess margin securities based upon the customer's subsequent trade and/or borrowing activity. For example, if the loan value of fully paid securities is subsequently used to acquire additional securities on credit, a portion of securities will then be classified as margin securities and subject to a lien and potential pledge or hypothecation by the broker.

See also "excess margin securities".

Comparison of U.S. Segregation Models

INTRODUCTION

The regulation of securities and commodities products and brokers1 in the U.S. is administered by two distinct federal agencies, the Securities and Exchange Commission (SEC) for securities including stocks, ETFs, bonds, options and mutual funds and the Commodities Futures Trading Commission (CFTC) for commodities including futures and options on futures.2 While both agencies seek to safeguard customer assets by restricting their use and “segregating” them from assets of the broker, the regulations and manner in which they accomplish this differs. The following article provides a basic overview of two segregation models and additional considerations relating to IB accounts.

OVERVIEW

Differences between the CFTC and SEC segregation models originate largely from the products themselves, whose characteristics are fundamentally unique. Commodity products, by nature, do not involve an extension of credit by the broker to the customer as a futures contract is not an asset but rather a contingent liability which is marked-to-market and a long futures option, while an asset, must be paid for in-full. Consequently, non-option assets in a commodities account are generally comprised of funds deposited as margin to secure performance on the contracts therein. Since the broker may not use the funds of one customer to margin or guarantee the transactions of another, the commodities segregation requirement (CFTC Rules 1.20 – 1.30) is equal to the gross assets of all customers and the broker needs to add its own funds to segregation to cover customers whose net equity is in deficit.

A securities margin account, in contrast, can facilitate the extension of credit for the purpose of long securities (e.g., stocks, bonds) purchases or short securities sales on a secured basis. The segregation or reserve requirement rules recognize this through special provisions for the protection of each of the cash and securities components, further distinguishing fully-paid securities from those whose purchase the broker has financed and maintains a lien upon. Here, the broker must deposit into a separate bank account the net amount of customer cash balances3, in accordance with a formula set forth in SEC Rule 15c3-3. In addition, the broker must identify and segregate in a good control location (e.g., depository, bank) customer securities which meet the definition of “fully paid” or “excess margin”.

The table below provides a comparison of the main principals of each model.

| COMPARISON OF CFTC & SEC SEGREGATION MODELS | ||

| PRINCIPAL | CFTC | SEC |

|

Separation of Customer Balances

|

Commodity customer balances must be maintained separate from firm assets and cannot be used to finance proprietary business activities or to satisfy firm debts.

Funds used for trading on non-US commodity exchanges must be kept separate from those used for trading on U.S. exchanges (even for the same customer). Commodity customer balances must also be maintained separate from securities customer balances (even for the same customer). |

Securities customer balances must be maintained separate from firm assets and cannot be used to finance proprietary business activities or to satisfy firm debts. Securities customer balances must also be maintained separate from commodity customer balances (even for the same customer).

|

|

Priority in the Event of Broker Default

|

Commodity customers maintain priority and equal claim over assets in each of their respective U.S. segregated and non-U.S. secured pools.

No claim on assets in a commodity pool in which one is not a participant and no claim on securities customer assets. If commodity segregated assets are insufficient to meet claims and broker is insolvent, customers share equally in shortfall and become general creditors for residual claims. |

Securities customers maintain priority and equal claim over assets.4

No claim on commodity segregated assets. If securities segregated assets are insufficient to meet claims, broker is insolvent and claims exceed SPIC coverage, customers share equally in shortfall and become general creditors for residual claims.

|

| Segregation Style |

Gross – the broker may not use the funds of one customer to margin or guarantee the transactions of another and must segregate assets in an amount at least equal to the sum of all customer credit balances. |

Net – broker may use customer cash credit balances to finance, on a secured basis, margin loans to other customers and may lend or pledge a portion of customer securities purchased on margin to other customers selling short.

|

| Investment of Cash Balances |

Broker is allowed to reinvest commodity customer’s cash balances and retain an interest in the income generated. Permissible investments include: U.S. government securities, municipal securities, government sponsored enterprise securities, bank CDs, corporate obligations (commercial paper, notes and bonds) fully guaranteed as to principal and interest by the U.S. under the Temporary Liquidity Guarantee Program and money market mutual funds. Securities which are the subject of reinvestment must be maintained in a segregated account. |

Broker is allowed to reinvest securities customer’s cash balances and retain an interest in the income generated. Permissible investments limited to “qualified securities” defined as securities which are guaranteed as to both interest and principal by the U.S. government. Securities which are the subject of reinvestment must be held in Special Reserve Bank Account (i.e., segregated). |

| Computation Frequency | Daily | Weekly |

| Insurance | None | Securities Investor Protection Corporation (SIPC) provides insurance of up to USD 500,000 with a cash sublimit of USD 250,000. |

ADDITIONAL CONSIDERATIONS

In addition to the safeguards afforded through segregation, IB employs a number of policies and practices which serve to enhance the safety and security of accounts beyond that outlined above. These include the following:

- IB computes its securities segregation or reserve requirement on a daily rather than weekly basis as allowed by regulation, thereby ensuring timely determination as to the amount required to be reserved and the deposit of funds necessary to satisfy the requirement.

- IB’s does not avail itself of the generally more permissive rules with respect to the investment of commodity customer cash balances. These balances are instead invested in a manner similar to that of securities cash balances (i.e., U.S. government securities) with the exception of an occasional investment in money market funds.

- All customer securities positions are held in the securities segment of the Universal Account as opposed to the commodities (commodities margin met with cash and/or futures options), thereby limiting their hypothecation to the more restrictive rules of the SEC.

- In addition to SIPC coverage, IB maintains an excess SIPC policy with Lloyd's of London which, in aggregate with SIPC, offers insurance totaling $30 million (with a cash sublimit of $900,000), subject to an aggregate firm limit of $150 million.

- IB offers account holders the ability to sweep cash balances in excess of that required for margin purposes in either the securities or commodities segment to the other segment. Details as to this feature may be found in KB1851.

- For additional information regarding IB strength and security, please review the following website page.

Other Relevant Knowledge Base Articles:

Information Regarding SIPC Coverage

Footnotes:

1The term broker as used in this article is intended to refer to an organization registered with both the SEC as a Broker-Dealer and the CFTC as a Futures Commission Merchant for the purpose of conducting customer transactions

2Single stock futures are a hybrid product jointly regulated by the SEC and CFTC and allowed to be carried in either account type.

3Including cash obtained through the use of customer securities such bank pledges or stock loans less cash required to finance customer transactions (e.g., stock borrows, customer fails to deliver of securities, or margin deposited for short option positions with OCC).

4Assets, or customer property, which securities customers share in proportion to their net equity claim, include cash, margin securities and fully-paid securities held in “street name”. IB does not hold securities in the customer’s name which are not considered bulk customer property.

How to request a Digital Security Card+ (DSC+) replacement

Overview:

The below steps are required in order to:

- Replace a Digital Security Card+ which has been lost, stolen or has become inoperable

- Request a Digital Security Card+ alongside your current security device (if you are a new or existing Client with equity above $1,000,000, or equivalent)

Background:

1. Notify IBKR Client Services- Contact IBKR Client Services to obtain a temporary account access. This service can only be provided via telephone and requires the identity of the account holder to be verified, as detailed in the IBKR Knowledge Base.

2. Obtain an Online Security Code Card - Activate an Online Security Code Card, which offers enhanced protection and full Client Portal functionality for an extended period of 21 days. Please consult the IBKR Knowledge Base should you need guidance for this specific step.

3. Request the DSC+ replacement - Once you have completed the Online Security Code Card activation, please remain in the Secure Login System section of the Client Portal and order your replacement DSC.

Request a DSC+

1. Click on the button Request Physical Device.

.png)

2. The shipping address will be shown in the device information screen. If your address is outdated or invalid, you can amend it by clicking on Change Address and following the on-screen instructions. If you do not need to update your address, please proceed to step 3..png)

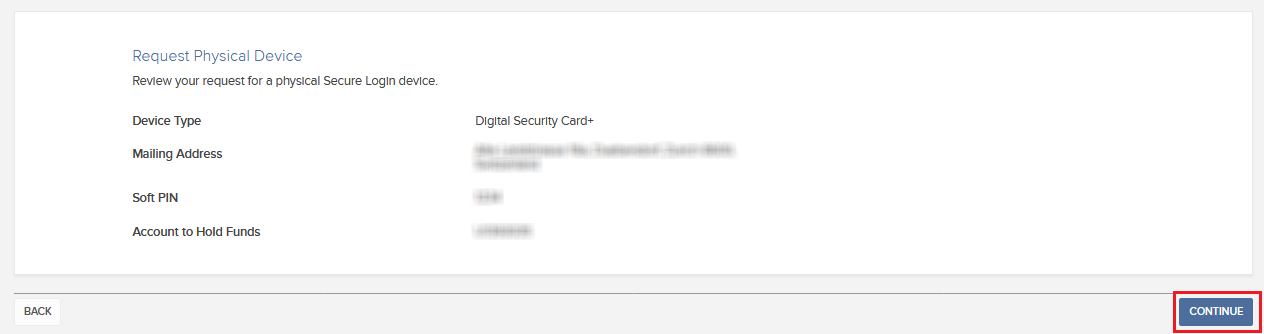

3. Enter a four-digit Soft PIN1 for your DSC+. Please make sure to remember the PIN you are typing since it will be necessary to activate and to operate your device. When applicable and desired, you may change the account on which the 20 USD deposit will be kept on hold2. Complete this step by clicking on Continue..png)

4. The system will show you a summary of your selection. Please make sure the information displayed is correct. Should you need to perform changes, click on the white Back button under the information field (not your browser back button), otherwise submit the request by clicking on Continue.

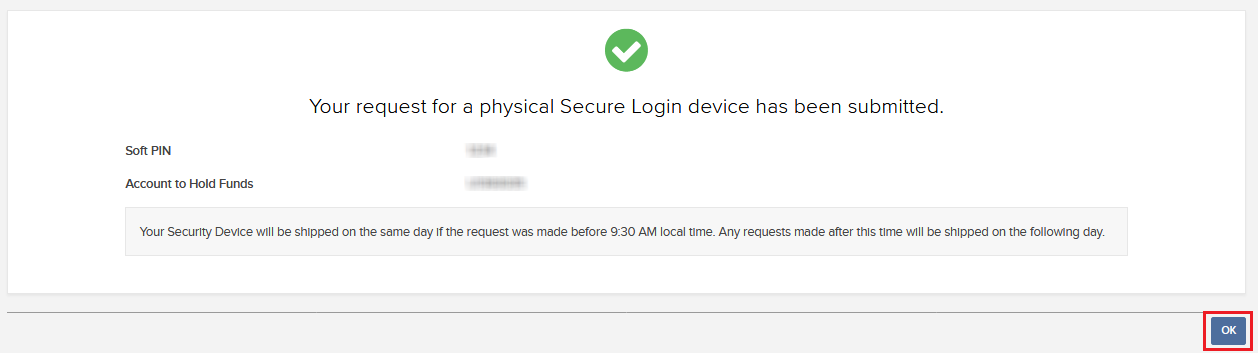

5. You will receive a final confirmation containing the estimated shipment date3. Click on Ok to finalize the procedure.

1. For PIN guidelines, please consult the IBKR Knowledge Base.

2. The Security token and the shipment are both free of charge. Nevertheless, when you order your device, we will freeze a small amount of your funds (20 USD). If your device is lost, intentionally damaged, stolen or if you close your account without returning it to IBKR, we will use that amount as a compensation for the loss of the hardware. In any other case, the hold will be released once your device has been returned to IBKR. More details on the IBKR Knowledge Base.

3. For security reasons, the replacement device is set to auto-activate within three weeks from the shipment date. IBKR will notify you when the auto-activation is approaching and when it is imminent.

IBKR Knowledge Base References

- See KB1131 for an overview of the Secure Login System

- See KB2636 for information and procedures related to Security Devices

- See KB2481 for instructions about sharing the Security Login Device between two or more users

- See KB2545 for instructions on how to opt back in to the Secure Login System

- See KB975 for instructions on how to return your security device to IBKR

- See KB2260 for instructions on activating the IB Key authentication via IBKR Mobile

- See KB2895 for information about Multiple 2Factor System (M2FS)

- See KB1861 for information about charges or expenses associated with the security devices

- See KB69 for information about Temporary passcode validity

Cash Sweeps

Background

Underlying the IB Universal account are two separate sub-accounts or segments, one for the securities positions and balances which are subject to the customer protection rules of the SEC and another for the commodities positions and balances which are subject to the customer protection rules of the CFTC. This Universal account structure is designed to minimize the administrative overhead that customers would otherwise be exposed to were they to maintain two distinct accounts (e.g., transferring of cash between accounts, login and order submission through separate accounts, multiple statements, etc.) while preserving the separation required by regulation.

These regulations further require that all securities transactions be effected and margined in the securities segment of the Universal account and commodities transactions in the commodities segment.1 While the regulations allow for the custody of fully-paid securities positions in the commodities segment as margin collateral, IB does not do so, thereby limiting their hypothecation to the more restrictive rules of the SEC. Given the regulations and policies which direct the decision to hold positions in one segment vs. the other, cash remains the only asset eligible to be transferred between the two and for which customer discretion is provided.

Outlined below is a discussion as to the cash sweep options offered, the process for selecting an option as well as selection considerations.

Cash Sweep Options

Customers are provided with 3 sweep options, descriptions for which are provided below:

1. Do not sweep excess funds – under this election, excess cash does not move from one segment to another unless necessary to:

a. Eliminate/reduce a margin deficiency in the other segment;

b. Minimize a cash debit balance and therefore interest charges in a given segment. Note that this is the default option and sole option for account holders having only one of securities or commodities trading permissions.

2. Sweep excess funds into my IB securities account – here, cash balances are only held in the commodities segment to the extent necessary to satisfy the current commodities margin requirement. Any cash in excess of the margin requirement, generated as a result of either an increase in cash (e.g., favorable variation and/or transaction related) or decrease in the margin requirement (e.g., changes in the SPAN risk arrays and/or transaction related) will be automatically transferred from the commodities segment to the securities segment. Note that the account holder must have permissions to trade securities in order to select this option.

3. Sweep excess funds into my IB commodities account – here, cash balances are only held in the securities segment to the extent that they, along with any other securities positions having loan value, are needed to satisfy the current securities margin requirement. Note that the account holder must have permissions to trade commodities in order to select this option.

Other items of note:

- As the Universal account allows for cash balances to be held in a variety of denominations, a hierarchy exists for the purpose of determining which particular currency to transfer first when long balances in multiple currencies exist. In these situations the procedure is to first transfer balances denominated in the Base Currency, then USD and then the remaining long currency balances in order of highest to lowest.

- To minimize the likelihood of one segment incurring a margin deficiency following the sweep of excess cash to the other, the full excess will not be transferred and a buffer equal to 5% of the maintenance margin requirement will be retained. Similarly, to minimize the operational overhead of transferring nominal balances, balances will only be transferred if, after giving effect to the 5% margin cushion, the excess, if any, is not less than 1% of account equity or $200.

- When performing the pre-trade credit check to determine whether an account maintains sufficient equity to support a new order, excess cash maintained in one segment will be considered for trades conducted in the other (although a sweep will not occur until the trade has executed and only if it then remains necessary for margin compliance). Accounts which are designated as a Pattern Day Trader and which are subject pre-trade credit check that takes into account the prior as well as current day's equity should pay particular attention to the Selection Considerations section below.

Selecting a Sweep Option

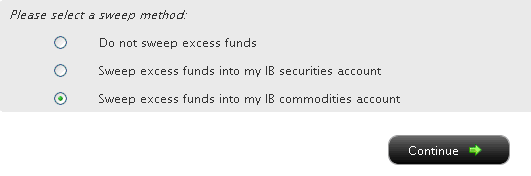

If your Account Management version contains a series of menu options on the left-hand side, select the Account Administration and then Excess Funds Sweep menu options. If your version has menu options across the top, select the Manage Account/Settings and then the Configure Account/Excess Funds Sweep menu options. Regardless of your version, you will be presented with a screen which appears as follows:

You may then select the radio button alongside the option of your choice and select the Continue button. Your choice will take effect as of the next business day and will remain in effect until a different option has been selected. Note that subject to the trading permission settings noted above, there is no restriction upon when or how often you may change your sweep method.

Selection Considerations

While the decision to elect one segment vs. the other for the purposes of maintaining excess cash may involve subjective decisions and preferences unique to each customer (e.g. customer maintains assets which are significant and concentrated in one segment vs. the other), outlined below are several factors warranting consideration:

1. Pattern Day Trading Equity - The securities buying power of accounts designated by regulation as Pattern Day Traders (i.e., 4 or more day trades within a 5 business day period) is limited by the lesser of the current or prior day’s closing equity in the securities segment. As such, an election to sweep excess funds to the commodities segment will prevent the inclusion of such funds in this calculation, thereby potentially limiting the capacity to enter new orders. To maximize the use of equity for purposes of entering securities orders, one would need to elect to sweep excess fund to the securities segment. Note that an election to the securities segment will not impair the ability to enter commodities orders as the pattern day trading rules do not apply to such accounts.

2. Insurance – SIPC protection is afforded to assets in the securities segment and there is no commensurate insurance scheme in place for the commodities segment. That being said, balances in excess of the SIPC $250,000 cash sub-limit ($900,000 Lloyd’s cash sub-limit, where applicable) are not afforded coverage. Customers of IB Canada and IB UK are also subject coverage rules as specified by CIPF and the FSCS, respectively.

3. Interest Income – all other things being equal, customers are likely to receive the most optimal interest income on long cash balances that have not been partitioned between the securities and commodities segments as they are not aggregated for interest credit purposes (since they are subject to distinct segregation pools and reinvestment rules). This, along with the fact that credits require maintenance of a minimum cash balance and that higher balances are afforded preferential rates are factors to be considered when making a sweep election.2

Other Relevant Knowledge Base Articles:

A Comparison of U.S. Segregation Models

A Comparison of U.S. Segregation Models

Footnotes:

1As OneChicago single stock futures are a hybrid product jointly regulated by the SEC and CFTC, they can be purchased and sold in either account type. IB, however, conducts such transactions in the securities segment of the Universal account as this is necessary to provide margin relief between the single stock future and any qualifying stock or option position.

2Consider, for example, an account which maintains a long USD balance of $9,000 in each of the securities and commodities segments. Depending upon the benchmark Fed Funds Effective rate, the account would be eligible to earn interest on $8,000 ($18,000 - $10,000) if the two balances were held in a single segment, but since balances below $10,000 in either of the two segments are not eligible for interest, could not earn anything without electing a sweep option. Similarly, one would be eligible to earn interest at a higher tier if as a result of a sweep election the account holder was then able to achieve a long USD cash balance above $100,000 in a given segment. For additional information regarding interest calculations including a link to current benchmark interest rates, refer to KB39.

Securities Account Protection for Interactive Brokers India Customers

Customer accounts domiciled under Interactive Brokers India Pvt. Limited,(IBI) are awarded different account protection services than our IB-LLC and IB-UK clients. There are two major exchanges, the National Stock Exchange of India (NSE) and the Bombay Stock Exchange (BSE), each one has established their own guidelines for investor grievances against exchange members and/or sub –brokers.

National Stock Exchange of India (NSE)

The NSE has established an Investor Protection Fund with the objective of compensating investors in the event of defaulters' assets not being sufficient to meet the admitted claims of investors, promoting investor education, awareness and research. The Investor Protection Fund is administered by way of registered Trust created for the purpose. The Investor Protection Fund Trust is managed by Trustees comprising of Public representative, investor association representative, Board Members and Senior officials of the Exchange.

The Investor Protection Fund Trust, based on the recommendations of the Defaulters' Committee, compensates the investors to the extent of funds found insufficient in Defaulters' account to meet the admitted value of claim, subject to a maximum limit of Rs. 11 lakhs (1.1 million USD) per investor per defaulter/expelled member.

Bombay Stock Exchange (BSE)

Currently trading is not offered on the BSE by Interactive Brokers.