Informazioni in regime di MiFIR richieste ai titolari di conto non aventi obblighi di segnalazione

Il regime di segnalazione delle operazioni MiFIR richiede alle imprese d'investimento del SEE, come IBUK, di includere i codici identificativi degli specifici clienti nella segnalazione delle operazioni.

I conti che negozino strumenti finanziari supportati da Interactive Brokers (U.K.) Limited (“IBUK”) dovranno essere identificati all'interno dei resoconti di IBUK mediante specifici codici identificativi che potrebbero o meno essere già disponibili per IBUK.

Allo stesso modo, le imprese d'investimento del SEE che fanno uso della piattaforma IB per gli ordini dei propri clienti, e che hanno scelto di effettuare la segnalazione delle operazioni per mezzo di IBUK, dovranno usare gli stessi codici identificativi per gli ordini dei propri clienti. IBUK richiederà ulteriori informazioni ai clienti di tali imprese, al fine di completare la segnalazione delle operazioni.

Queste informazioni dovranno essere fornite a IBUK entro il 30 novembre 2017.

Nuove informazioni richieste

Qualora siano necessarie maggiori informazioni a tal fine, ai clienti sarà richiesto di fornirle mediante la compilazione di un formato elettronico disponibile in Gestione conto.

Le informazioni richieste per questi conti sono le seguenti:

- Tutti i Paesi di cittadinanza delle persone fisiche che siano titolari di conti e trader autorizzati;

- Lo specifico identificatore nazionale delle persone fisiche che siano titolari di conto e trader autorizzati;

- I "Legal Entity Identifiers" ("identificativi del soggetto giuridico" - LEI) delle entità giuridiche. I clienti che non dispongano di un LEI potranno richiederlo tramite IBUK.

- Per i conti delle organizzazioni, sarà necessario indicare se l'entità giuridica è un'entità non finanziaria che impiega il conto per la negoziazione di derivati su commodity al fine della riduzione dei rischi in modo oggettivamente misurabile conformemente all'articolo n. 57 del MiFID II.

Nota: per un elenco delle definizioni e dei termini noti del MiFIR, consultare l'articolo KB2980

LA PRESENTE COMUNICAZIONE È VOLTA A FORNIRE INDICAZIONI ESCLUSIVAMENTE AI CLIENTI CHE EFFETTUINO COMPENSAZIONE TRAMITE INTERACTIVE BROKERS. LE INDICAZIONI NON SI APPLICANO AI CONTI DI SOLA ESECUZIONE.

NOTA: LE INFORMAZIONI SOVRASTANTI NON SONO DA RITENERSI INDICAZIONI ESAUSTIVE OD ONNICOMPRENSIVE, E NON RAPPRESENTANO UN'INTERPRETAZIONE DEFINITIVA DEL REGOLAMENTO, BENSÌ UNA SINTESI DEGLI OBBLIGHI DI SEGNALAZIONE DELLE OPERAZIONI PREVISTI DAL MiFIR.

PRIIPs Regulation

The Packaged Retail and Insurance-based Investment Products Regulation - EU No 1286/2014 (“PRIIPs Regulation” or “PRIIPs”) became applicable on 1 January 2018.

A PRIIP is defined as any investment where the amount repayable to the investor is subject to fluctuations because of exposure to reference values. PRIIPs include ETFs, options, futures, CFDs, structured products, etc.

The Regulation requires product manufacturers to create Key Information Documents (KIDs) and persons advising or selling PRIIPs to provide retail investors based in the European Economic Area (EEA) with KIDs to enable those investors to better understand and compare products. The UK Financial Conduct Authority (FCA) has equivalent requirements for UK residents.

As a broker, IBKR is required to block trading in a PRIIP if a KID is not available.

The objectives of the PRIIPs Regulation.

Since the financial crisis of 2008, one of the main objectives of the European Commission has been to increase consumer protection and rebuild confidence in financial markets.

The Regulation specifies that the Key Information Document (KID) must be prepared in a standardised format.

By defining a standard format and content for the KID, the Regulation aims to:

- Ensure that the information provided is complete and comparable between similar products in order to help investors make informed investment decisions.

- Improve transparency and increase confidence in the retail investment market.

What is a KID?

The KID is a 3-page document that contains important details of the product including general description, cost, risk reward profile and possible performance scenarios.

Who is the regulation applicable to?

The Regulation applies to both PRIIPs manufacturers and distributors. The responsibility to create and maintain the document falls to the product manufacturer. However, any distributor or financial intermediary that sells or provides advice about PRIIPs to a retail investor, or receives a buy order for a PRIIP from a retail investor, must provide the investor with a KID. This also applies to execution-only, online environments.

Who should receive a KID?

Retail investors domiciled in the EEA and the UK should receive a KID prior to investing in a PRIIP. If no KID is available from the manufacturer, the PRIIP will be restricted from trading for EEA and UK retail clients.

Generally KIDs must be provided in an official language of the country in which a client is resident.

However, clients of IBKR have agreed to receive communications in English, and therefore if a KID is available in English all EEA and UK clients can trade the product regardless of their country of residence.

If a KID is not available in English, but one is available in another language, German for example, the PRIIP can only be traded by retail clients who are citizens of, or resident in countries where that language is an official language, in this example Germany, Austria, Belgium, Luxembourg or Liechtenstein.

Special Case – US ETFs

U.S. clients are not impacted by PRIIPs, so the issuers of U.S. listed ETFs do not as a rule create KIDs. This means that EEA and UK Retail clients may not purchase the product. Clients nevertheless have several options:

- Many US ETF issuers have equivalent ETFs issued by their European entities. European-issued ETFs have KIDs and are therefore freely tradable.

- Clients can trade most large US ETFs as CFDs. The CFDs are issued by IBKRs European entities and as such meet all KID requirements.

- Clients may be eligible for re-classification as a professional client, for whom KIDs are not required.

CLIENT CATEGORISATION

We categorize all individual clients as “Retail” by default as this affords clients the broadest level of protection afforded by MiFID. Client who are categorised as “Professional” do not receive the same level of protection as “Retail” but are not subject to the KIDs requirement. As defined under MiFID II rules, “Professional” clients include regulated entities, large clients and individuals who have asked to be re-categorised as “elective professional clients” and meet the MiFID II requirements based on their knowledge, experience and financial capability.

We provide an online step-by-step process that allows “Retail” to request that their categorisation be changed to “Professional". The qualifications for re-categorisation along with the steps for requesting that one’s categorisation be considered are outlined here or, to directly apply for a change in categorisation, the questionnaire is available in the Client Portal/Account Management.

Implications for Interactive Brokers:

In order to meet the PRIIPs Regulation, where required, IB UK will provide KIDs electronically by means of a website (“PRIIPs KID Landing Page”).

Where can I find the PRIIPs KID Landing Page?

The KIDs can be accessed from our designated PRIIPs KID Landing Page. There are three different ways you can find the KIDs. They are available through the IBKR Trader Workstation (“TWS”), the IBKR website and Client Portal.

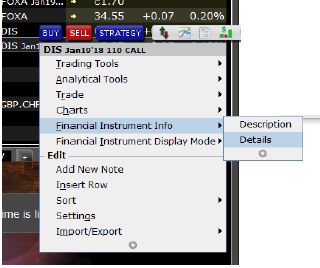

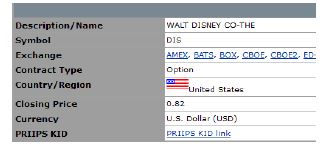

1. Find KIDs through TWS:

- Log into TWS

- Right click on the symbol of the product for which you want the KID.

- Under Financial Instrument Info select Details.

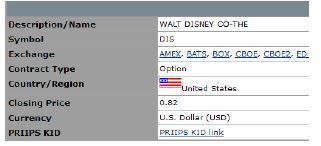

- From the Contract Details page, you can select the PRIIPs KID link. This will take you to our PRIIPs KID Landing Page in Client Portal.

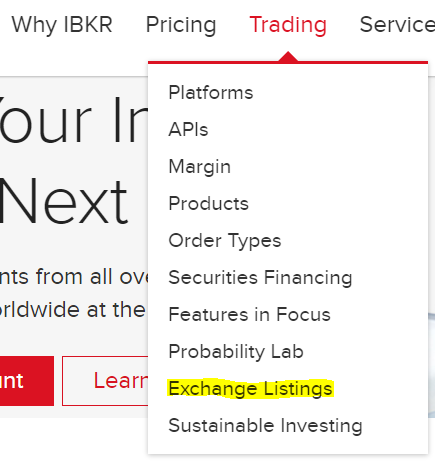

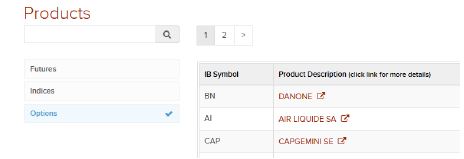

2. Find KIDs through the IBKR website:

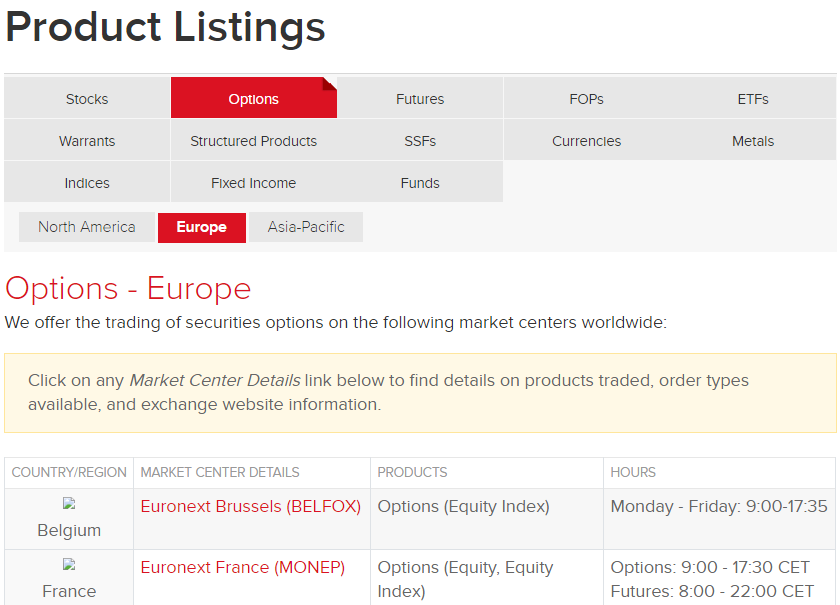

- Open the Trading tab and select Exchange Listings.

- From there, select Product Listings. Select the derivative type, region and exchange of the product for which you would like to find the contract information.

- Select the product you would like to see the KID of, which will take you to the Contract Details page.

- From the Contract Details page, as above, you can select the PRIIPs KID link, which will take you to our PRIIPs KID Landing Page in Client Portal.

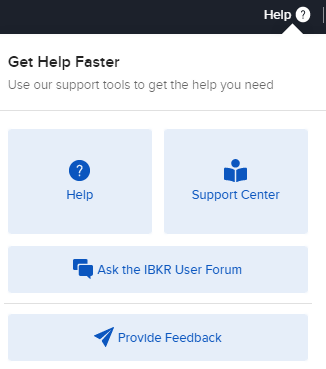

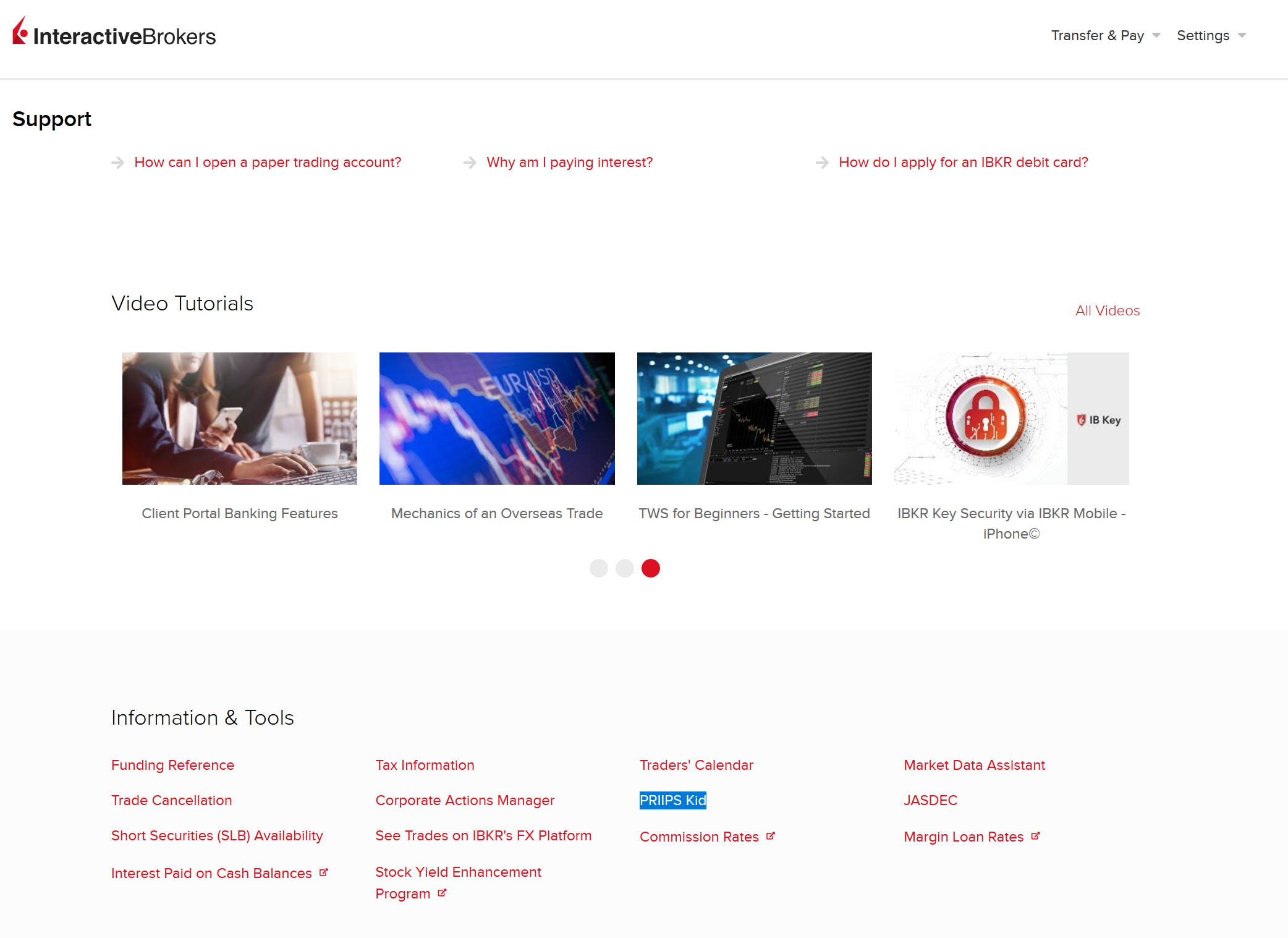

3. Find KIDs through Client Portal:

- Log into Client Portal.

- Click the Help (?) icon followed by Support Center.

- In the Information & Tools section, select PRIIPs Kid, which will take you to our PRIIPs KID Landing Page.

Can I potentially get exposure to a US ETF/other PRIIPs restricted product through a CFD?

An investor could potentially get exposure to a U.S. ETF or other PRIIPs restricted product when trading a CFD (Contract for Difference) as some CFDs are designed to track the performance of underlying assets, including ETFs and other PRIIPs products.

If an investor trades a CFD that is designed to track the performance of a U.S. ETF or other PRIIPs product, the investor may be indirectly investing in that underlying asset. This is because the CFD's value is based on the value of the underlying asset, and any gains or losses in the value of the underlying asset will be reflected in the value of the CFD.

Panoramica della segnalazione delle operazioni in regime di MiFIR

Premessa

A decorrere dal 3 gennaio 2018 entreranno in vigore la nuova direttiva 2014/65/EC ("MiFID II") e il nuovo regolamento (UE) n. 600/2014 ("MiFIR"), introducendo modifiche significative al quadro sulla segnalazione delle operazioni ("Segnalazione delle operazioni nel regime di MiFIR") creato nel 2007 con la direttiva relativa ai mercati degli strumenti finanziari ("MiFID I").

Interactive Brokers (U.K.) Limited ("IBUK") ha implementato un nuovo sistema di segnalazione delle operazioni che consentirà ai clienti di IBUK e del Gruppo Interactive Brokers ("IB Group") con obblighi di segnalazione diretta ai sensi del nuovo regolamento di soddisfare i nuovi requisiti previsti dal MiFIR.

I clienti coinvolti dal nuovo regolamento dovranno provvedere a fornire a Interactive Brokers informazioni aggiuntive per poter continuare l'attività di trading del proprio conto, una volta entrati in vigore i nuovi requisiti in materia di segnalazione a decorrere dal 3 gennaio 2018. Interactive Brokers richiederà le necessarie informazioni in formato elettronico per facilitarne la raccolta.

I clienti coinvolti dovranno fornire le informazioni tempestivamente e non oltre il 30 novembre 2017.

Ambito degli obblighi di segnalazione delle operazioni nel regime di MiFIR

La segnalazione delle operazioni nel regime di MiFIR si applica alle imprese d'investimento dello Spazio economico europeo ("SEE"), come IBUK, ma anche alle imprese d'investimento del SEE che si avvalgono di IBUK o di altre affiliate del Gruppo Interactive Brokers per l'esecuzione degli ordini. In qualità di clienti di IBUK, o di una imprese d'investimento che si avvale della piattaforma IB, si potrebbe essere soggetti alla richiesta di informazioni aggiuntive per consentire l'adeguata trasmissione della segnalazione delle operazioni.

Le imprese d'investimento del SEE hanno l'obbligo di segnalare i dettagli completi e accurati delle operazioni eseguite sugli strumenti finanziari coperti dal MiFIR alla relativa autorità nazionale competente ("ANC") non oltre il termine della giornata successiva.

Il MiFIR ha ampliato l'ambito degli strumenti finanziari segnalabili per coprire quelli negoziati sui mercati regolamentati, sui sistemi multilaterali di negoziazione e sui sistemi organizzati di negoziazione del SEE. In aggiunta alle operazionei eseguite sui mercati del SEE, il MiFIR registrerà anche le operazioni OTC (over-the-counter) e le operazioni sugli strumenti finanziari quotati nel SEE ed eseguiti su sedi di negoziazione non appartenenti al SEE (per esempio titoli azionari quotati sulla Borsa di Londra e negoziati sulla Borsa di New York). (Visualizzare gli strumenti finanziari coperti dal MiFIR).

Soluzioni per la segnalazione delle operazioni in regime di MiFIR per i clienti IB che siano imprese d'investimento: segnalazione dettagliata delle operazioni e segnalazione tramite delega

Ai clienti IB che abbiano confermato di essere imprese d'investimento del SEE soggette agli obblighi di segnalazione delle operazioni previsti dal MiFIR sarà offerta la possibilità di delegare i propri obblighi di segnalazione a IBUK.

Determinate operazione eseguite da queste imprese d'investimento del SEE saranno segnalate da IBUK alla voce obblighi "di segnalazione dettagliata". Per quanto concerne queste operazioni, IBUK completerà i propri resoconti con i dettagli dell'impresa d'investimento, soddisfacendo gli obblighi di segnalazione dell'impresa d'investimento. Le altre tipologie di operazioni saranno segnalate a nome delle imprese d'investimento tramite delega come resoconti separati, in aggiunta a quelli propri di IBUK. I clienti dovranno firmare solamente un accordo con IBUK per la copertura di entrambe le tipologie di segnalazione.

Informazioni oggetto della segnalazione

I campi relativi alla segnalazione sono aumentati da 23, ai sensi del regime di MiFID I, a 65, ai sensi del nuovo regime di MIFIR. I nuovi requisiti informativi ora comprendo, tra le altre cose:

- Identificazione dettagliata dell'acquirente e del venditore di ciascuna operazione. In particolare, il regolamento richiede la presentazione degli identificativi del soggetto giuridico ("Legal Entity Identifiers" - LEI) per le persone giuridiche e gli identificatori nazionali per le persone fisiche (in base al relativo Paese di cittadinanza).

- Identificazione del responsabile decisionale per l'acquirente o il venditore in caso di esercizio discrezionale da parte di terzi:

- Un soggetto diverso dal titolare di un conto individuale o cointestato, o un'entità esterna.

- Una terza parte diversa dai trader autorizzati per il conto di un'organizzazione (es. un consulente finanziario che effettui trading per i conti di secondo livello dei propri clienti).

Questa informazione non è richiesta in caso di titolare del conto che effettui trading di persona o di trader autorizzati effettuino trading per la propria organizzazione.

- Identificazione del soggetto o algoritmo responsabile presso l'impresa che effettua la segnalazione per la decisione d'investimento o l'esecuzione dell'operazione. Queste informazioni sono richieste per le imprese d'investimento del SEE che si avvalgono dei nostri servizi di segnalazione.

- In caso di operazioni in strumenti derivati su materie prime, un'indicazione del fatto che le operazioni di strumenti derivati su materie prime riducano i rischi in una modalità oggettivamente misurabile in conformità con l'articolo n. 57 del MiFID II; ciò è applicabile ai conti delle organizzazioni solamente se il titolare è un'entità non finanziaria.

Questa nuova informazione colpisce i clienti Interactive Brokers in modi diversi a seconda del fatto che il cliente sia un'impresa d'investimento del SEE, o un'organizzazione o un soggetto che non sia un'impresa d'investimento, ma anche a seconda del fatto che gli strumenti finanziari negoziati siano supportati da IBUK o da un'altra affiliata del Gruppo Interactive Brokers.

Implicazioni per i clienti IB non soggetti agli obblighi di segnalazione delle operazioni previsti dal MiFIR

Per poter soddisfare i propri obblighi di segnalazione, IBUK ha l'obbligo di identificare e segnalare il proprio cliente immediato per ciascuna operazione eseguita. La segnalazione deve comprendere i nuovi codici identificativi dei clienti previsti dai regolamenti.

Di conseguenza, IBUK dovrà ottenere e segnalare il codice identificativo del cliente per:

- I clienti diretti di IBUK che detengano un conto per la negoziazione di strumenti finanziari supportati da IBUK;

- I clienti che siano imprese d'investimento del SEE e si avvalgano dei servizi di segnalazione di Interactive Brokers;

- I clienti che siano conti di secondo livello di imprese d'investimento del SEE che si avvalgano della piattaforma Interactive Brokers e utilizzino i nostri servizi di segnalazione.

Consultare l'articolo KB2976 per maggiori dettagli in merito alle informazioni richieste ai titolari di conto che non siano direttamente soggetti al regime di MiFIR.

Nota: per un elenco delle definizioni e dei termini noti del MiFIR, consultare l'articolo KB2980

LA PRESENTE COMUNICAZIONE È VOLTA A FORNIRE INDICAZIONI ESCLUSIVAMENTE AI CLIENTI CHE EFFETTUINO COMPENSAZIONE TRAMITE INTERACTIVE BROKERS. LE INDICAZIONI NON SI APPLICANO AI CONTI DI SOLA ESECUZIONE.

NOTA: LE INFORMAZIONI SOVRASTANTI NON SONO DA RITENERSI INDICAZIONI ESAUSTIVE OD ONNICOMPRENSIVE, E NON RAPPRESENTANO UN'INTERPRETAZIONE DEFINITIVA DEL REGOLAMENTO, BENSÌ UNA SINTESI DEGLI OBBLIGHI DI SEGNALAZIONE DELLE OPERAZIONI PREVISTI DAL MiFIR.

MiFIR Definitions & Terms

European Economic Area (EEA) - As of October 2017, the EEA consists of the following countries: Austria, Belgium, Bulgaria, Croatia, Republic of Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden and the United Kingdom.

Investment Firms - Article 4 (1) (1) of MiFID II defines investment firm as any legal person whose regular occupation or business is the provision of one or more investment services to third parties and/or the performance of one or more investment activities on a professional basis. The investment services and activities covered by the framework are listed in Section A of Annex I of MiFID II.

Transactions Executed - For the purposes of MiFIR Transaction Reporting, a transaction is the conclusion of an acquisition or disposal of one of the financial instruments covered by MiFIR. A transaction is considered to be executed when it resulted from one of the following activities performed by an Investment Firm:

- Reception or transmission of orders in relation to one or more financial instruments (exceptions apply under Article 4 of Commission Delegated Regulation (EU) 2017/590);

- Execution of orders on behalf of clients;

- Dealing on own account;

- Making an investment decision in accordance with a discretionary mandate given by a client;

- Transfer of financial instruments to or from accounts.

[Ref: Articles 2 and 3 of Commission Delegated Regulation (EU) 2017/590]

IB Broker - Accounts that trade financial instruments which are received and/or transmitted by one of the following Interactive Brokers Group entities ("IB Brokers"):

- Interactive Brokers (U.K.) Limited

- Interactive Brokers Central Europe Zrt.

- Interactive Brokers Ireland Limited

Financial Instruments Covered by MiFIR - Article 26 (2) of Regulation (EU) No 600/2014 (MiFIR) lays out the transaction reporting obligation with regard to transactions in financial instruments listed below, irrespective of whether or not such transactions are carried out on the trading venue:

- Financial instruments which are admitted to trading or traded on a trading venue or for which a request for admission to trading has been made;

- Financial instruments where the underlying is a financial instrument traded on a trading venue; and

- Financial instruments where the underlying is an index or a basket composed of financial instruments traded on a trading venue.

The financial instruments covered by this requirement are legally enumerated in Section C of MiFID II:

(1) Transferable securities;

(2) Money-market instruments;

(3) Units in collective investment undertakings;

(4) Options, futures, swaps, forward rate agreements and any other derivative contracts relating to securities, currencies, interest rates or yields, emission allowances or other derivatives instruments, financial indices or financial measures which may be settled physically or in cash;

(5) Options, futures, swaps, forwards and any other derivative contracts relating to commodities that must be settled in cash or may be settled in cash at the option of one of the parties other than by reason of default or other termination event;

(6) Options, futures, swaps, and any other derivative contract relating to commodities that can be physically settled provided that they are traded on a regulated market, a MTF, or an OTF, except for wholesale energy products traded on an OTF that must be physically settled;

(7) Options, futures, swaps, forwards and any other derivative contracts relating to commodities, that can be physically settled not otherwise mentioned in point 6 of this Section and not being for commercial purposes, which have the characteristics of other derivative financial instruments;

(8) Derivative instruments for the transfer of credit risk;

(9) Financial contracts for differences;

(10) Options, futures, swaps, forward rate agreements and any other derivative contracts relating to climatic variables, freight rates or inflation rates or other official economic statistics that must be settled in cash or may be settled in cash at the option of one of the parties other than by reason of default or other termination event, as well as any other derivative contracts relating to assets, rights, obligations, indices and measures not otherwise mentioned in this Section, which have the characteristics of other derivative financial instruments, having regard to whether, inter alia, they are traded on a regulated market, OTF, or an MTF;

(11) Emission allowances consisting of any units recognised for compliance with the requirements of Directive 2003/87/EC (Emissions Trading Scheme).

National Identifiers - Under MiFIR, natural persons must be reported by using specific national identifiers required under a priority order that depends and varies on the Country of citizenship that is identified as relevant under MiFIR. The identifier can be a passport, a national ID card, a tax or personal code or a concatenation of full name and date of birth (“CONCAT”). The IB Broker will only request clients to provide national identifiers that are not already available.

Legal Entity Identifiers (“LEI”) = 20-character unique identifier based on the ISO 17442 for the global identification of legal entities that engage in financial transactions.

Commodity Derivatives Transactions that reduce risk in an objectively measurable way - When reporting transactions in commodity derivatives, the IB Broker will have to specify whether the transaction reduces risk in an objectively measurable way in accordance with Article 57 of Directive 2014/65/EU (“Art 57”). The IB Broker will allow such transactions only from accounts held by entities that are non-financial entities using the account for trades in commodity derivatives that are intended to objectively reduce risk directly relating to their commercial activity in accordance with Art 57. (e.g. company that produces wheat that trades in such derivatives to hedge its commercial activity).

Account holders that make such a declaration in the Trading Permission section of their Account Management, agree that all the transactions executed in commodity derivatives for that account will be executed for reducing the risk under Art 57, and the IB Broker will report the relevant transactions accordingly.

Individual or algorithm responsible at the reporting firm for making the investment decision - Under MiFIR, Investment Firms are required to include in their transaction reports the identification of the individual or algorithm that was primarily responsible for making the investment decision within the firm to acquire or dispose of a financial instrument. Only one individual or algorithm can be identified as responsible with regard to a transaction, and Investment Firms must identify such individual or algorithm as specified in Article 8 of commission delegated regulation (EU) 2017/590.

In accordance with these requirements, your IB Broker has implemented a new section in Account Management and new features in the IB Trader Workstation to allow Investment Firms that report their transactions through an IB Broker to identify individuals and algorithms in compliance with the new obligations.

Individual responsible at the reporting firm for the execution of a transaction - Art 9 of Commission Delegated Regulation (EU) 2017/590 requires Investment Firms to identify individuals or algorithms responsible for determining which trading venue to access […], which firms to transmit orders to or any other condition related to the execution of an order. While this requirement applies only to IB Brokers for the majority of the transactions reports (because the IB Broker is usually the entity that executes the transaction), when an order is submitted by an Investment Firm that transaction reports through an IB Broker via the Delegated Transaction Reporting, the specific user that has submitted the order will be reported as responsible for executing the transaction.

Article 4 of commission delegated regulation (EU) 2017/590 - Transmission of an order

1. An investment firm transmitting an order pursuant to Article 26(4) of Regulation (EU) No 600/2014 (transmitting firm) shall be deemed to have transmitted that order only if the following conditions are met:

(a) the order was received from its client or results from its decision to acquire or dispose of a specific financial instrument in accordance with a discretionary mandate provided to it by one or more clients;

(b) the transmitting firm has transmitted the order details referred to in paragraph 2 to another investment firm (receiving firm);

(c) the receiving firm is subject to Article 26(1) of Regulation (EU) No 600/2014 and agrees either to report the transaction resulting from the order concerned or to transmit the order details in accordance with this Article to another investment firm.

For the purposes of point (c) of the first subparagraph the agreement shall specify the time limit for the provision of the order details by the transmitting firm to the receiving firm and provide that the receiving firm shall verify whether the order details received contain obvious errors or omissions before submitting a transaction report or transmitting the order in accordance with this Article.

2. The following order details shall be transmitted in accordance with paragraph 1, insofar as pertinent to a given order:

(a) the identification code of the financial instrument;

(b) whether the order is for the acquisition or disposal of the financial instrument;

(c) the price and quantity indicated in the order;

(d) the designation and details of the client of the transmitting firm for the purposes of the order;

(e) the designation and details of the decision maker for the client where the investment decision is made under a power of representation;

(f) a designation to identify a short sale;

(g) a designation to identify a person or algorithm responsible for the investment decision within the transmitting firm;

(h) country of the branch of the investment firm supervising the person responsible for the investment decision and country of the investment firm's branch that received the order from the client or made an investment decision for a client in accordance with a discretionary mandate given to it by the client;

(i) for an order in commodity derivatives, an indication whether the transaction is to reduce risk in an objectively measurable way in accordance with Article 57 of Directive 2014/65/EU;

(j) the code identifying the transmitting firm.

For the purposes of point (d) of the first subparagraph, where the client is a natural person, the client shall be designated in accordance with Article 6. For the purposes of point (j) of the first subparagraph, where the order transmitted was received from a prior firm that did not transmit the order in accordance with the conditions set out in this Article, the code shall be the code identifying the transmitting firm. Where the order transmitted was received from a prior transmitting firm in accordance with the conditions set out in this Article, the code provided pursuant to point (j) referred to in the first subparagraph shall be the code identifying the prior transmitting firm.

3. Where there is more than one transmitting firm in relation to a given order, the order details referred to in points (d) to (i) of the first subparagraph of paragraph 2 shall be transmitted in respect of the client of the first transmitting firm.

4. Where the order is aggregated for several clients, information referred to in paragraph 2 shall be transmitted for each client.

Also see:

Overview of MIFIR Transaction Reporting

MiFIR Enriched and Delegated Transaction Reporting for EEA Investment Firms

MiFIR Information Required from Account Holders that do not have Reporting Obligations

MiFIR Information Required from Account Holders that do not have Reporting Obligations

The MiFIR Transaction Reporting regime requires Investment Firms, like your IB Broker, to include specific client identifiers in their transaction reports.

Accounts that trade in financial instruments which are received and/or transmitted by one of the following Interactive Brokers Group entities (“IB Brokers”) will need to be identified in the IB Broker’s reports by using specific identifiers that may or may not be already available to it.

- Interactive Brokers (U.K.) Limited

- Interactive Brokers Central Europe Zrt.

- Interactive Brokers Ireland Limited

Similarly, Investment Firms that use the IB platform for their clients’ orders and have elected to transaction report through their IB Broker will have to use the same identifiers for their client orders. If you are the client of such a firm, your IB Broker may need additional information from you to complete the transaction reports.

Information Required

When additional information is necessary for this purpose, clients will be asked to provide it via the completion of an electronic form available in the Account Management.

The information requested for these accounts is:

- All countries of citizenship for natural persons that are account holders and authorised traders;

- A specific National Identifier for natural persons that are account holders and authorised traders;

- The Legal Entity Identifier for legal entities. Clients that do not have an LEI will be able to apply for one through their IB Broker.

- For organisation accounts, an indication as to whether the Legal Entity is a non-financial entity using the account for trades in Commodity Derivatives Transactions to reduce risk in an objectively measurable way in accordance with Article 57 of MiFID II.

Note: For a listing of common MiFIR definitions and terms, see KB2980

THIS INFORMATION IS GUIDANCE FOR INTERACTIVE BROKERS CLEARED CLIENTS ONLY. THIS GUIDANCE DOES NOT APPLY TO EXECUTION ONLY ACCOUNTS.

NOTE: THE INFORMATION ABOVE IS NOT INTENDED TO BE A COMPREHENSIVE OR EXHAUSTIVE GUIDANCE AND IT IS NOT A DEFINITIVE INTERPRETATION OF THE REGULATION, BUT A SUMMARY OF MiFIR TRANSACTION REPORTING OBLIGATIONS.

MiFIR Enriched and Delegated Transaction Reporting for Investment Firms

Who is Subject to the MiFIR Transaction Reporting Requirements?

All EEA and UK investment firms (collectively, "Investment Firms") are subject to the reporting requirements and will have to report all transactions executed in financial instruments covered by MiFIR within one working day from their execution.

The below entities (“IB Brokers”), will offer assistance to IB clients that are Investment Firms in complying with the new requirements:

- Interactive Brokers (U.K.) Limited

- Interactive Brokers Central Europe Zrt.

- Interactive Brokers Ireland Limited

- Interactive Brokers Luxembourg SARL

With the exception of Omnibus Introducing Brokers, where applicable, that utilise the IB platform (in which all their underlying client positions are held in one or more omnibus accounts), all IB clients that are EEA Investment Firms will be able to elect to have their IB Broker report on their behalf. The IB Broker will report for IB clients based on two distinct reporting mechanisms implemented in accordance with the Regulation: Enriched Transaction Reporting and Delegated Transaction Reporting.

ENRICHED TRANSACTION REPORTING

In compliance with Article 4 of Commission Delegated Regulation (EU) 2017/590, if an IB Broker includes details of orders submitted by clients that are Investment Firms (“the transmitting firm”) in its own transaction reports, the transmitting firm is exempt from reporting these transactions.

Enriched Transaction Reporting will only apply to transactions in financial instruments carried by an IB Broker submitted for execution by an Investment Firm for the benefit of the Investment Firm’s clients (for example, a Financial Advisor, Fund Manager or Introducing Broker Account submitting orders for its clients' subaccounts).

DELEGATED TRANSACTION REPORTING

Delegated Transaction Reporting services are provided by an IB Broker to Investment Firms for all other transactions submitted by the Investment Firm.

This includes transactions entered by the Investment Firm for its own proprietary account, transactions submitted on the basis of discretionary mandates given by their clients and transactions in Financial Instruments for which an IB Broker is not the carrying broker (i.e., any transaction in a financial instrument where another IB affiliate is the carrying broker). Delegated transaction reporting does not apply where the trades are submitted directly by clients of the Investment Firm.

These reports will be submitted to the National Competent Authority (“NCA”) of the Country of legal residence recorded in the Legal Entity Identifier of the account for which the Delegated Transaction Reporting was enabled (e.g., if the Investment Firm’s legal residence is Netherlands, transactions will be reported to the Authority for the Financial Markets (AFM)).

Clients will only need to sign one agreement with an IB Broker to cover both Enriched and Delegated Transaction Reporting.

How to Sign Up for the Enriched and Delegated Transaction Reporting Service

Investment Firms (other than Omnibus Introducing Brokers) will be prompted to complete an electronic form in the Account Management system during which it will be possible to accept to use IB’s Enriched and Delegated Transaction Reporting Service.

Investment Firms that are Omnibus Introducing Brokers on the IB platform will not have the ability to activate the Enriched and Delegated Transaction Reporting.

Investment Firms that utilise IB’s Enriched and Delegated Transaction Reporting Service will need to sign the relevant legal agreement and provide the following information:

- Legal Entity Identifier (“LEI”). Clients that do not have an LEI, will be able to apply for one through an IB Broker;

- The citizenship(s) for each authorised trader and further information as required by the national client identifier requirements for the relevant country;

- Individuals or Algorithms that can be responsible for making the investment decision within the investment firm:

- Individual active traders who have been previously selected as possible investment decision makers within the firm. Only individuals that are authorised as traders on the account will be allowed;

- Algorithm identifiers provided for algorithms that the firm may use for making investment decisions. It is the client’s responsibility to determine and provide algorithm identifiers in compliance with the regulation.

How the New Requirements Will Affect the Account Management and the IB Order Entry System

Some of the information required for the submission of a transaction report may change on an order by order basis, and may require input of the person submitting the trade. Hence, IB has amended IB Account Management and the IB Order Entry System to allow traders to provide the necessary information.

Accounts that want to use IB’s Enriched and Delegated Transaction Reporting Service shall select the authorised traders and list the Algorithm IDs that may be responsible for making an investment decision.

The traders and algorithms listed in Account Management will be displayed in a new dropdown field of the IB Trader Workstation at the time of the order submission. This field will show the default value selected in Account Management of the account. The client will be able to change this by selecting another value present in the dropdown list.

The IB Trader Workstation will allow an authorised trader on the account for which the Enriched and Delegated Transaction Reporting was activated to select one person or algorithm as responsible for the investment decision within the firm with regard to the specific order submitted.

Note: For a listing of common MiFIR definitions and terms, see KB2980

THIS INFORMATION IS GUIDANCE FOR INTERACTIVE BROKERS CLEARED CLIENTS THAT ARE INVESTMENT FIRMS ONLY. THIS GUIDANCE DOES NOT APPLY TO EXECUTION ONLY ACCOUNTS.

NOTE: THE INFORMATION ABOVE IS NOT INTENDED TO BE A COMPREHENSIVE OR EXHAUSTIVE GUIDANCE AND IT IS NOT A DEFINITIVE INTERPRETATION OF THE REGULATION, BUT A SUMMARY OF MiFIR TRANSACTION REPORTING OBLIGATIONS.

Overview of MIFIR Transaction Reporting

Background

On 3 January 2018, a new Directive 2014/65/EC (“MiFID II”) and Regulation (EU) No 600/2014 (“MiFIR”) became effective, introducing significant changes to the transaction reporting (“MiFIR Transaction Reporting”) framework that was created in 2007 with the Markets in Financial Instrument Directive (“MiFID I”).

Interactive Brokers has implemented a new transaction reporting system that will enable clients that have direct reporting obligations under the new Regulation to comply with the new MiFIR requirements.

Scope of MiFIR Transaction Reporting Obligations

MiFIR Transaction Reporting applies to European Economic Area (“EEA”) and United Kingdom ("UK") Investment Firms ("Investment Firms") and also to Investment Firms that use a broker within the IB Group ("IB Group") to execute orders. As a client of an Investment Firm that uses the IB platform, you may be required to provide additional information to allow the proper transaction reports to be filed.

Investment Firms are obliged to report complete and accurate details of transactions executed in financial instruments covered by MiFIR to the relevant National Competent Authority (“NCA”) no later than the close of the next working day.

MiFIR has widened the scope of reportable financial instruments to cover those that are traded on EEA/UK Regulated Exchanges, Multilateral Trading Facilities (“MTFs”) and Organised Trading Facilities (“OTFs”). In addition to transactions executed on EEA/UK exchanges, MiFIR will capture Over the Counter (“OTC”) transactions and transactions of EEA/UK listed financial instruments that are executed on non-EEA/UK trading venues, e.g., a stock listed on the LSE traded on NYSE. (see financial instruments covered by MiFIR).

MiFIR Transaction Reporting Solutions for IB Clients that are EEA Investment Firms: Enriched and Delegated Transaction Reporting

IB clients that have confirmed that they are an Investment Firm subject to MiFIR transaction reporting obligations will be offered the option to delegate their reporting obligations to their relevant IB Broker.

Some transactions executed by these Investment Firms will be reported under “Enriched Reporting” obligations. For these trades the IB Broker will add details about the Investment Firm to its own reports, satisfying the reporting obligations of the Investment Firm. Other transactions will only be reported on behalf of Investment Firms on a delegated basis, as separate reports in addition to the IB Broker's own reports. Clients will only need to sign one agreement with their IB Broker to cover both types of reporting.

Information to Be Reported

The reporting fields increased from 23 under the MiFID I regime to 65 under MIFIR. The new information requirements now include, among other items:

- Detailed identification of the buyer and the seller for each transaction. In particular, the Regulation requires the provision of Legal Entity Identifiers (“LEI”) for legal entities and National Identifiers for natural persons (based on their countries of citizenship).

- Identification of the Decision Maker for the buyer and the seller when a third-party exercises discretion:

- A person other than the account holder on an individual or joint account, or a third-party entity.

- A third-party other than the authorised traders on the account for an organisation account (e.g. a Financial Advisor trading for its clients’ subaccounts).

This information is not required where the account holder is self-trading or where authorised traders are trading for their own organisation.

- Identification of the person or algorithm that is responsible at the reporting firm for making the investment decision or for the execution of a transaction. This information is required for EEA Investment Firms that use our reporting services.

- For Commodity Derivatives Transactions, an indication as to whether such Commodity Derivatives Transactions reduce risk in an objectively measurable way in accordance with Article 57 of MiFID II; This is applicable to organisation accounts only when the holder is a non-financial entity.

The new information affects Interactive Brokers clients in different ways depending on whether the client is an EEA Investment Firm, or an organisation/person that is not an Investment Firm, and also depending on whether the financial instruments being traded are received and/or transmitted by their IB Broker or another Interactive Brokers Group affiliate.

Implications for IB Clients that are not Subject to MiFIR Transaction Reporting Obligations

In order to meet its own reporting obligations, each IB Broker is obliged to identify and report its immediate client for each transaction executed. The reporting must contain the new client identifiers mandated by the Regulations.

Therefore, each IB Broker will need to obtain and report a client identifier for:

- The IB Broker's direct clients that hold an account to trade financial instruments received and/or transmitted by the IB Broker;

- Clients that are EEA Investment Firms and utilise the Interactive Brokers reporting services;

- Clients that are subaccounts of an EEA Investment Firm that uses the Interactive Brokers platform and utilises our reporting services.

See KB2976 for further details on the information required from account holders that are not directly subject to MiFIR.

Note: For a listing of common MiFIR definitions and terms, see KB2980

THIS INFORMATION IS GUIDANCE FOR INTERACTIVE BROKERS CLEARED CLIENTS ONLY. THIS GUIDANCE DOES NOT APPLY TO EXECUTION ONLY ACCOUNTS.

NOTE: THE INFORMATION ABOVE IS NOT INTENDED TO BE A COMPREHENSIVE OR EXHAUSTIVE GUIDANCE AND IT IS NOT A DEFINITIVE INTERPRETATION OF THE REGULATION, BUT A SUMMARY OF MiFIR TRANSACTION REPORTING OBLIGATIONS.

Priorità degli ordini di clienti professionali

Nel quarto trimestre del 2009 determinate Borse delle opzioni statunitensi (CBOE, ISE) hanno applicato disposizioni volte a contraddistinguere gli ordini provenienti da un gruppo di clienti pubblici ritenuti "professionali" (ovvero, soggetti o entità aventi accesso a informazioni e/o risorse tecnologiche che consentono loro di negoziare con le stesse modalità impiegate dagli operatori indipendenti) da quelli dei clienti retail. Secondo quanto previsto da tali disposizioni, tutti i conti dei clienti che non siano operatori indipendenti, e che in un determinato mese immettano una media giornaliera di oltre 390 ordini di opzioni quotate (eseguiti o meno) tra tutte le Borse delle opzioni a vantaggio del/i proprio/i conto/i, saranno classificati come "professionali". Dal momento dell'attuazione iniziale da parte del CBOE e dell'ISE, la maggior parte delle altre Borse delle opzioni statunitensi ha introdotto disposizioni analoghe per contraddistinguere gli ordini aventi provenienza "professionale".

Ai fini della priorità di esecuzione, gli ordini inviati a tali Borse delle opzioni a nome dei clienti ritenuti "professionali" saranno trattati alla stregua degli ordini degli operatori indipendenti; inoltre, saranno soggetti a una commissione di transazione per contratto compresa tra storni di ($0.65) e una tariffa di $1.12 (a seconda della categoria delle opzioni).

I broker sono tenuti a condurre una verifica trimestrale per identificare i clienti che eccedono la soglia dei 390 ordini in ciascun mese di tale trimestre e devono essere classificati come "professionali" per il trimestre successivo. Si prega di notare che, ai fini di tale disposizione, le singole componenti dello spread non sono considerate ordini singoli, bensì ciascun ordine di spread costituisce in sé un ordine unico. IB provvederà a informare i clienti coinvolti da tali disposizioni. Si ricorda, inoltre, che il sistema di indirizzamento SmartRouting di IB è progettato per tenere in considerazione tali nuove commissioni di Borsa al momento della scelta dell'indirizzamento.

Per maggiori dettagli, si prega di fare riferimento ai seguenti link:

Common Reporting Standard (CRS)

The Common Reporting Standard (CRS), referred to as the Standard for Automatic Exchange of Financial Account Information (AEOI), calls on countries to obtain information from their financial institutions and exchange that information with other countries automatically on an annual basis. The CRS sets out the financial account information to be exchanged, the financial institutions required to report, the different types of accounts and taxpayers covered, as well as common due diligence procedures to be followed by financial institutions. For more information about CRS, please visit the OECD website.

Interactive Brokers entities comply with the requirements of CRS as implemented in the jurisdictions where they are located, and report account information to the applicable government authorities. Clients reported by Interactive Brokers under CRS will receive a CRS Client Report in the Client Portal shortly after the reporting deadlines specified below. The CRS Client Report provides an overview of the information that was reported by Interactive Brokers.

- What information is reported under CRS:

- Account number

- Name

- Address

- Tax ID Number

- Tax residency country

- Date of birth

- Year-end account balance

- Gross proceeds (all sales)

- Interest income

- Dividend income

- Other income

- When and where is the information reported:

- Interactive Brokers Australia Pty. Ltd. reports to the Australian Taxation Office (ATO) by July 31.

- Interactive Brokers Canada Inc. reports to the Canada Revenue Agency (CRA) by May 1.

- Interactive Brokers Central Europe Zrt. reports to the National Tax and Customs Administration of Hungary (NAV) by June 30.

- Interactive Brokers Hong Kong Limited reports to the Inland Revenue Department of Hong Kong SAR (IRD) by May 31.

- Interactive Brokers India Pvt. Ltd. reports to the Reserve Bank of India/Central Board of Direct Taxes (RBI/CBDT) by May 31.

- Interactive Brokers Ireland Limited reports to the Office of the Revenue Commissioners of Ireland by June 30.

- Interactive Brokers Securities Japan Inc. reports to the National Tax Agency of Japan (NTA) by April 30.

- Interactive Brokers Singapore Pte. Ltd. reports to the Inland Revenue Authority of Singapore (IRAS) by May 31.

- Interactive Brokers U.K. Limited reports to Her Majesty's Revenue and Customs of the United Kingdom (HMRC) by May 31.

- Additional Notes:

- Information relating to clients of Introducing Brokers is not reported by Interactive Brokers. Introducing Brokers are responsible for their own reporting under CRS.

- Accounts held by Interactive Brokers LLC are not reported under CRS as the United States has not signed the CRS.

SEC Tick Size Pilot Program

Background

Effective October 3, 2016, securities exchanges registered with the SEC will operate a Tick Size Pilot Program ("Pilot") intended to determine what impact, if any, widening of the minimum price change (i.e., tick size) will have on the trading, liquidity, and market quality of small cap stocks. The Pilot will last for 2 years and it will include approximately 1,200 securities having a market capitalization of $3 billion or less, average daily trading volume of 1 million shares or less, and a volume weighted average price of at least $2.00.

For purposes of the Pilot, these securities will be organized into groups that will determine a minimum tick size for both quote display and trading purposes. For example, Test Group 1 will consist of securities to be quoted in $0.05 increments and traded in $0.01 increments and Test Group 2 will include securities both quoted and traded in $0.05 increments. Test Group 3 will include also include securities both quoted and traded in $0.05 increments, but subject to Trade-at rules (more fully explained in the Rule). In addition, there will be a Control Group of securities that will continue to be quoted and traded in increments of $0.01. Details as to the Pilot and securities groupings are available on the FINRA website.

Impact to IB Account Holders

In order to comply with the SEC Rules associated with this Pilot, IB will change the way that it accepts orders in stocks included in the Pilot. Specifically, starting October 3, 2016 and in accordance with the phase-in schedule, IB will reject the following orders associated with Pilot Securities assigned to Test Groups:

- Limit orders having an explicit limit that is not entered in an increment of $0.05;

- Stop or Stop Limit orders having an explicit limit that is not entered in an increment of $0.05; and

- Orders having a price offset that is not entered in an increment of $0.05. Note that this does not apply to offsets which are percentage based and which therefore allow IB to calculate the permissible nickel increment

Clients submitting orders via the trading platform that are subject to rejection will receive the following pop-up message:

The following order types will continue to be accepted for Pilot Program Securities:

- Market orders;

- Benchmark orders having no impermissible offsets (e.g., VWAP, TVWAP);

- Pegged orders having no impermissible offsets ;

- Retail Price Improvement Orders routed to the NASDAQ-BX and NYSE as follows:

- Test Group 1 in .001

- Test Group 2 and 3 in .005

Other Items of Note

- GTC limit and stop orders entered prior to the start of the Pilot will be adjusted as allowed (e.g., a buy limit order at $5.01 will be adjusted to $5.00 and a sell limit at $5.01 adjusted to $5.05).

- Clients generating orders via third-party software (e.g., signal provider), order management system, computer to computer interfaces (CTCI) or through the API, should contact their vendor or review their systems to ensure that all systems recognize the Pilot restrictions.

- Incoming orders to IB that are marked with TSP exception codes from other Broker Dealers will not be acted upon by IB. For example, IB will not accept incoming orders marked with the Retail Investor Order or Trade-At ISO exception codes.

- The SEC order associated with this Pilot is available via the following link: https://www.sec.gov/rules/sro/nms/2015/34-74892-exa.pdf

- For a list of Pilot Program related FAQs, please see KB2750

Please note that the contents of this article are subject to revision as further regulatory guidance or changes to the Pilot Program are issued.