FATCA Procedures - Grantor Trust Tax Information Submission

Overview:

Interactive Brokers is required to collect certain documentation from clients to comply with U.S. Foreign Account Tax Compliance Act (“FATCA”) and other international exchange of information agreements.

This guide contains instructions for a Trust to complete the online tax information and to electronically submit a W-9 or W-8BEN.

U.S. Tax Classification

Your U.S. income tax classification determines the tax form(s) required to document the account.

You must login to Account Management with the trust's primary username to access the Tax Form Collection page.

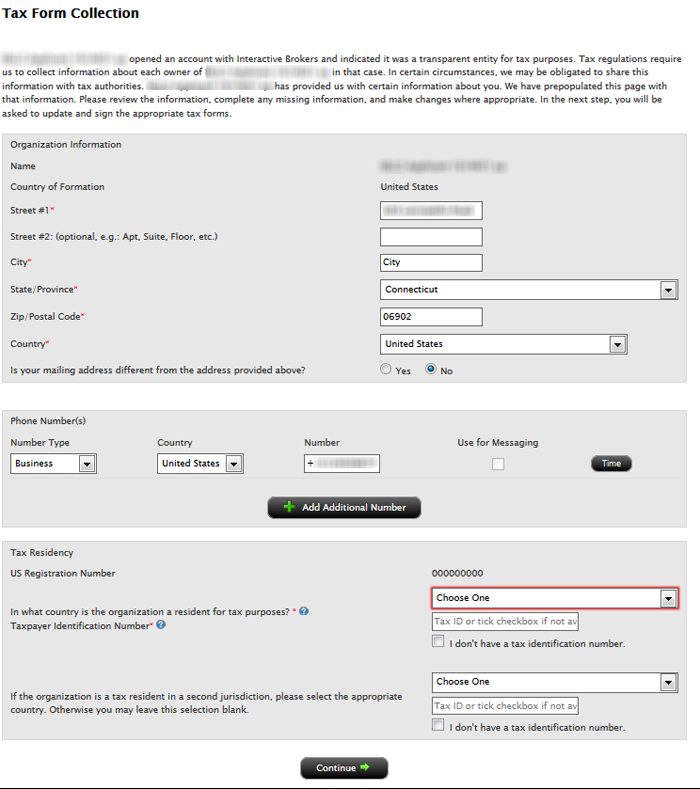

1. Tax Form Collection

The Tax Form Collection page lets account holders review and update important tax-related information and lets account holders electronically fill out an IRS Form W-9 (U.S. taxpayers) and IRS Form W-8 (non-U.S. taxpayers).

Accessing the Tax Form Collection Page

a. Click Manage Account > Account Information > Tax Information > Tax Forms.

b. Click the Update Tax Forms button to access the Collection page.

The Tax Form Collection page opens, displaying a form with tax-related information that should already be completed. (Advisors and brokers can check the status of client updates to this page on the Dashboard Pending Items tab.

c. Review the Trust’s information and update as required.

Confirm the primary tax residency of the trust beside the Tax Residency question, "In what country is the trust a resident for tax purposes?" Select the appropriate country in the drop down menu.

Select in the Tax Residency drop down menu the applicable country.

d. Click Continue.

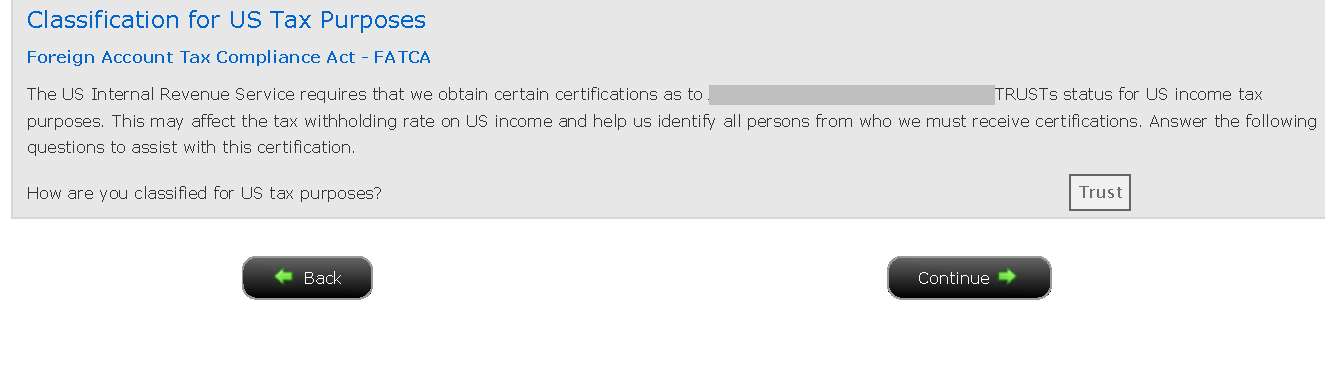

2. Classification for US Tax Purposes

Confirming the Trust’s classification for U.S. purposes

a. Review the Trust’s status by confirming the question, “How are you classified for US tax purposes?” The answer is pre-filled based upon your information completed during the account application process.

b. Click the Continue button to confirm the trust classification and complete the Form W-8 or W-9 for the entity.

c. Click the Continue button to identify each Grantor.

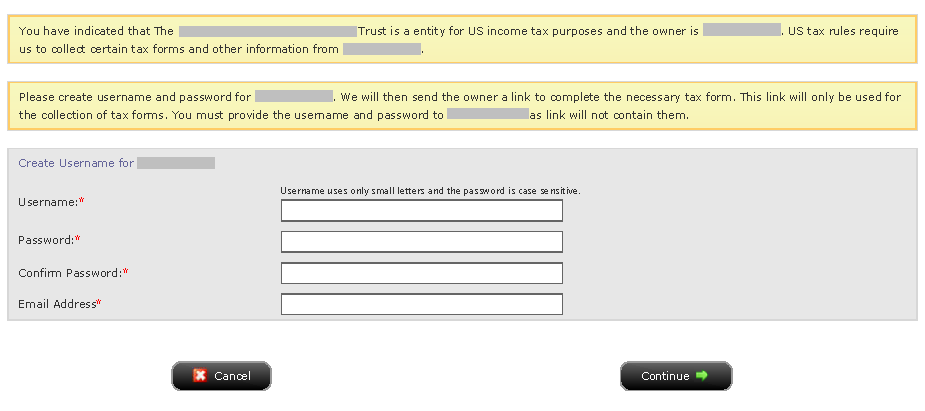

3. Identify Grantors

a. Click Manage Account > Account Information > Tax Information > Tax Forms.

b. Click the Create button beside each grantor to send each user the applicable tax questionnaire and to submit the tax certification form (W-8 or W-9).

Also, update the "Percentage of Ownership" to add up to 100%, if necessary.

.png)

c. Enter the required fields for the username and password for specified grantor and click the Continue button to complete the email delivery of the link.

We will then send the owner a link to complete the necessary tax form. This link will only be used for the collection of tax forms. You must provide the username and password to the Grantor as link will not contain them.

Each Grantor must login with the username/password created and complete the pending tasks by going to Manage Account > Account Information > Tax Information > Tax Forms > Update Tax Forms.

d. Click the Continue button upon creating and sending usernames to each Grantor.

Disclaimer

This guide does not constitute tax or legal advice and Interactive Brokers cannot advise you on how to complete an IRS Forms W-8 or W-9. Instructions are for information purposes only and do not address all possible scenarios. Please consult your tax professional if you are unsure how to complete.

Entity and FATCA Classification for Non-Financial Entities

Introduction

Interactive Brokers (“IB”, “we” or “us”) is required to collect certain documentation from clients (“you”) to comply with U.S. Foreign Account Tax Compliance Act (“FATCA”) and other international exchange of information agreements.

This guide contains a series of flowcharts and accompanying notes that summarize IRS rules relating to:

1. The tax classification for purposes of determining which W-8 or W-9 tax form an entity is required to complete; and

2. The FATCA classification required of entities completing the W-8 tax form (Part I, Section 5).

![]() Note: The flowcharts and notes contained herein do not cover every possible scenario and other scenarios not presented here exist and may more closely align with your situation. You should consult a tax professional regarding your particular circumstances if you are still unsure of your U.S. entity and/or FATCA classification after reading this guide.

Note: The flowcharts and notes contained herein do not cover every possible scenario and other scenarios not presented here exist and may more closely align with your situation. You should consult a tax professional regarding your particular circumstances if you are still unsure of your U.S. entity and/or FATCA classification after reading this guide.

What is NOT Covered in this Guide

The guide is directed to non-U.S. entities that (i) are the beneficial owners of the payments made to the account and (ii) are not financial institutions. This guide does not apply to:

• Individuals (use W-9 or W-8BEN)

• U.S. entities (use W-9)

• Entities acting as an intermediary (such as a nominee, broker, custodian, investment advisor) on behalf of another person (use W-8IMY).

• Non-U.S. Tax-Exempt Organizations and Private Foundations

• Financial Institutions

![]() Note: The U.S. entered into bilateral agreements called Intergovernmental Agreements (IGAs) with many countries regarding the implementation of FATCA. In some cases, the provisions of an applicable IGA could modify the results described in this guide. Entities are covered by an IGA should refer to the IGA and/or consult a tax professional for their filing requirements.

Note: The U.S. entered into bilateral agreements called Intergovernmental Agreements (IGAs) with many countries regarding the implementation of FATCA. In some cases, the provisions of an applicable IGA could modify the results described in this guide. Entities are covered by an IGA should refer to the IGA and/or consult a tax professional for their filing requirements.

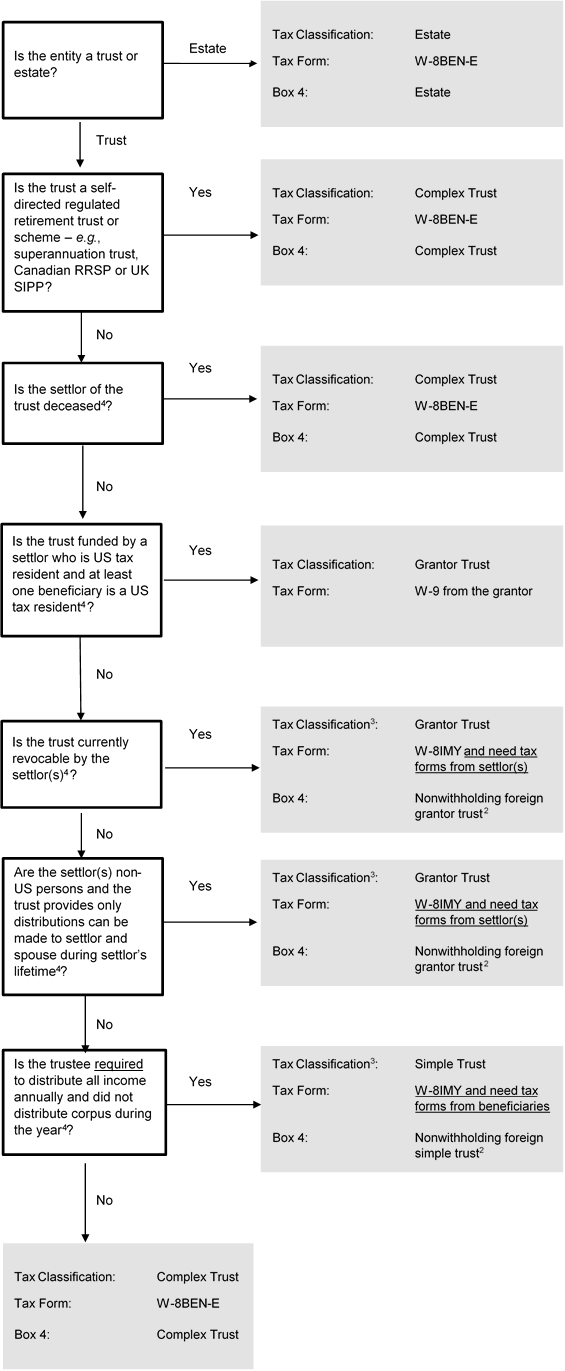

1. U.S. Tax Classification

Your U.S. income tax classification determines the tax form(s) required to document the account. The flow chart below may help you determine your tax classification and the tax form to be completed.

Important: The U.S. imposes income tax on its residents’ worldwide income. On the other hand, nonresidents are only subject to withholding tax on certain limited types of US source investment income (dividends from U.S. companies, etc.). Completion of a W-8 series tax form certifies you are NOT taxable as a U.S. resident. A W-8 form may also be used to claim a reduced rate of withholding tax under a U.S. income tax treaty.

Flowchart for Determining Tax Classification and Required Tax Form (Non-Trust Entities)

.png)

Flowchart for Determining Tax Classification and Required Tax Form (Trusts)

2. FATCA Classification

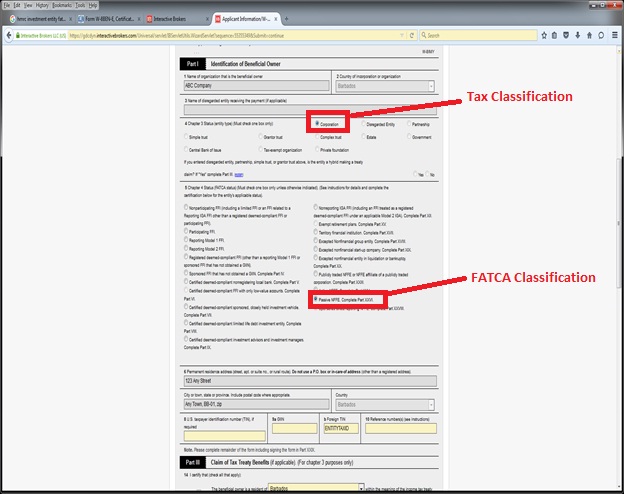

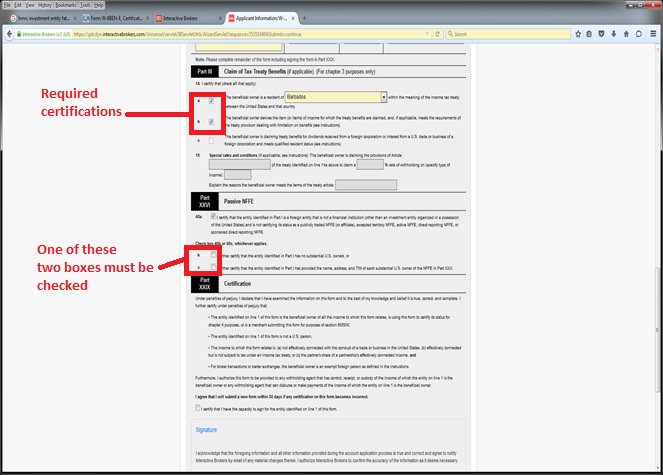

The W8 tax forms are also used to collect FATCA classifications. Many countries have executed “Intergovernmental Agreements (IGA)” with the U.S. requiring its local financial institutions to classify its customers for FATCA purposes. The classification rules under an IGA may not exactly match the classification rules established by the IRS. Other institutions have agreed with the IRS to become FATCA compliant and determine their customers’ FATCA classifications under the IRS rules. We are required to collect this information. The flowchart below applies the IRS default FATCA classification rules and is general in nature. The flowchart is accompanied by sample W-8BEN-E screenshots for a common account structure: a non-U.S. corporation classified for FATCA purposes as a Passive Non-Financial Foreign Entity (NFFE), which qualifies for treaty witholding rates.

![]() Note: It is important to recognize many organizations meet the qualifications for multiple FATCA types and you must select the most appropriate classification. Your specific situation may not fall within the general guidance. We recommend you seek your own independent advice as we are not in a position to make this determination for you and the rules are complex.

Note: It is important to recognize many organizations meet the qualifications for multiple FATCA types and you must select the most appropriate classification. Your specific situation may not fall within the general guidance. We recommend you seek your own independent advice as we are not in a position to make this determination for you and the rules are complex.

Flowchart for Determining FATCA Classification

.png)

Example: A corporation is a common form of entity ownership, involving two or more owners with none having any personal liability for the debts of entity. As outlined in the Tax Classification flowchart above, an entity of this type would be required to complete the W-8BEN-E. Assuming the corporation is not classified as a Foreign Financial Entity (e.g. bank, broker, investment manager, hedge fund, mutual fund, insurance company) as discussed in footnote 5 below, then its FATCA classification would be Passive NFFE. Screenshots of the W-8BEN-E for this sample entity are provided below.

Sample Screenshots - W-8BEN-E (Passive NFFE)

Footnotes

1 The US Internal Revenue Service (IRS) established rules for determining the tax classification of entities formed outside the United States. These rules apply regardless of how the entity is classified in its country of organization or residency.

Generally corporate entities are treated as the beneficial owners of an account and should complete a W-8BEN-E and select “corporation” unless they elect otherwise (discussed below).

IRS regulations assign a default classification to each entity type. This default classification may be overridden by making a filing with the IRS and obtaining an US employer identification number. Certain entities cannot change their classification and are treated as corporations in all events (e.g., Sociedad Anonima, Public Limited Company and Aktiengesellschaft). A complete list may be found at US Treasury Regulation Section 301.7701-2(b)(8).

The IRS default classification usually depends on (i) the number of owners and (ii) whether any owner is personally liable for the debts of the entity based on the organizing statute (i.e., bank guarantees or other contractual agreements by owners are ignored). The following table summarizes the default rules:

|

|

Number of Owners

|

Owners have Limited Liability?

|

|

|||

|

|

Yes?

|

No?

|

|

|||

|

|

1 Owner

|

Corporation

|

Disregarded Entity

|

|

||

|

|

2+ Owners

|

Corporation

|

Partnership

|

|

||

|

|

|

|

||||

Note: Since the entity tax classification of a disregarded entity is determined by its owner, a US disregarded entity may find the flowchart helpful if the owner is a non-US entity.

A fiscally transparent entity (such as a partnership, simple trust or grantor trust) using IRS Form W-8IMY must provide IRS tax forms for all of its beneficial owners (partners in a partnership, beneficiaries for a simple trust and settlors for a grantor trust) for the account to be documented for US tax purposes.

Certain unit investment trusts (generally where there is an ability to vary the investments) are not considered trusts for US tax purposes. These investment trusts are treated in the same manner as a traditional business entity under the rules discussed above (i.e., corporation, partnership or disregarded entity).

Finally, a trust (other than a unit investment trust treated as a business entity) is considered a non-US trust for US tax purposes if (1) a court outside the United States is able to exercise primary supervision over the administration of the trust, and (2) any non-US person has the ability to control (or veto) any “substantial decision” of the trust.

The flowchart assumes that the default entity classification rules apply and the entity is not a per se corporation.

2 A partnership or simple or grantor trust may enter into a withholding agreement with the IRS pursuant to which the partnership or simple or grantor trust agrees to withhold US taxes on the account. The flowchart assumes no withholding agreement was executed.

3 In general, US tax treaty benefits are granted to the beneficial owner of the income determined under US tax principles. For fiscally transparent entities (such as partnerships, simple or grantor trusts or disregarded entities), this means the owners of the entity, NOT THE ENTITY ITSELF, claim US tax treaty benefits. These benefits are claimed on the beneficial owners’ W8 tax forms. However in certain limited cases, an entity may be considered fiscally transparent for US tax purposes but not fiscally transparent by the country with which the US has an income tax treaty. This type of an entity is called a “hybrid entity.” In certain cases, a hybrid entity, not the owners, may claim US tax treaty benefits if the hybrid entity meets the so-called qualified resident test under the applicable tax treaty. A qualifying “hybrid entity” claims the benefits of a US tax treaty by providing a Form W-8BEN-E, in addition to the form required by the flowchart. Importantly, electing hybrid status does not eliminate the need to document all beneficial owners. We note it is unusual for a hybrid entity to claim treaty benefits. The more common scenario is the beneficial owners claim treaty benefits on their tax forms.

4 The rules for classifying trusts are difficult and complex. The flowchart applies generalized rules only. There are many nuances to be considered when classifying a trust which are not addressed in the flowchart. For example, simple trusts cannot have charitable beneficiaries.

5 What is a foreign financial institution for FATCA purpose?

The various FATCA classifications can be broken down into two major categories: foreign financial institutions (FFI) and non-financial foreign (NFFE). Very generally, a financial institution is an entity that is a:

• Depository Institution

• Custodial Institution

• Investment Entity

• Insurance Company that issues certain cash value insurance or annuity contracts.

An FFI typically is required to register with the IRS, obtain a Global Intermediary Identification Number and report on its customers / owners to the appropriate tax authorities. If the entity does not meet the definition of a Financial Institution, it is considered an NFFE and covered by this guide book.

Subject to variations under IRS regulations and intergovernmental agreements:

• a Depository Institution is an institution that accepts deposits in the ordinary course of a banking or similar business. This includes banks and credit unions.

• a Custodial Institution is an institution which holds financial assets for the account of others as a substantial portion of its business. This includes brokers, custodial banks, trust companies, clearing organizations, etc.

• an Investment Entity is any entity if either

(i) the entity generates 50%+ of its gross income from (i) trading in money market instruments, foreign currency, transferrable securities, interest rates, futures, etc.; (ii) portfolio management or (iii) otherwise investing, administering or managing funds or financial assets on behalf of other persons (generally, broker-dealers and investment managers);

or

(ii) 50%+ of the entity gross income is attributable to investing, reinvesting, or trading in financial assets AND it is managed by a Financial Institution (mutual funds, hedge funds, and collective investment vehicles are examples);

or

(iii) the entity holds itself out as an entity created to invest, reinvest, or trade invest in financial assets (mutual funds, hedge funds, and collective investment vehicles are examples).

An individual cannot be an FFI. Thus, an organization managed by a professional individual investment advisor (as opposed to an employee of an organization) would not be considered an Investment Entity under (ii) above because it is not managed by a financial institution.

Trusts, family investment companies and funds may fall within the definition of an Investment Entity when they are professionally managed by a financial institution – i.e. where a financial institution handles the day-to-day functions of the entity or has discretionary authority over the fund.

Example: Individual created a non-US Trust A and appoints X, a non-US bank or other financial institution, as the trustee. X, as trustee, is responsible for the management and administration of Trust A. Trust A is an Investment Entity and a Foreign Financial Institution because it is managed by a Foreign Financial Institution.

Example: Individual created a non-US Trust A and appoints Y, an individual professional manager, as the trustee. Y, as trustee, is responsible for the management and administration of Trust A. Trust A is not an Investment Entity or a Foreign Financial Institution because it is not managed by a Foreign Financial Institution. Individuals cannot be financial institutions.

6 The IRS has a list of countries with which it has executed intergovernmental agreements (IGAs) to authorize the implementation of FATCA in that jurisdiction. The list of IGAs can be found at https://www.treasury.gov/resource-center/tax-policy/treaties/Pages/FATCA....

7 See #4 for the definition of Financial Institution. An organization that is not considered a financial institution is considered a non-financial foreign entity (NFFE). There are 3 types of NFFEs; Excepted, Active and Passive. An Active NFFE is an operating business where less than 50% of (i) its gross income is considered passive income and (ii) its average assets are held for the production of passive income. Any NFFE that is not Excepted or Active is a Passive NFFE and must provide us with a certification of its substantial US owners (if any) – generally 10%+ direct or indirect ownership. Some IGAs modify the means of substantial US owners and refer to them as Controlling Persons.

8 Other possible choices include nonfinancial group entity, excepted nonfinancial start-up company, excepted non-financial entity in liquidation or bankruptcy, publicly traded NFFE or sponsored NFFE. See the instructions to the W-8 for further information.

Disclaimer

This guide does not constitute tax or legal advice and Interactive Brokers cannot advise you on how to complete IRS Forms W-8. Examples included in this guide are for illustration only and do not address all possible scenarios. Please consult your tax professional if you are unsure how to complete IRS Forms W-8.

FATCA FAQs - Issues Involving Mismatch Between Tax Treaty Country and Address

FATCA related FAQs involving mismatches between tax treaty country and address. See KB2601 for other FATCA related FAQ topics.

Q1: I claimed treaty benefits in one country but have an address outside that treaty country. Why did I receive an email asking for additional documentation?

A1: We are required to verify your connection with the treaty country since you also have an address outside that country. We can process your claim for treaty benefits if you provide one document from Category (A) AND one document from Category (B) below.

|

Category (A)

|

AND

|

Category (B)

|

|

ANY OF the following unexpired documents issued by the treaty country:

|

ANY OF the following documents that match your address in the treaty country:

|

|

|

· Driver’s license

|

· Driver’s license

|

|

|

· Passport

|

· Bank or brokerage statement*

|

|

|

· National identity card

|

· Utility bill*

|

*Bank or brokerage statements and utility bills must be less than 12 months old. Alternatively, if you cannot provide documents from both categories, please provide a written explanation as to why you are entitled to treaty benefits together with any supporting documentation. Note: we may request further information or documentation from you depending on the explanation provided.

Q2: I submitted a proof of address and I received an email that the document submission did not resolve the issue. Why?

A2: Please confirm that the proof of identity you submitted was issued by the treaty country and that the proof of address relates to your address in the treaty country. A proof of address document alone is not sufficient to resolve the matter. Sometimes, customers inadvertently submit documentation for the other address. Please check the date of the proof of address document. We can only accept documents dated less than 12 months old. Also confirm you submitted a proof of identity document from the treaty country.

Q3: I live in Hong Kong and chose China as my tax treaty country on my Form W-8BEN. I received a notification saying the proof of address and proof of identity I submitted was not sufficient to claim benefits under the U.S.-China tax treaty. Hong Kong is a Special Administrative Region of the People’s Republic of China, so the U.S.-China tax treaty applies to it, correct?

A3: No. According to the US Internal Revenue Service, the U.S.-People’s Republic of China tax treaty does NOT apply to Hong Kong. Unless you can provide a proof of address and identity in the People’s Republic of China or provide other evidence that you are a tax resident of People’s Republic of China, you may not claim Chinese tax treaty benefits.

Q4: I live in Macau and chose China as my tax treaty country on my Form W-8BEN. I received an e-mail saying that the proof of address I submitted for my Macau address was not sufficient to claim benefits under the U.S.-China tax treaty. Macau is a Special Administrative Region of the People’s Republic of China, so the U.S.-China tax treaty applies to it, correct?

A4: No. According to the U.S. Internal Revenue Service, the U.S.- People’s Republic of China tax treaty does NOT apply to Macau. Unless you can provide a proof of address and identity in the People’s Republic of China or provide other evidence that you are a tax resident of People’s Republic of China, you may not claim Chinese tax treaty benefits.

Q5: I live in Taiwan, ROC and chose China as my tax treaty country on my Form W-8BEN. I received an e-mail saying that the proof of address I submitted for my address in Taiwan, ROC was not sufficient to claim benefits under the U.S.-China tax treaty. Taiwan, ROC is formally known as the Republic of China, so the U.S.-China tax treaty applies to it, correct?

A5: No. According to the US Internal Revenue Service, the U.S.- People’s Republic of China tax treaty does NOT apply to Taiwan, ROC. Unless you can provide a proof of address in People’s Republic of China or provide other evidence that you are a tax resident of People’s Republic of China, you may not claim Chinese tax treaty benefits.

Q6: The information you have in your master file is out-of-date. I moved so that the address you identified as outside the treaty country is incorrect. What should I do?

A6: The fastest and most effective way to remedy the situation is to provide the requested information (see FAQ#1 above) so that our records are complete. You should also log into Account Management and make any required changes to your personal information.

We do not provide tax advice. Please consult your tax advisor for advice in completing tax forms and determining your taxpayer status.

FATCA FAQs - Issues Involving U.S. Address or Telephone Number

FATCA related FAQs involving U.S. address or telephone number. See KB2601 for other FATCA related FAQ topics.

Q1: I received a notification that a review of my file indicated a U.S. address or telephone and additional information is required. What additional information do I need to provide?

A1: You need to provide one document from Category (A) AND one document from Category (B) from the table below AND a written explanation explaining the U.S. address.

|

Category (A)

|

AND

|

Category (B)

|

AND

|

Category (C)

|

|

ANY OF the following documents issued by a non-US country:

|

ANY OF the following documents that match your foreign address:

|

A reasonable written explanation supporting your claim of non-US status.

|

||

|

· Driver’s license

|

· Driver’s license

|

|||

|

· Passport

|

· Bank or brokerage statement*

|

|||

|

· National identity card

|

· Utility bill*

|

*Bank or brokerage statements and utility bills must be less than 12 months old.

Q2: The day count table on the account application says I am a U.S. tax resident and will not let me complete IRS Form W-8. What should I do?

A2: The US Internal Revenue Service generally considers individuals who spend a significant number of days in the United States each year to be U.S. taxpayers. The table flags customers who exceed those IRS rules for U.S. income tax residency and requires a W-9. Alternatively, it may be possible for you to satisfy the “closer connection test” or utilize a U.S. tax treaty to avoid U.S. tax residency. Please refer to IRS Publication 519 for details or consult a tax professional regarding IRS rules for counting days, the closer connection test and U.S. tax treaties.

Q3: I am a studying in the U.S. and present on an F-1 visa. I responded to your email and provided a copy of my F-1 visa. I received an email saying my response was insufficient to resolve the issue. Why?

A3: Please check the expiration date of your visa. If your visa has expired, please provide other evidence of your status, such as an Optional Practical Training (OPT) card, a copy of Form I-20 endorsed by the DSO for your school or another Employment Authorization Document (EAD). Also confirm you submitted the necessary proof of identify and address documentation.

Q4: I use my daughter’s address to receive all mail. She lives in the United States. What should I do?

A4: In this case, you can probably satisfy the substantial presence test noted in the notification you've received . Please provide the number of days you spent or plan to spend in the U.S. in the current and prior two years (e.g., 2015, 2014 and 2013). Also refer to the documentation requirements outlined in FAQ#1 above.

Q5: The address or telephone you noted in your email is out-of-date. I have since moved out of the United States. What should I do?

A5: The fastest and most effective way to remedy the situation is to provide the information as requested in the notification you've received (see FAQ#1 above), so that our records are complete. You should also log into Account Management and make any required changes to your personal information of record.

We do not provide tax advice. Please consult your tax advisor for advice in completing tax forms and determining your taxpayer status.

FATCA FAQs - Issues Involving U.S. Passport or Other Evidence of U.S. Citizenship

FATCA related FAQs involving U.S. passport or other evidence of U.S. citizenship . See KB2601 for other FATCA related FAQ topics.

Q1: I received a notification saying a review of my file indicated I am a U.S. citizen. I am being asked to complete IRS Form W-9 and provide a U.S. Social Security Number. I am not a U.S. citizen. What should I do?

A1: In most cases you received this message because our review of your file indicated you had U.S. citizenship or a U.S. place of birth, which likely infers automatic U.S. citizenship and U.S. taxpayer status even if you do not live in the U.S. or hold a U.S. passport. US citizens are required to provide us with IRS Form W-9 and a valid social security number. Nevertheless, we may accept IRS Form W-8 from you to establish your status as a non-U.S. taxpayer if you provide us with a copy of your Certificate of Loss of Nationality of the United States (Form DS-4083) and a copy of your passport evidencing citizenship in another country. Alternatively, you may provide us with a written explanation of why you are not a U.S. citizen (for instance, you were born in the United States to parents who were fully-accredited foreign diplomats). We may request further information from you depending on the explanation provided.

Q2: I gave up my U.S. citizenship. What should I do?

A2: Please provide us with a copy of your Certificate of Loss of Nationality of the United States (Form DS-4083) and a copy of your passport from another country.

We do not provide tax advice. Please consult your tax advisor for advice in completing tax forms and determining your taxpayer status.

FATCA FAQs - Issues Involving U.S. Green Card Holders

FATCA related FAQs involving U.S. Green Card Holders. See KB2601 for other FATCA related FAQ topics.

Q1: I have a U.S. Green Card but am not a U.S. taxpayer. What additional information or documentation do I need to provide to ensure you can accept my Form W-8BEN?

A1: In general, all U.S. Green Card holders are U.S. taxpayers, even if they do not live in the United States (and even if their Green Card has expired or is otherwise invalid). In general, a U.S. Green Card holder cannot provide Form W-8BEN, and must provide Form W-9 instead. If you are a former U.S. Green Card holder who gave up your U.S. Green Card, you will need to provide a copy of your Form I-407 (Record of Abandonment of Lawful Permanent Resident Status.

Q2: I used to have a U.S. Green Card but gave it up. What additional information or documentation do I need to provide to ensure you can accept my Form W-8BEN?

A2: You will need to provide a copy of your Form I-407 (Record of Abandonment of Lawful Permanent Resident Status).

Q3: I have a U.S. Green Card but it expired. I received notification asking me provide a reasonable written explanation as to why I am a non-U.S. taxpayer despite having a Green Card. I responded that my Green Card is expired but received an email saying my response was insufficient to resolve the issue. Why?

A3: Even if your Green Card has expired for immigration purposes (that is, you cannot use it to enter the United States), tax rules, generally, provide you remain a U.S. taxpayer until you formally renounce your U.S. Green Card. Generally, a U.S. Green Card holder cannot provide Form W-8BEN, and must provide Form W-9 instead. If you did formally renounce your US Green Card, please provide a copy of your Form I-407 (Record of Abandonment of Lawful Permanent Resident Status).

We do not provide tax advice. Please consult your tax advisor for advice in completing tax forms and determining your taxpayer status.

FATCA FAQs - Issues Involving U.S. Place of Birth

FATCA related FAQs involving U.S. Place of Birth. See KB2601 for other FATCA related FAQ topics.

Q1: I was born in the United States but I do not have a U.S. passport and am not a U.S. taxpayer. Why am I being asked for additional documentation?

A1: In most cases, you automatically acquired U.S. citizenship when you were born in the United States even if you have never applied for a passport. U.S. tax rules designate all U.S. citizens as U.S. taxpayers, even those that did not live in the U.S. or receive a U.S. passport. U.S. citizens are required to provide us with IRS Form W-9 and a valid taxpayer ID (e.g. Social Security Number). Nevertheless, we may accept IRS Form W-8 from you to establish your status as a non-U.S. taxpayer if you provide us with a copy of your Certificate of Loss of Nationality of the United States (Form DS-4083) and a copy of your passport evidencing citizenship in another country.

Alternatively, you may provide us with a written explanation of why you are not a U.S. citizen (for instance, you were born in the United States to parents who were fully-accredited foreign diplomats). We may request further information from you depending on the explanation provided.

Q2: I was born in the United States but I am not a U.S. taxpayer. I do not have a Certificate of Loss of Nationality of the United States (Form DS-4083). What should I do?

A2: In general, you are a U.S. citizen and U.S. taxpayer if you were born in the United States. Unlike many jurisdictions, the U.S. taxes its citizens regardless of where they live (or even if they have never lived in the United States). We cannot accept IRS Form W-8 from a U.S. citizen, and must receive a Form W-9 instead. If you are a former U.S. citizen who gave up your citizenship, please refer to the FAQ above for the additional information and documentation you may need to provide to establish your status as a former U.S. citizen.

We do not provide tax advice. Please consult your tax advisor for advice in completing tax forms and determining your taxpayer status.

FATCA FAQs - General

General FAQs involving FATCA . See KB2601 for other FATCA related FAQ topics.

Q1: I am not a U.S. taxpayer. Why do I have to submit IRS Form W-8?

A1: IRS Form W-8 is used to certify your status as a non-U.S. taxpayer. It is also used to claim reduced tax withholding on dividends and other income paid with respect to U.S. securities. Without proper documentation, brokers may be required to impose exceptional withholding tax on transactions occurring in the account and/or report the account as noncompliant to tax authorities.

Q2: I submitted IRS Form W-8. Why do I have to submit additional documentation?

A2: In certain cases, the IRS Form W-8 you submitted is insufficient to establish your status as a non-U.S. taxpayer. This often occurs when certain U.S. connections are found to be associated with your account (e.g., U.S. mailing or permanent address, U.S. telephone number, U.S. place of birth, citizenship or Green Card). The presence of these U.S. connections requires us to collect additional documentation before we can designate you as a non-U.S. taxpayer.

Q3: I am an existing client. Why did I receive a request for additional documentation to support my tax status?

A3: We will request additional documentation from existing clients if:

· Your account details show any U.S. connections (e.g., U.S. mailing or permanent address, U.S. telephone number, U.S. place of birth, citizenship or Green Card) or an address outside the country you identified on your IRS Form W-8 for purposes of claiming treaty benefits; or

· Our records show you moved or otherwise experienced a change of circumstance with respect to your account;

Q4: I was asked to submit a proof of identity document and a proof of address. I provided that information when I opened my account. Isn’t that sufficient to resolve this issue?

A4: It is necessary for us to have current information on our clients. Expired or out-of-date documents cannot be accepted. Please make sure all documentation you submit is legible, has not expired and all proof of address documentation is less than 12 months old. It is important that you promptly respond to our requests for documentation so that the correct withholding rate is applied to your account.

Q5: I responded to your email and provided the requested documents. Now I received an email saying my response was insufficient to resolve the issue. Why?

A5: We cannot accept proof of address documentation that is more than 12 months old or which is nor legible. Please verify that the proof of address document submitted, such as a bank or brokerage statement or a utility bill, is less than 12 months old. You should also confirm you submitted all required documentation. In certain cases, the documentation must be submitted from the country with which you claimed treaty benefits or tax residency to be acceptable.

Q6: I do not wish to submit any additional documentation or complete a new IRS Form W-8. What will happen if I do not respond?

A6: It is imperative you response to the email request with appropriate documentation. Failure to do so may result in exceptional U.S. tax withholding being imposed on your account, reporting of your account to tax authorities and other remedial measures.

Q7: The information in your records is incorrect. I have no connection to the U.S. What can I do to remedy this situation?

A7: It is not uncommon for a client to have changes to their tax residency, which they have not informed us about, thereby resulting in out-of-date or inaccurate records. In these situations, the quickest and most effective way to remedy the situation is to provide the requested information so that our records are complete. You should also log into Account Management and make any required changes.

We do not provide tax advice. Please consult your tax advisor for advice in completing tax forms and determining your taxpayer status.

Index of FATCA Related FAQs

Outlined below are links to a series of FATCA related FAQs organized by topic. For a general overview of FATCA, please see KB1986.

1. General (See KB2602)

2. Issues Involving U.S. Place of Birth (See KB2603)

3. Issues Involving U.S. Green Card Holders (See KB2604)

4. Issues Involving U.S. Passport or Other Evidence of U.S. Citizenship (See KB2605)

5. Issues Involving U.S. Address or Telephone Number (See KB2606)

6. Issues Involving Mismatch Between Tax Treaty Country and Address (See KB2607)

We do not provide tax advice. Please consult your tax advisor for advice in completing tax forms and determining your taxpayer status.

IB Tax Form Users Guide

Introduction

This Users Guide is intended to assist introducing brokers with answering questions your clients may have when completing the online IB Tax Form. Individual and joint accounts having tax information requiring update will be presented with the form immediately upon login to Account Management. For joint accounts, each account holder needs to provide his or her personal information and complete an appropriate tax form. Organization and trust accounts will complete the form through an updated online account application made available through your Account Management Dashboard. Applicable sections of the form will be pre-populated with information on record and the form should therefore only take a few minutes to complete. Completion of the form in a timely manner is critical to ensuring that both U.S. and non-U.S. taxpayers are not subject to any exceptional U.S. tax withholding and non-U.S. taxpayers receive the most favorable rate on dividend withholding as defined by U.S. treaties. As a result, the form cannot be by-passed upon client login and no other Account Management functions will be accessible until completed.

To notify your clients about this online Tax Form and request that they log into Account Management to complete it, sample communication templates suitable for sending to each of your U.S. (Exhibit I) and Non-U.S. (Exhibit II) clients have been included in the Exhibit section of this document. Note that once the Tax Form has been completed, it will be reviewed by IB for purposes of verifying the client’s stated tax residency which, depending upon the information submitted, may require the client to complete additional tasks (e.g., explain responses or send supporting identity and/or address documentation). As IB will have no direct communication with your clients as part of this process, you will need contact the client to complete these additional tasks and forward required documentation to fatca@interactivebrokers.com. To assist you with managing communications and tracking status, IB will be sending periodic reports to your Message Center listing any clients having tasks pending completion and the nature of those tasks.

IB Tax Form Screen Overview

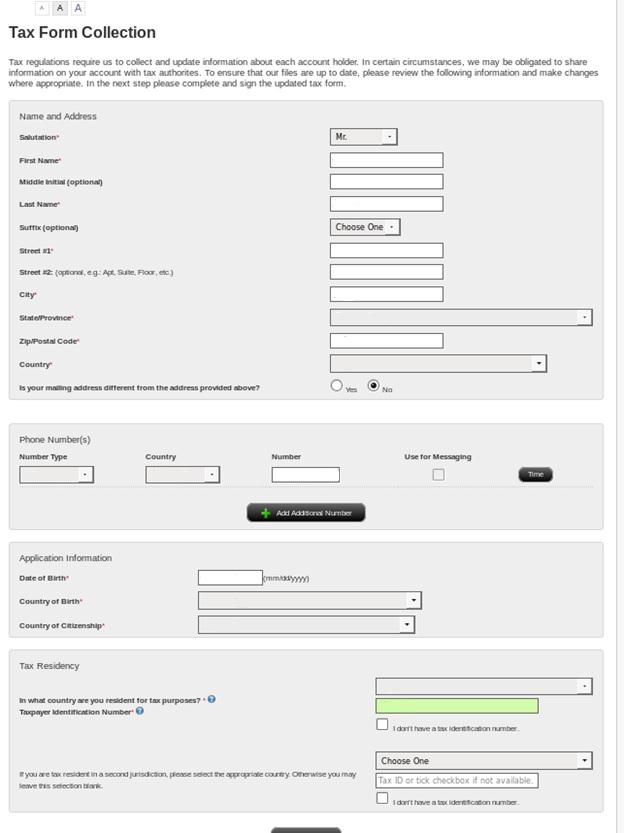

Screen 1

The first screen which the client will be presented upon login to Account Management contains basic account identifying information provided by the client at the point of application or updated through Account Management thereafter. The information presented is as follows:

Section 1: Name and Address – the Salutation, First Name, Middle Initial, Last Name and Suffix fields are pre-populated and cannot be changed on this form. If any of this information has changed, please continue with form and when complete navigate to the Settings, Account Settings and Profile sections to make changes. Changes to permanent and mailing address and telephone number are allowed.

Warning! Certain changes will require verification documents from the client.

Note: The presence of (i) U.S. telephone number and no non-U.S. number, (ii) a U.S. address (mailing or permanent), or (iii) U.S. place of birth are considered U.S. tax connections. Explanations and further follow up documentation from the client are required when these connections are found.

The presence of an address in Jersey, Isle of Mann, Guernsey and Gibraltar is UK indicia flag if the client does not indicate tax residency in the corresponding country. Explanation and further follow up documentation may be required from the client.

Section 2: Phone Number(s) – allows update and addition of phone numbers by type (home, work, mobile fax). For each number entered, specify country of issuance and number. If phone type is mobile and you which to receive test messages check “Use for Messaging” box. An optional entry for preferred times of contact may be specified by clicking on the Time button.

Note: We understand that many clients us a U.S. mobile number for simplicity and ease of communication. While understandable, failure by the client to provide a secondary, non-U.S. telephone number will result in the account being flagged for further review.

Section 3: Application Information - Date of birth, country of citizenship and country of birth will be prepopulated if IB has this information on file. These are required fields which require client entry to proceed.

Note: U.S. citizenship is considered a U.S. tax connection and requires disclosure of U.S. tax residency and a social security number.

U.S. place of birth is considered a U.S. connection if the client does not indicate U.S. citizenship. Explanation and further follow up documentation from the client is required when this connection is found.

Section 4: Tax Residency - The client must disclose the jurisdictions where the client is tax resident and the tax id associated with that residency if applicable. The second tax jurisdiction is an optional field although entries which are clearly erroneous will not be accepted. Additionally, we have programmed rules for the collection of tax ids in certain countries. For example a U.S. social security number has 9 digits and all are numbers. If a client fails the logic, the system will not accept the tax id. If the client is having a problem inserting tax ids, this could be the reason.

Client should hit “Submit” button after all personal information is completed. Assuming no entry errors have been made, the client will be directed to Page 2 (tax form).

Screen 1

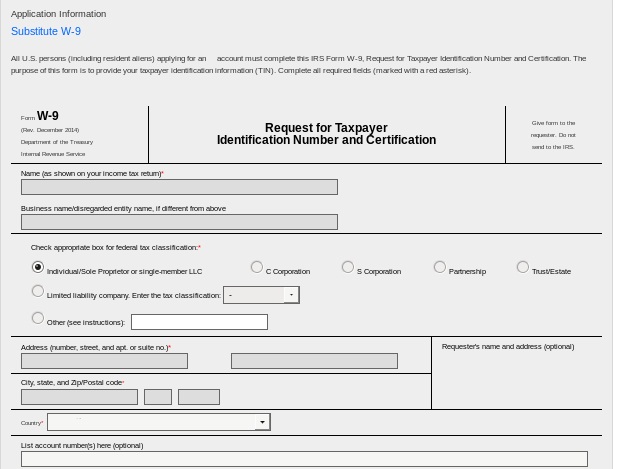

Screen 2 (W-9)

The second screen which the client will be presented will be the W-9 or W-8BEN tax form, whichever is applicable, based upon information provided on the prior screen. For example, a W-9 will be shown if the client selects U.S. tax residency (even if another tax residency was disclosed). Note that information on the W-9 will be pre-populated and cannot be edited.

Important: To change the pre-populated information on the W-9, the client MUST hit the back button and change the relevant information on the prior page for the tax form to be updated.

In the Part II Certification section of this screen, the client will need to review and check the boxes that apply.

Important: The first 3 boxes on the W-9 under certification must be checked to avoid having the client subject to back up withholding.

.jpg)

Next, the client will need to provide an electronic signature by typing their name (i.e., account title) exactly as it appears on the screen and select the “Save and Continue” button. The client will then be taken to the confirmation screen which will list any documents that they need to send to the broker.

.jpg)

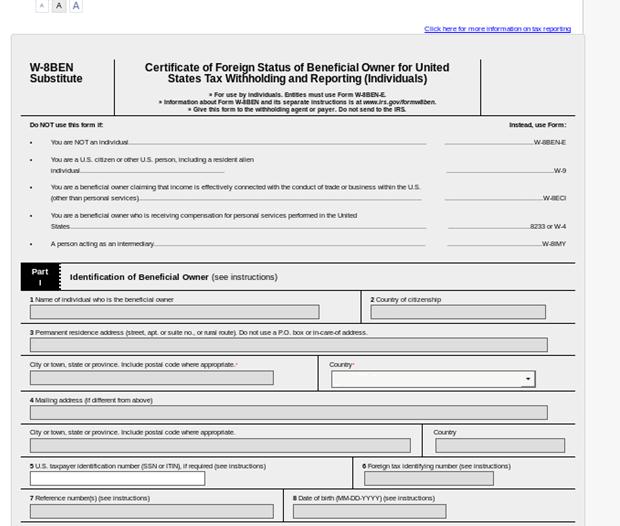

Screen 2 (W-8BEN)

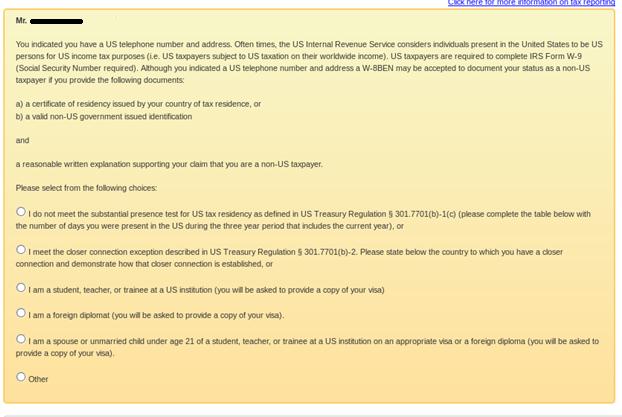

A W-8BEN will be show if the client selected any tax residency other than U.S. At the top of the tax form will be shown any U.S. or U.K. connections (e.g., U.S. address, telephone number, place of birth or crown dependency address) identified and tasks necessary to resolve it.

Example of U.S. address / telephone number problem

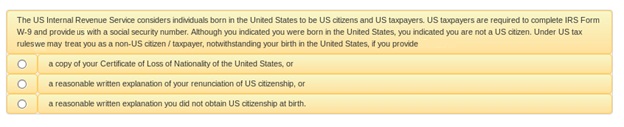

Example of U.S. place of birth.

The client must answer the questions by selecting the appropriate radio button. Many of these require document submissions to resolve the connection and the condition is not resolved until the appropriate documentation is provided. If a document is required, the client will be notified of this information once the form has been completed.

Information on Part I of the W-8BEN will be pre-populated based on the information provided on the prior page. Generally, the information cannot be edited with the exception of U.S. taxpayer identification number. This may be updated by the client.

On Part II of the W-8BEN the client will be prompted to specify whether they are a resident of a country which maintains a tax treaty with the U.S. Only those countries with which the U.S. maintains a treaty will be shown on the drop-down list and if the client does not see his or her treaty country, the client should select “N/A” or “I am not resident in a treaty country.”

Important: The system will flag a problem if the client’s mailing or permanent address is outside the treaty country which they have specified. In this case, the client will need to explain the reason for the non-treaty country address on the form and will be prompted afterwards to submit a proof of address and proof of identity from the treaty country for the claim to be valid. Client who cannot comply will not be afforded treaty benefits per IRS rules.

.jpg)

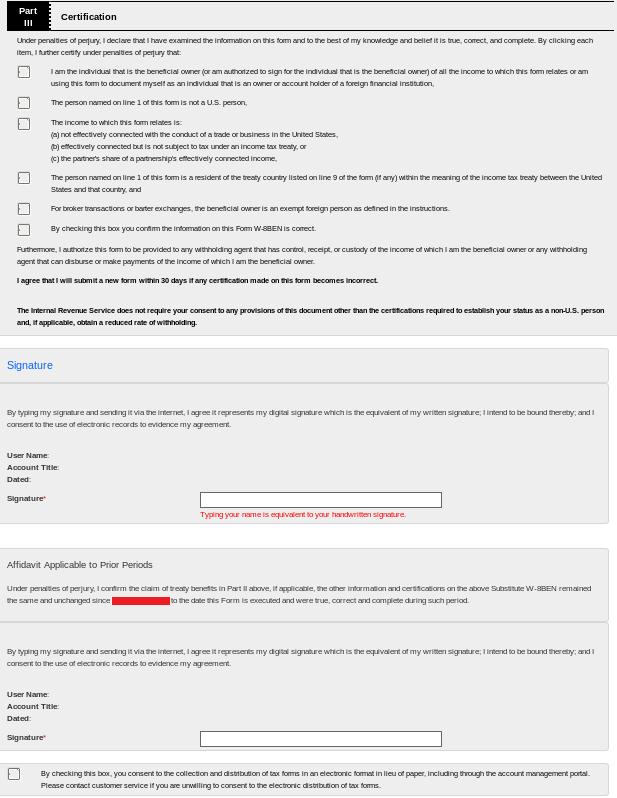

On Part III of the W-8BEN the client will be prompted to certify that the information provided on the form is accurate by checking the boxes and providing an electronic signature by typing their name (i.e., account title) exactly as it appears on the screen.

The client will also be prompted to acknowledge that the treaty benefits being claimed have remained unchanged since the date of their last tax form certification. This affidavit also requires entry of an electronic signature.

The client will then be prompted to check the box through which they consent to electronic collection and delivery of tax forms and then select the “Save and Continue” button. The client will then be taken to the confirmation screen which will list any documents that they need to send to the broker.

Final Review & Document Request

Once the form has been completed, it is subject to review by IB for purposes of verifying the client’s stated tax residency. This review may generate discrepancies in one of the following three areas: U.S. Connection, Treaty Claim or U.K. Crown Connection. If a client account is flagged for any discrepancy, you will need to contact them and request documents to resolve. The steps for resolving each of these is as follows:

1. U.S. Connection – Clients who complete the Form W-8BEN and have indication of a U.S. connection either from entries provided on the form or through a review by IB of the client’s records, will need submit proof that they are not a U.S. taxpayer. The proof varies by connection type and are as follows:

a. U.S. Person – if there is indication of U.S. citizenship or place of birth, the client must provide a copy of:

- Valid non-U.S. passport, AND

- Certificate of Loss of Nationality of the United States (Form DS-4083) or

- Reasonable written explanation of your renunciation of U.S. citizenship, or

- Reasonable written explanation that you did not obtain U.S. citizenship at birth.

b. U.S. Address – if there is an indication of a U.S. mailing address, permanent address or telephone number, the client must provide a copy of:

- Proof of non-U.S. identity document, AND

- Proof of non-U.S. address (less than 12 months old), AND

c. Explanation for U.S. address. One of:

- I do not meet the substantial presence test for U.S. residency as defined in U.S. Treasury Regulation § 301.7701(b)-1(c). In your response, please provide IB with the total number of days you are (intend to be) present in the United States in the current calendar year and the total number of days you were present in the United States in each of the 2 preceding calendar years. This computation is subject to verification by IB.

- I meet the closer connection exception described in U.S. Treasury Regulation § 301.7701(b)-2. In your response, please state the country to which you have a closer connection and demonstrate how that closer connection is established. This claim must be verified for reasonableness by IB.

- I am present in the United States as a student, teacher or trainee at a U.S. institution. Copy of F, J, M or Q visa from U.S. Immigration and Customs Enforcement is required.

- I am present in the United States as a foreign diplomat. Copy of your A or G visa (other than A-3 or G-3 visa) from U.S. Immigration and Customs Enforcement is required.

- I am present in the United States and am a spouse or unmarried child under the age of 21 of a person described in 2 prior bullets. Copy of visa required.

Important: If a U.S. Green Card is found, then W-8 tax status will only be allowed with IB’s consent.

If a U.S. passport is found, then W-8 status not allowed. The account will be considered a U.S. person and required to submit a W-9.

2. Treaty Claim - Clients who complete the Form W-8BEN containing a mailing address or permanent address outside of their stated country of tax residency will need submit proof of tax residency as follows:

a. Proof of treaty country identity document; AND

b. Proof of treaty country address (less than 12 months old): AND

c. Written explanation of non-treaty country address

3. U.K. Crown Connection - Clients who complete the Form W-8BEN containing a mailing address or permanent address located in either Guernsey, Jersey, Gibraltar or Isle of Man but did not indicate they are a tax resident of one of those regions will need to provide a reasonable written explanation for why they maintain such address.

Information and documentation to resolve problem must be sent to IB at fatca@interactivebrokers.com for confirmation.

IB will send a periodic report listing clients who have tasks which need to be completed so that you may contact them to act. This will include those accounts who have not logged into Account Management to complete the Tax Form or who have completed the form but need to send in documentation.

EXHIBIT 1 – Tax Form Prompt – U.S.

Immediate Response Requested

Dear Client,

A review of your account (Insert account ID) shows your tax information is out-of-date.Please immediately log into Account Management. You will be presented with information we already have on file as well as a tax form you should check, make corrections as needed, and then sign. This form will only be presented to the primary account owner, and should only take a few minutes to complete.

Confirming your information is essential to ensure that you will not become subject to backup withholding, including withholding on trade proceeds.

We appreciate your prompt attention to this matter.

Confirming your information is essential to ensure that you will not become subject to backup withholding, including withholding on trade proceeds.

We appreciate your prompt attention to this matter.

Immediate Response Requested

Dear Client,

A review of your account (Insert account ID) shows your tax information is out-of-date.

Please immediately log into Account Management. You will be presented with information we already have on file as well as a tax form you should check, make corrections as needed, and then sign. This form will only be presented to the primary account owner, and should only take a few minutes to complete.

Confirming your information is essential to ensure that (a) we can give you the most favorable rate on normal dividend and interest withholding as defined by standard international tax treaties; and (b) you will not become subject to any exceptional U.S. tax withholding.

We appreciate your prompt attention to this matter.

Confirming your information is essential to ensure that (a) we can give you the most favorable rate on normal dividend and interest withholding as defined by standard international tax treaties; and (b) you will not become subject to any exceptional U.S. tax withholding.

We appreciate your prompt attention to this matter.