期权第一至第四层级

什么是期权交易许可的层级?

IBKR新推出了两种更低层级的期权交易许可,即第一和第二层级交易许可,使目前无法获得“有限”或“完整”期权交易许可的客户可交易期权。“有限”交易许可目前被称为第三层级,而“完整”交易许可则被视为第四层级。

账户可交易的期权策略类型取决于账户获得的交易许可层级。不同的层级如下:

|

层级 |

支持的期权策略 |

|

第一层级 |

允许交易持保看涨期权,即在做空看涨期权的同时持有相等数量的底层证券。 |

|

第二层级 |

允许交易FINRA法规2360定义的持保期权持仓,但有额外的限制,即期权多头的到期日不得早于价差策略中期权空头的到期日。 |

|

第三层级 |

允许交易最大损失风险有限的期权策略。 |

|

第四层级 |

允许交易所有期权策略。 |

要了解各层级允许交易的期权组合举例,请见下表:

|

策略 |

层级要求 |

|

持保看涨/持保篮子看涨 |

第一层级 |

|

买股票卖买权(Buy Write) |

第一层级 |

|

做多期权持仓 |

第二层级 |

|

做多看涨 |

第二层级 |

|

做多看跌 |

第二层级 |

|

持保看跌 |

第二层级 |

|

保护性看涨 |

第二层级 |

|

保护性看跌 |

第二层级 |

|

做多跨式 |

第二层级 |

|

做多宽跨式套利 |

第二层级 |

|

转换 |

第二层级 |

|

做多看涨价差 |

第二层级 |

|

做多看跌价差 |

第二层级 |

|

做多铁鹰 |

第二层级 |

|

做多盒子价差 |

第二层级 |

|

领口 |

第二层级 |

|

做空领口 |

第二层级 |

|

做空看跌 |

第三层级 |

|

合成 |

第三层级 |

|

逆转 |

第三层级 |

|

做空看涨价差 |

第三层级 |

|

做空看跌价差 |

第三层级 |

|

做空铁鹰 |

第三层级 |

|

做多蝶式 |

第三层级 |

|

不平衡蝶式 |

第三层级 |

|

做空蝶式 |

第三层级 |

|

日历价差 - 借记 |

第三层级 |

|

对角价差 - 做空最先到期的边 |

第三层级 |

|

做空裸看涨 |

第四层级 |

|

做空跨式 |

第四层级 |

|

做空宽跨式 |

第四层级 |

|

做空合成 |

第四层级 |

|

日历价差 - 借记 |

第四层级 |

|

对角价差 - 做多最先到期的边 |

第四层级 |

交易期权须开立何种账户类型?

保证金、现金和IRA/退休账户可申请期权交易许可。

保证金账户可申请任意层级的期权交易许可(第一至第四层级均可)。现金或IRA账户只能申请第一至第三层级,且买入所有看涨和看跌期权均要求全额支付。

请注意

- 持有现金或保证金账户的客户必须在账户中保有2000美元(或等值的其它货币)的净清算价值方可开仓或加仓已有的未持保期权仓位。

如何申请或更新我的期权交易许可?

要更新您的期权交易许可:

1. 登录客户端

2. 依次选择使用者菜单(右上角的小人图标)和设置

3. 在 账户设置下找到交易板块

4. 点击交易许可

5. 找到期权板块,选择添加/编辑或请求,然后选择您想申请的许可层级并点击继续。

6. 阅读并签署披露与协议。

7. 点击继续并根据屏幕上的提示操作。

交易许可请求可能需要24-48小时审核。有关交易许可的更多信息,请见客户端用户指南。

请注意

- 当一个国家/地区只有期权交易许可,该许可将包括股票和指数期权。

- 受美国证监会限制,美国法定居民通常不得在美国以外交易证券期权。证券期权指以个股、美国法定股票或任何以现金结算的宽基指数期货为底层的期权。

- 某些期权合约额外要求有“复杂或加杠杆的交易所交易产品”许可。

21周岁以下的人士能否交易期权?

所有客户均可申请第一级的期权交易许可。然而,IBKR要求客户须年满21周岁方可申请第二至四级的许可。

申请期权交易许可须满足哪些要求?

IBKR会向满足最低年龄、流动净资产、投资目标、产品知识及投资经验要求的申请人提供不同层级的交易许可。此类信息是在开户时收集的,或在开户后客户申请提升交易许可时在客户端内收集。

如您需升级或查看您的财务信息、投资目标或投资经验,请根据以下说明操作:

1. 登录客户端

2. 前往使用者菜单(右上角的小人图标),然后点设置

3. 在账户设置下找到个人信息板块

4. 点击财务画像来修改您的信息并确认。

Option Levels 1-4

What are the levels of Option Trading Permissions?

IBKR introduced two new, lower levels of option trading permissions, Level 1 and 2, in order to be able to offer option trading to those who currently would not qualify for Limited or Full option trading permissions. Limited permissions are now referred to as Level 3, and Full permissions are considered Level 4.

Please note that clients of IB Canada and IB India are not eligible for option level permissions and remain with Limited or Full option trading permissions.

The type of option strategies available to trade will depend on the level of option permissions approved on the account. The various levels are as follows:

|

Level |

Option Strategies Allowed |

|

Level 1 |

Covered calls, i.e. short call vs long equal quantity of underlying, are allowed. |

|

Level 2 |

Covered Options Positions as defined by FINRA Rule 2360 are allowed with the additional restriction that the expiration date of the long option must be on or after the expiration date of the short option in a spread. |

|

Level 3 |

Option strategies that have limited maximum potential loss are allowed. |

|

Level 4 |

All option strategies are allowed. |

For examples of the types of option combinations allowed in each level, please see the following chart:

|

Strategy |

Level Requirement |

|

Covered Call/Covered Basket Call |

Level 1 |

|

Buy Write |

Level 1 |

|

Long option positions |

Level 2 |

|

Long Call |

Level 2 |

|

Long Put |

Level 2 |

|

Covered Put |

Level 2 |

|

Protective Call |

Level 2 |

|

Protective Put |

Level 2 |

|

Long Straddle |

Level 2 |

|

Long Strangle |

Level 2 |

|

Conversion |

Level 2 |

|

Long call spread |

Level 2 |

|

Long put spread |

Level 2 |

|

Long Iron Condor |

Level 2 |

|

Long Box Spread |

Level 2 |

|

Collar |

Level 2 |

|

Short Collar |

Level 2 |

|

Short Put |

Level 3 |

|

Synthetic |

Level 3 |

|

Reversal |

Level 3 |

|

Short Call Spread |

Level 3 |

|

Short Put Spread |

Level 3 |

|

Short Iron Condor |

Level 3 |

|

Long Butterfly |

Level 3 |

|

Unbalanced Butterfly |

Level 3 |

|

Short Butterfly |

Level 3 |

|

Calendar Spread - Debit |

Level 3 |

|

Diagnol Spread - Short leg expires first |

Level 3 |

|

Short Naked Call |

Level 4 |

|

Short Straddle |

Level 4 |

|

Short Strangle |

Level 4 |

|

Short Synthetic |

Level 4 |

|

Calendar Spread - Credit |

Level 4 |

|

Diagnol Spread - Long leg expires first |

Level 4 |

What account type is needed to trade options?

Option trading permissions are available for Margin, Cash and IRA/Retirement accounts.

A Margin account may request any level of option trading permissions (1-4). A Cash or IRA account may only request levels 1-3, and full payment is required for all call and put purchases.

Please Note

- Clients who maintain either a cash or margin type account must maintain net liquidating equity of at least USD 2,000 (or equivalent in other currencies) in order to establish or increase an existing uncovered options position.

How do I request or update my option trading permissions?

To update your trading permissions for options:

1. Log in to Client Portal

2. Select the User menu (head and shoulders icon in the top right corner) followed by Settings

3. Under Account Settings find the Trading section

4. Click on Trading Permissions

5. Locate Options section, select Add/Edit or Request under Options, select the level of permissions you want to request and click on CONTINUE.

6. Review and sign the disclosures and agreements.

7. Click CONTINUE and follow the prompts on screen.

Trading permission requests may take 24-48 hours to be reviewed. Find more information on trading permissions in the Client Portal Users' Guide.

Please Note

- When only Options permissions are available for a country the permissions will include both Stock and Index Options.

- US legal residents are generally excluded from trading securities options outside of the United States due to SEC restrictions. Securities options are defined as any option on an individual stock, US legal stock, or any cash settled broad based index future.

- Certain option contracts require an additional permission for "Complex or Leveraged Exchange Traded Products".

Is it possible for someone under the age of 21 to trade options?

All clients are eligible for Level 1 options trading permissions. However, IBKR requires that clients be at least 21 years of age to be eligible for level 2-4 option trading.

What are the requirements to qualify for option trading permissions?

IBKR offers various levels of trading permissions to applicants meeting minimum age, liquid net worth, investment objectives, product knowledge and prior experience qualifications. This information is gathered in the account application phase or in Client Portal if a trading permissions upgrade is requested following initial account approval.

If you need to update or review your financial information, investment objectives or experience use the button above or follow this procedure:

1. Log into Client Portal

2. Go to the User menu (head and shoulders icon in the top right corner) followed by Settings

3. Under Account Settings find the Account Profile section

4. Click on Financial Profile, rectify your information and confirm.

VR(T) time decay and term adjusted Vega columns in Risk Navigator (SM)

Background

Risk Navigator (SM) has two Adjusted Vega columns that you can add to your report pages via menu Metrics → Position Risk...: "Adjusted Vega" and "Vega x T-1/2". A common question is what is our in-house time function that is used in the Adjusted Vega column and what is the aim of these columns. VR(T) is also generally used in our Stress Test or in the Risk Navigator custom scenario calculation of volatility index options (i.e VIX).

Abstract

Implied volatilities of two different options on the same underlying can change independently of each other. Most of the time the changes will have the same sign but not necessarily the same magnitude. In order to realistically aggregate volatility risk across multiple options into a single number, we need an assumption about relationship between implied volatility changes. In Risk Navigator, we always assume that within a single maturity, all implied volatility changes have the same sign and magnitude (i.e. a parallel shift of volatility curve). Across expiration dates, however, it is empirically known that short term volatility exhibits a higher variability than long term volatility, so the parallel shift is a poor assumption. This document outlines our approach based on volatility returns function (VR(T)). We also describe an alternative method developed to accommodate different requests.

VR(T) time decay

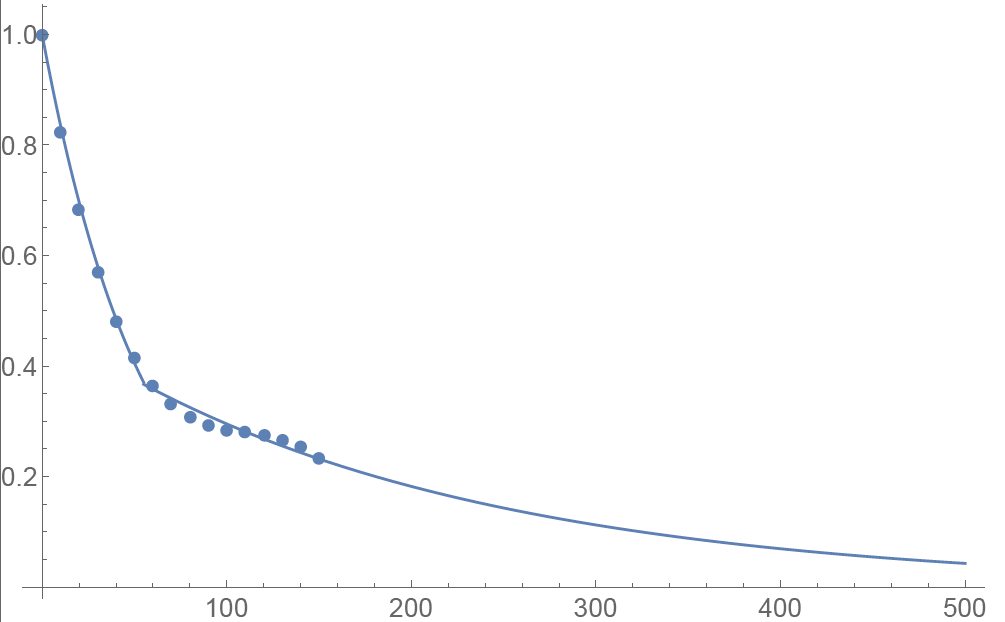

We applied the principal component analysis to study daily percentage changes of volatility as a function of time to maturity. In that study we found that the primary eigen-mode explains approximately 90% of the variance of the system (with second and third components explaining most of the remaining variance being the slope change and twist). The largest amplitude of change for the primary eigenvector occurs at very short maturities, and the amplitude monotonically decreases as time to expiration increase. The following graph shows the main eigenvector as a function of time (measured in calendar days). To smooth the numerically obtained curve, we parameterize it as a piecewise exponential function.

Functional Form: Amplitude vs. Calendar Days

To prevent the parametric function from becoming vanishingly small at long maturities, we apply a floor to the longer term exponential so the final implementation of this function is:

where bS=0.0180611, a=0.365678, bL=0.00482976, and T*=55.7 are obtained by fitting the main eigenvector to the parametric formula.

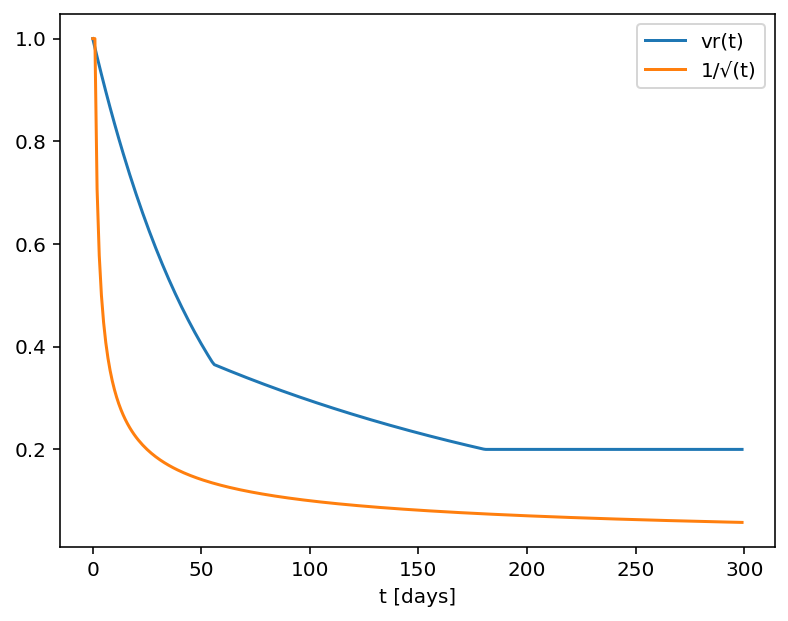

Inverse square root time decay

Another common approach to standardize volatility moves across maturities uses the factor 1/√T. As shown in the graph below, our house VR(T) function has a bigger volatility changes than this simplified model.

Time function comparison: Amplitude vs. Calendar Days

Adjusted Vega columns

Risk Navigator (SM) reports a computed Vega for each position; by convention, this is the p/l change per 1% increase in the volatility used for pricing. Aggregating these Vega values thus provides the portfolio p/l change for a 1% across-the-board increase in all volatilities – a parallel shift of volatility.

However, as described above a change in market volatilities might not take the form of a parallel shift. Empirically, we observe that the implied volatility of short-dated options tends to fluctuate more than that of longer-dated options. This differing sensitivity is similar to the "beta" parameter of the Capital Asset Pricing Model. We refer to this effect as term structure of volatility response.

By multiplying the Vega of an option position with an expiry-dependent quantity, we can compute a term-adjusted Vega intended to allow more accurate comparison of volatility exposures across expiries. Naturally the hoped-for increase in accuracy can only come about if the adjustment we choose turns out to accurately model the change in market implied volatility.

We offer two parametrized functions of expiry which can be used to compute this Vega adjustment to better represent the volatility sensitivity characteristics of the options as a function of time to maturity. Note that these are also referred as 'time weighted' or 'normalized' Vega.

Adjusted Vega

A column titled "Vega Adjusted" multiplies the Vega by our in-house VR(T) term structure function. This is available any option that is not a derivative of a Volatility Product ETP. Examples are SPX, IBM, VIX but not VXX.

Vega x T-1/2

A column for the same set of products as above titled "Vega x T-1/2" multiplies the Vega by the inverse square root of T (i.e. 1/√T) where T is the number of calendar days to expiry.

Aggregations

Cross over underlying aggregations are calculated in the usual fashion given the new values. Based on the selected Vega aggregation method we support None, Straight Add (SA) and Same Percentage Move (SPM). In SPM mode we summarize individual Vega values multiplied by implied volatility. All aggregation methods convert the values into the base currency of the portfolio.

Custom scenario calculation of volatility index options

Implied Volatility Indices are indexes that are computed real-time basis throughout each trading day just as a regular equity index, but they are measuring volatility and not price. Among the most important ones is CBOE's Marker Volatility Index (VIX). It measures the market's expectation of 30-day volatility implied by S&P 500 Index (SPX) option prices. The calculation estimates expected volatility by averaging the weighted prices of SPX puts and calls over a wide range of strike prices.

The pricing for volatility index options have some differences from the pricing for equity and stock index options. The underlying for such options is the expected, or forward, value of the index at expiration, rather than the current, or "spot" index value. Volatility index option prices should reflect the forward value of the volatility index (which is typically not as volatile as the spot index). Forward prices of option volatility exhibit a "term structure", meaning that the prices of options expiring on different dates may imply different, albeit related, volatility estimates.

For volatility index options like VIX the custom scenario editor of Risk Navigator offers custom adjustment of the VIX spot price and it estimates the scenario forward prices based on the current forward and VR(T) adjusted shock of the scenario adjusted index on the following way.

- Let S0 be the current spot index price, and

- S1 be the adjusted scenario index price.

- If F0 is the current real time forward price for the given option expiry, then

- F1 scenario forward price is F1 = F0 + (S1 - S0) x VR(T), where T is the number of calendar days to expiry.

在哪里可以了解更多有关期权的信息?

期权清算公司(OCC)是所有美国交易所交易之证券期权的中央清算机构,其运营着一个呼叫中心以满足个人投资者和零售证券经纪商的学习需求。其主要解决由OCC清算之期权产品的下列相关问题:

- 期权行业协会有关研讨会、视频和教学材料的信息;

- 基本期权问题,如期限定义和产品信息;

- 策略和操作性问题(包括特定交易头寸和策略)解答。

可拨打1-800-OPTIONS联系呼叫中心。营业时间为美国中部标准时间周一至周四上午8点到下午5点,周五上午8点到下午4点.每月逢周五到期日营业时间将延长至下午5点。

Complex Position Size

For complex, multi-leg options positions comprising two or more legs, TWS might not track all changes to this position, e.g. a vertical spread where the short leg is assigned and the user re-writes the same leg the next day, or if the user creates a the position over multiple trades, or if the order is not filled as a native combination at the exchange.

If you received a message because you are submitting an order to close a position, roll a position, or modify a position using the “% Change” feature, it means that the maximum quantity of option positions in your account that are available to close for this order is different from that of the original position tracked by TWS.

Before submitting, you should review the order and confirm that the order quantity we have calculated is the correct quantity that you want to trade.

盈收

北美上市公司通常要求按季度发布盈收报告。这些报告包含一系列相关数据(收益和利润),通常可反映公司未来的盈收能力,可能引起公司股票市价的巨大波动。从期权交易的视角看,任何可能导致股票波动的因素都会影响期权定价。盈收发布也不例外。

期权交易者常常试图预期市场对盈收新闻的反应。他们知道随着盈收发布日期的临近,隐含波动率-期权价格的关键因素将稳步上升,而斜线-平价期权与价外期权隐含波动率的差额也会逐渐变陡。调整幅度通常基于历史情况而定。过去在盈收发布后出现重大波动的股票通常期权价格会更高。

盈收风险具有特殊性,这意味着其通常因股票而异且不易于与指数或同类公司对冲。相互密切关联的股票其反应可能会大相径庭,这会导致股价偏移或指数衰减。出于这些原因,没有哪个策略适用于在这些情境下交易期权。交易员必须对股票的可能动向有十分清晰的预期,然后决定哪种期权组合可能会产生最大的利润。

如果市场对一个公司的盈收预期太过乐观,很简单,只需购买(尽管通常比较贵)跨式期权或价外看跌期权并期待市场发生重大变动。在即月隐含波动率看似过高时利用反向预期也可能盈利,但这也可能在股票大幅上扬时成为空头裸期权,从而导致严重的损失。交易员可通过购买日历价差-卖出即月看跌期权并买入下月行使价相同的期权来利用较高的即月波动率。如果股票以行使价成交且即月期权的下滑速度远大于价格更高的远期期权,则会实现最大盈利。损失限制为初始交易价。

有时,当价外看跌期权隐含波动率日渐高于平价期权时,斜线会变得十分陡峭,这表明市场过度恐慌。使用垂直价差的交易员可在这种情景下盈利。看跌交易员可以买入平价看跌期权同时卖出价外看跌期权。这允许买家支付部分高价期权的成本,尽管如果股价跌至较低行使价以下,这会限制交易利润。另一方面,认为市场过度看跌的交易员可以卖出价外看跌期权同时买入行使价更低的看跌期权。尽管交易员买入的是波动率较高的期权,只要股价高于行使价就能盈利,同时损失也限定在两个行使价之间的差额。T

该文章仅作信息参考并不旨在提供建议或招揽买卖证券。期权交易涉及重大风险。交易期权前请阅读"标准期权的特征和风险"。客户对自己的交易决定负全部责任。

到期前行使看涨期权的注意事项

简介

到期前行使股票看涨期权通常不会带来收益,因为:

- 这会导致剩余期权时间价值的丢失;

- 需要更大的资金投入以支付股票交割;并且

- 会给期权持有人带来更大的损失风险。

尽管如此,对于有能力满足更大资金或借款要求并能承受更大下行市场风险的账户持有人来说,提前行权行使美式看涨期权可获取即将分配的股息。

背景

看涨期权持有者无权获取底层股票的股息,因为该股息属于股息登记日前的股票持有人所有。 其他条件相同,股价应该下降,降幅与除息日的股息保持一致。期权定价理论提出看涨期权价格將反映预期股息的折扣价格,看涨期权价格也可能在除息日下跌。最可能促成该情境与提前行权决定的条件如下:

1. 期权为深度价内期权且delta值为100;

2. 期权几乎没有时间价值;

3. 股息相对较高且除息日在期权到期日之前。

举例

为阐述这些条件对提前行权决定的影响,假设账户的多头现金余额为$9,000美元,且持有行使价为$90.00美元的ABC多头看涨头寸,10天后到期。 ABC当前的成交价为$100.00美元,每股股息为$2.00美元,明天是除息日。再假设期权价格与股票价格动向相同,且在除息日下跌的幅度均为股息金额。

这里,我们将检查行权决定,目的是维持100股delta头寸并使用两种期权价格假设(假设一个为平价,一个高于平价)最大化总资产。

情境1:期权价格为平价 - $10.00美元

如果期权以平价交易,提前行权可维持delta头寸并可避免股票除息交易时多头期权价值遭受损失,从而保护资产。在这里现金收入被全数用于以行使价购买股票,期权权利金就此丧失并且股票(扣除股息)与应收股息会记入账户。如果您想通过在除息日前卖出期权并买入股票来达到同样的效果,请记得考虑佣金/价差:

| 情境1 | ||||

| 账户组成部分 | 起始余额 | 提前行权 | 无行动 |

卖期权& 买股票 |

| 现金 | $9,000 | $0 | $9,000 | $0 |

| 期权 | $1,000 | $0 | $800 | $0 |

| 股票 | $0 | $9,800 | $0 | $9,800 |

| 应收股息 | $0 | $200 | $0 | $200 |

| 总资产 | $10,000 | $10,000 | $9,800 | $10,000减去佣金/价差 |

情境2:期权价格高于平价 - $11.00美元

如果期权以高于平价的价格交易,提前行权获取股息则可能并不会带来收益。在此情景中,提前行权可能会导致期权时间价值损失$100美元,而卖出期权买入股票在扣除佣金之后收益情况也可能不如不采取行动。在这里,可取的行动为无行动。

| 情境2 | ||||

| 账户组成部分 | 起始余额 | 提前行权 | 无行动 |

卖期权& 买股票 |

| 现金 | $9,000 | $0 | $9,000 | $100 |

| 期权 | $1,100 | $0 | $1,100 | $0 |

| 股票 | $0 | $9,800 | $0 | $9,800 |

| 应收股息 | $0 | $200 | $0 | $200 |

| 总资产 | $10,100 | $10,000 | $10,100 | $10,100减去佣金/价差 |

![]() 请注意:考虑到空头期权边被行权的可能性,持有作为价差组成部分之多头看涨头寸的账户持有人应格外注意不行使多头期权边的风险。请注意,空头看涨期权的被行权会导致空头股票头寸,且在股息登记日前持有空头股票头寸的持有人有义务向股票的借出者支付股息。此外,清算所行权通知处理周期不支持提交响应被行权的行权通知。

请注意:考虑到空头期权边被行权的可能性,持有作为价差组成部分之多头看涨头寸的账户持有人应格外注意不行使多头期权边的风险。请注意,空头看涨期权的被行权会导致空头股票头寸,且在股息登记日前持有空头股票头寸的持有人有义务向股票的借出者支付股息。此外,清算所行权通知处理周期不支持提交响应被行权的行权通知。

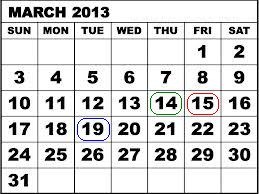

例如,假设SPDR S&P 500 ETF Trust (SPY)的信用看涨(熊市)价差包括100张13年3月到期行使价为$146美元的空头合约,以及100张13年3月到期行使价为$147美元的多头合约。在13年3月14日,SPY Trust宣布每股股息为$0.69372美元,并且会在13年4月30日向13年3月19日前登记的股东支付。因为美国股票的结算周期为3个工作日,想要获取股息,交易者需要在13年1月14日之前买入股票或行使看涨期权,因为该日期一过,股票便开始除息交易。

13年3月14日,距离期权到期只剩一个交易日,平价成交的两张期权合约每张合约的最大风险为$100美元,100张合约则为$10,000美元。但是,未能行使多头合约以获取股息以及未能避免空头合约被其他想要获取股息的交易者行权会使每张合约产生额外$67.372美元的风险,如果所有空头看涨合约都被行权,则所有头寸总风险为$6,737.20美元。如下表所示,如果空头期权边没有被行权,则13年3月15日确定最终的合约结算价格时,最大风险仍为每张合约$100美元。

| 日期 | SPY收盘价 | 13年3月行使价为$146的看涨期权 | 13年3月行使价为$147的看涨期权 |

| 2013年3月14日 | $156.73 | $10.73 | $9.83 |

| 2013年3月15日 | $155.83 | $9.73 | $8.83 |

请注意,如果您的账户符合美国871(m)预扣税要求,则除息日前平仓头多期权头寸并在除息日后重新建仓可能会带来收益。

有关如何提交提前行权通知的信息,请查看网站。

上述内容仅作信息参考,不构成任何推荐、交易建议,也不代表提前行权会成功或适合所有客户或交易。账户持有人应咨询税务专家以确定提前行权可能带来的税务影响,并应格外注意以多头股票头寸替换多头期权头寸的潜在风险。

Earnings

Publicly traded companies in North America generally are required to release earnings on a quarterly basis. These announcements, which contain a host of relevant statistics, including revenue and margin data, and often projections about the company's future profitability, have the potential to cause a significant move in the market price of the company's shares. From an options trading viewpoint, anything with the potential to cause volatility in a stock affects the pricing of its options. Earnings releases are no exceptions.

Options traders often try to anticipate the market's reaction to earnings news. They know implied volatilities, the key to options prices, will steadily rise while skew - the difference in implied volatility between at-money and out-of-the-money options - will steadily steepen as the earnings date approaches. The degree by which those adjustments occur is often based on history. Stocks that have historically made significant post-earnings moves often have more expensive options.

Earnings risk is idiosyncratic, meaning that it is usually stock specific and not easily hedged against an index or a similar company. Stocks that are normally quite well correlated may react quite differently, leading to share prices that diverge or indices with dampened moves. For those reasons, there is no single strategy that works for trading options in these situations. Traders must have very clear expectations for a stock's potential move, and then decide which combination of options will likely lead to the most profitable results if the trader is correct.

If the market seems too sanguine about a company's earnings prospects, it is fairly simple (though often costly) to buy a straddle or an out-of the-money put and hope for a big move. Taking advantage of the opposite prospect, when front month implied volatilities seem too high, can also be profitable but it can also cause serious losses to be short naked options in the face of a big upward stock move. Traders can take advantage of high front month volatility by buying a calendar spread - selling a front month put and buying the same strike in the following month. The maximum profit potential is reached if the stock trades at the strike price, with the front-month option decaying far faster than the more expensive longer-term option. Losses are limited to the initial trade price.

Sometimes excessive fear is expressed by extremely steep skew, when out-of-the-money puts display increasingly higher implied volatilities than at-money options. Traders who use vertical spreads can capitalize on this phenomenon. Those who are bearish can buy an at-money put while selling an out-of-the-money put. This allows the purchaser to defray some of the cost of a high priced option, though it caps the trade's profits if the stock declines below the lower strike. On the other hand, those who believe the market is excessively bearish can sell an out-of-the-money put while buying an even lower strike put. Although the trader is buying the higher volatility option, it allows him to make money as long as the stock stays above the higher strike price, while capping his loss at the difference between the two strikes.

This article is provided for information only and is not intended as a recommendation or a solicitation to buy or sell securities. Option trading can involve significant risk. Before trading options read the "Characteristics and Risks of Standardized Options." Customers are solely responsible for their own trading decisions.

Considerations for Exercising Call Options Prior to Expiration

INTRODUCTION

Exercising an equity call option prior to expiration ordinarily provides no economic benefit as:

- It results in a forfeiture of any remaining option time value;

- Requires a greater commitment of capital for the payment or financing of the stock delivery; and

- May expose the option holder to greater risk of loss on the stock relative to the option premium.

Nonetheless, for account holders who have the capacity to meet an increased capital or borrowing requirement and potentially greater downside market risk, it can be economically beneficial to request early exercise of an American Style call option in order to capture an upcoming dividend.

BACKGROUND

As background, the owner of a call option is not entitled to receive a dividend on the underlying stock as this dividend only accrues to the holders of stock as of its dividend Record Date. All other things being equal, the price of the stock should decline by an amount equal to the dividend on the Ex-Dividend date. While option pricing theory suggests that the call price will reflect the discounted value of expected dividends paid throughout its duration, it may decline as well on the Ex-Dividend date. The conditions which make this scenario most likely and the early exercise decision favorable are as follows:

1. The option is deep-in-the-money and has a delta of 100;

2. The option has little or no time value;

3. The dividend is relatively high and its Ex-Date precedes the option expiration date.

EXAMPLES

To illustrate the impact of these conditions upon the early exercise decision, consider an account maintaining a long cash balance of $9,000 and a long call position in hypothetical stock “ABC” having a strike price of $90.00 and time to expiration of 10 days. ABC, currently trading at $100.00, has declared a dividend of $2.00 per share with tomorrow being the Ex-Dividend date. Also assume that the option price and stock price behave similarly and decline by the dividend amount on the Ex-Date.

Here, we will review the exercise decision with the intent of maintaining the 100 share delta position and maximizing total equity using two option price assumptions, one in which the option is selling at parity and another above parity.

SCENARIO 1: Option Price At Parity - $10.00

In the case of an option trading at parity, early exercise will serve to maintain the position delta and avoid the loss of value in long option when the stock trades ex-dividend, to preserve equity. Here the cash proceeds are applied in their entirety to buy the stock at the strike, the option premium is forfeited and the stock (net of dividend) and dividend receivable are credited to the account. If you aim for the same end result by selling the option prior to the Ex-Dividend date and purchasing the stock, remember to factor in commissions/spreads:

| SCENARIO 1 | ||||

|

Account Components |

Beginning Balance |

Early Exercise |

No Action |

Sell Option & Buy Stock |

| Cash | $9,000 | $0 | $9,000 | $0 |

| Option | $1,000 | $0 | $800 | $0 |

| Stock | $0 | $9,800 | $0 | $9,800 |

| Dividend Receivable | $0 | $200 | $0 | $200 |

| Total Equity | $10,000 | $10,000 | $9,800 | $10,000 less commissions/spreads |

SCENARIO 2: Option Price Above Parity - $11.00

In the case of an option trading above parity, early exercise to capture the dividend may not be economically beneficial. In this scenario, early exercise would result in a loss of $100 in option time value, while selling the option and buying the stock, after commissions, may be less beneficial than taking no action. In this scenario, the preferable action would be No Action.

| SCENARIO 2 | ||||

|

Account Components |

Beginning Balance |

Early Exercise |

No Action |

Sell Option & Buy Stock |

| Cash | $9,000 | $0 | $9,000 | $100 |

| Option | $1,100 | $0 | $1,100 | $0 |

| Stock | $0 | $9,800 | $0 | $9,800 |

| Dividend Receivable | $0 | $200 | $0 | $200 |

| Total Equity | $10,100 | $10,000 | $10,100 | $10,100 less commissions/spreads |

![]() NOTE:

NOTE:

Options have two components that make up their total premium value - intrinsic value and time value. The intrinsic value is the amount by which the option is in-the-money, while the time value represents the possibility that the option could become even more profitable before expiration as the underlying asset price fluctuates while providing protection against adverse moves.

Many options are American-style, which means they can be exercised early, ahead of their expiration date. Early exercise of an option eliminates the remaining time value component from the option's premium, since the option holder loses protection against unfavorable movements in the underlying asset’s price.

This makes early exercise suboptimal in most situations, as the option holder is willingly forfeiting a portion of the option's value.

There are a few specific circumstances where early exercise could make sense, such as:

- For call options on a stock that will pay dividends soon, where the dividend amount exceeds the remaining time value (and only if the exercise will settle on or prior to the record date for the dividend).

- For deep in-the-money options where the time value is negligible compared to the intrinsic value, and the option is expected to drop in value due to interest rate effects (PUTS), or expected stock loan benefits (CALLS).

The first case, exercising an in the money call immediately ahead of a dividend payment, is the most common economically-sensible early exercise. In most cases, it is advisable to hold or sell the option instead of exercising it early, in order to capture the remaining time value. An option should only be exercised early after carefully considering all factors and determining that the benefits of early exercise outweigh the time value being surrendered.

Account holders holding a long call position as part of a spread should pay particular attention to the risks of not exercising the long leg given the likelihood of being assigned on the short leg. Note that the assignment of a short call results in a short stock position and holders of short stock positions as of a dividend Record Date are obligated to pay the dividend to the lender of the shares. In addition, the clearinghouse processing cycle for exercise notices does not accommodate submission of exercise notices in response to assignment.

As example, consider a credit call (bear) spread on the SPDR S&P 500 ETF Trust (SPY) consisting of 100 short contracts in the March '13 $146 strike and 100 long contracts in the March '13 $147 strike. On 3/14/13, with the SPY Trust declared a dividend of $0.69372 per share, payable 4/30/13 to shareholders of record as of 3/19/13. Given the 3 business day settlement time frame for U.S. stocks, one would have had to buy the stock or exercise the call no later than 3/14/13 in order receive the dividend, as the next day the stock began trading Ex-Dividend.

On 3/14/13, with one trading day left prior to expiration, the two option contracts traded at parity, suggesting maximum risk of $100 per contract or $10,000 on the 100 contract position. However, the failure to exercise the long contract in order to capture the dividend and protect against the likely assignment on the short contracts by others seeking the dividend created an additional risk of $67.372 per contract or $6,737.20 on the position representing the dividend obligation were all short calls assigned. As reflected on the table below, had the short option leg not been assigned, the maximum risk when the final contract settlement prices were determined on 3/15/13 would have remained at $100 per contract.

| Date | SPY Close | March '13 $146 Call | March '13 $147 Call |

| March 14, 2013 | $156.73 | $10.73 | $9.83 |

| March 15, 2013 | $155.83 | $9.73 | $8.83 |

Please note that if your account is subject to tax withholding requirements of the US Treasure rule 871(m), it may be beneficial to close a long option position before the ex-dividend date and re-open the position after ex-dividend.

For information regarding how to submit an early exercise notice please click here.

The above article is provided for information purposes only as is not intended as a recommendation, trading advice nor does it constitute a conclusion that early exercise will be successful or appropriate for all customers or trades. Account holders should consult with a tax specialist to determine what, if any, tax consequences may result from early exercise and should pay particular attention to the potential risks of substituting a long option position with a long stock position.