Come stabilire se si stanno assumendo in prestito fondi da IBKR

Se il saldo di liquidità complessivo di un determinato conto è a debito, o negativo, allora, i fondi sono stati assunti in prestito e questo è soggetto all'addebito di interessi. Tuttavia, potrebbe essere ancora presente un prestito, anche qualora il saldo di liquidità complessivo sia a credito, o positivo, come conseguenza della compensazione del saldo o di eventuali scarti temporali. Gli esempi più comuni in questa casistica sono i seguenti:

1. Saldi valutari a credito e a debito: i titolari di conto possono assumere in prestito liquidità denominata in una valuta se tale liquidità può essere garantita da un saldo a credito in un'altra valuta. Si consideri, per esempio, un conto, in cui la valuta di base è lo USD con un saldo di liquidità a credito regolato in USD di 10,000, un saldo di liquidità a debito regolato in EUR di 5,000 e un tasso di cambio EUR.USD di 1.38:1. In questo caso, ai fini della rendicontazione e del calcolo degli interessi, il saldo di liquidità complessivo è un credito in USD di 3,088 (10,000 - (5,000 * 1.38)). Dato che ciascuna valuta è soggetta a una specifica modalità di finanziamento e reinvestimento, il saldo a debito sarebbe soggetto a costi di finanziamento in funzione del relativo tasso di riferimento e del relativo livello. Tale costo potrebbe essere compensato dagli eventuali interessi percepiti sul saldo a credito secondo il relativo tasso di riferimento e il relativo livello.

2. Saldi al lordo per segmento: – il conto Universal Account di IBKR contiene molteplici conti di secondo livello o segmenti, ciascuno dei quali mantiene posizioni e garanzie non possono essere combinati per motivi di regolamentazione e salvaguardia dei clienti. Questa separazione non consente la compensazione dei saldi tra i vari segmenti, quindi, il credito di un determinato segmento potrebbe non compensare il debito di un altro. Si consideri, per esempio, un conto IBLLC avente posizioni su titoli e commodity, dove il segmento titoli mantiene un saldo di liquidità a debito di 3,000 USD e il segmento commodity un saldo di liquidità a credito di 8,000 USD. Nonostante il conto detenga un saldo a credito netto complessivo di 5,000 USD, il saldo a debito potrebbe andare in contro a interessi passivi, potenzialmente compensabili dagli interessi attivi del saldo a credito.

3. Vendita allo scoperto: – la vendita allo scoperto è un'operazione a margine nella quale il titolare del conto assume in prestito azioni anziché liquidità. Mentre i proventi derivanti dalla vendita allo scoperto sono accreditati sul saldo di liquidità del conto, questi fondi devono essere depositati presso il prestatore delle azioni a garanzia del loro rendimento. Di conseguenza, e in considerazione del fatto che l'operazione di prestito è soggetta alle proprie specifiche condizioni di finanziamento, non viene tenuto conto della liquidità a garanzia del prestito nel determinare l'eventuale presenza di un prestito a margine.

Per esempio, si consideri un conto che ha registrato un capitale di liquidazione netto (tutti i saldi in USD) di 9,000 costituito da un saldo di liquidità a credito di 4,000, un valore azionario long pari a 10,000 e un valore azionario short di 5,000. Per stabilire se i fondi sono assunti in prestito per il finanziamento della posizione azionaria long, la porzione di 5,000 della liquidità data in garanzia al prestatore delle azioni è dedotta dal saldo di liquidità complessivo di 4,000, con un conseguente debito di 1,000. Questo debito è soggetto a interessi passivi e la liquidità sottostante il prestito azionario è soggetta o all'addebito di interessi in caso di azioni hard-to-borrow o a uno rimborso sulle azioni short se le quote azionarie sono facilmente ottenibili per il prestito e i tassi di reinvestimento sufficientemente alti.

4. Fondi non regolati: - le assunzioni di prestiti sono stabilite in base ai fondi regolati e l'arco temporale entro il quale è previsto il pagamento di una determinata transazione dipende dallo specifico prodotto (es. sono previsti, in genere, 3 giorni lavorativi per il regolamento dei titoli azionari, 2 per le valute a pronti e 1 per i derivati). Ai fini della rendicontazione e della piattaforma di trading, i saldi di liquidità sono dichiarati alla data della transazione anziché alla data del regolamento, come se il regolamento fosse avvenuto.

Di conseguenza, un conto che riporta un saldo di liquidità a credito potrebbe, in realtà, essere ancora soggetto a un prestito a margine se tale saldo comprende proventi della vendita di azioni acquistate con fondi assunti in prestito in attesa di regolamento. Allo stesso modo, un conto potrebbe registrare un saldo a debito basato sulla data della transazione, senza però essere ancora soggetto a un prestito a margine e interessi passivi, in quanto la transazione non è ancora stata regolata.

Per maggiori informazioni in merito al calcolo degli interessi, si prega di fare riferimento all'articolo Modalità di calcolo degli interessi.

Allocation of Partial Fills

How are executions allocated when an order receives a partial fill because an insufficient quantity is available to complete the allocation of shares/contracts to sub-accounts?

Overview:

From time-to-time, one may experience an allocation order which is partially executed and is canceled prior to being completed (i.e. market closes, contract expires, halts due to news, prices move in an unfavorable direction, etc.). In such cases, IB determines which customers (who were originally included in the order group and/or profile) will receive the executed shares/contracts. The methodology used by IB to impartially determine who receives the shares/contacts in the event of a partial fill is described in this article.

Background:

Before placing an order CTAs and FAs are given the ability to predetermine the method by which an execution is to be allocated amongst client accounts. They can do so by first creating a group (i.e. ratio/percentage) or profile (i.e. specific amount) wherein a distinct number of shares/contracts are specified per client account (i.e. pre-trade allocation). These amounts can be prearranged based on certain account values including the clients’ Net Liquidation Total, Available Equity, etc., or indicated prior to the order execution using Ratios, Percentages, etc. Each group and/or profile is generally created with the assumption that the order will be executed in full. However, as we will see, this is not always the case. Therefore, we are providing examples that describe and demonstrate the process used to allocate partial executions with pre-defined groups and/or profiles and how the allocations are determined.

Here is the list of allocation methods with brief descriptions about how they work.

· AvailableEquity

Use sub account’ available equality value as ratio.

· NetLiq

Use subaccount’ net liquidation value as ratio

· EqualQuantity

Same ratio for each account

· PctChange1:Portion of the allocation logic is in Trader Workstation (the initial calculation of the desired quantities per account).

· Profile

The ratio is prescribed by the user

· Inline Profile

The ratio is prescribed by the user.

· Model1:

Roughly speaking, we use each account NLV in the model as the desired ratio. It is possible to dynamically add (invest) or remove (divest) accounts to/from a model, which can change allocation of the existing orders.

Basic Examples:

Details:

CTA/FA has 3-clients with a predefined profile titled “XYZ commodities” for orders of 50 contracts which (upon execution) are allocated as follows:

Account (A) = 25 contracts

Account (B) = 15 contracts

Account (C) = 10 contracts

Example #1:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 10 am (ET) the order begins to execute2but in very small portions and over a very long period of time. At 2 pm (ET) the order is canceled prior to being executed in full. As a result, only a portion of the order is filled (i.e., 7 of the 50 contracts are filled or 14%). For each account the system initially allocates by rounding fractional amounts down to whole numbers:

Account (A) = 14% of 25 = 3.5 rounded down to 3

Account (B) = 14% of 15 = 2.1 rounded down to 2

Account (C) = 14% of 10 = 1.4 rounded down to 1

To Summarize:

A: initially receives 3 contracts, which is 3/25 of desired (fill ratio = 0.12)

B: initially receives 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: initially receives 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The system then allocates the next (and final) contract to an account with the smallest ratio (i.e. Account C which currently has a ratio of 0.10).

A: final allocation of 3 contracts, which is 3/25 of desired (fill ratio = 0.12)

B: final allocation of 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: final allocation of 2 contract, which is 2/10 of desired (fill ratio = 0.20)

The execution(s) received have now been allocated in full.

Example #2:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 11 am (ET) the order begins to be filled3 but in very small portions and over a very long period of time. At 1 pm (ET) the order is canceled prior being executed in full. As a result, only a portion of the order is executed (i.e., 5 of the 50 contracts are filled or 10%).For each account, the system initially allocates by rounding fractional amounts down to whole numbers:

Account (A) = 10% of 25 = 2.5 rounded down to 2

Account (B) = 10% of 15 = 1.5 rounded down to 1

Account (C) = 10% of 10 = 1 (no rounding necessary)

To Summarize:

A: initially receives 2 contracts, which is 2/25 of desired (fill ratio = 0.08)

B: initially receives 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: initially receives 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The system then allocates the next (and final) contract to an account with the smallest ratio (i.e. to Account B which currently has a ratio of 0.067).

A: final allocation of 2 contracts, which is 2/25 of desired (fill ratio = 0.08)

B: final allocation of 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: final allocation of 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The execution(s) received have now been allocated in full.

Example #3:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 11 am (ET) the order begins to be executed2 but in very small portions and over a very long period of time. At 12 pm (ET) the order is canceled prior to being executed in full. As a result, only a portion of the order is filled (i.e., 3 of the 50 contracts are filled or 6%). Normally the system initially allocates by rounding fractional amounts down to whole numbers, however for a fill size of less than 4 shares/contracts, IB first allocates based on the following random allocation methodology.

In this case, since the fill size is 3, we skip the rounding fractional amounts down.

For the first share/contract, all A, B and C have the same initial fill ratio and fill quantity, so we randomly pick an account and allocate this share/contract. The system randomly chose account A for allocation of the first share/contract.

To Summarize3:

A: initially receives 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: initially receives 0 contracts, which is 0/15 of desired (fill ratio = 0.00)

C: initially receives 0 contracts, which is 0/10 of desired (fill ratio = 0.00)

Next, the system will perform a random allocation amongst the remaining accounts (in this case accounts B & C, each with an equal probability) to determine who will receive the next share/contract.

The system randomly chose account B for allocation of the second share/contract.

A: 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: 0 contracts, which is 0/10 of desired (fill ratio = 0.00)

The system then allocates the final [3] share/contract to an account(s) with the smallest ratio (i.e. Account C which currently has a ratio of 0.00).

A: final allocation of 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: final allocation of 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: final allocation of 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The execution(s) received have now been allocated in full.

Available allocation Flags

Besides the allocation methods above, user can choose the following flags, which also influence the allocation:

· Strict per-account allocation.

For the initially submitted order if one or more subaccounts are rejected by the credit checking, we reject the whole order.

· “Close positions first”1.This is the default handling mode for all orders which close a position (whether or not they are also opening position on the other side or not). The calculation are slightly different and ensure that we do not start opening position for one account if another account still has a position to close, except in few more complex cases.

Other factor affects allocations:

1) Mutual Fund: the allocation has two steps. The first execution report is received before market open. We allocate based onMonetaryValue for buy order and MonetaryValueShares for sell order. Later, when second execution report which has the NetAssetValue comes, we do the final allocation based on first allocation report.

2) Allocate in Lot Size: if a user chooses (thru account config) to prefer whole-lot allocations for stocks, the calculations are more complex and will be described in the next version of this document.

3) Combo allocation1: we allocate combo trades as a unit, resulting in slightly different calculations.

4) Long/short split1: applied to orders for stocks, warrants or structured products. When allocating long sell orders, we only allocate to accounts which have long position: resulting in calculations being more complex.

5) For non-guaranteed smart combo: we do allocation by each leg instead of combo.

6) In case of trade bust or correction1: the allocations are adjusted using more complex logic.

7) Account exclusion1: Some subaccounts could be excluded from allocation for the following reasons, no trading permission, employee restriction, broker restriction, RejectIfOpening, prop account restrictions, dynamic size violation, MoneyMarketRules restriction for mutual fund. We do not allocate to excluded accountsand we cancel the order after other accounts are filled. In case of partial restriction (e.g. account is permitted to close but not to open, or account has enough excess liquidity only for a portion of the desired position).

Footnotes:

Overview of Dividend Payments in Lieu ("PIL")

Payment In Lieu of a Dividend (“payment in lieu” or “PIL”) is a term commonly used to describe a cash payment to an account in an amount equivalent to the ordinary dividend. Generally, the amount paid is per share owned. In addition, the dividend in most cases is paid quarterly (i.e., four times per year). The dividend payment is classified as follows: (1) ordinary dividend; and/or (2) payment in lieu of dividend. The former designation is for a payment received directly from the issuer or its paying agent. The latter designation is used when a cash payment is received from other than the issuer or the issuer’s agent.

Payment in lieu of an ordinary dividend may be received when the shares have been bought on margin, or when the account has a subsequent margin loan due to borrowing money to facilitate the payment for additional purchases of shares or as the result of a withdrawal from the margin account. Payment in lieu of a dividend may also be received when shares are owed to the brokerage firm and have not been received by the dividend record date.

To better understand the difference between an ordinary dividend and a payment in lieu, we will explain the steps taken by IB to comply with US regulations. Each business day, the Firm analyzes the positions in each customer account, every borrow, every loan, every pledge of shares for each security held by its customers to determine how many shares are held on margin and the associated margin loan balances. For each security that is fully paid, we are required to segregate those shares in a good control location (for example, a depository or a US bank. See KB1964). For shares that are held as collateral for a margin loan we are allowed to hypothecate and re-hypothecate shares valued up to 140 percent of the total debit balance in the customer account (See KB1967).

While the guidelines noted above for segregation of securities are clear, there are exceptions that are outside of the Firm's control. For instance, through no fault of its own, IB may have a deficit in segregated shares due to customer activity that changes the Firm’s overall segregation requirement for a security. This may be for a variety of reasons including a delay in receiving shares that have been loaned out to a counterparty after segregation requirements are recalculated and the Firm has issued a stock loan recall, sales of securities by one or more customers that reduce or eliminate margin loans, the deposit of cash by customers that similarly reduce or eliminate margin loans, or a failure of a counterparty to deliver shares for a trade settlement.

Upon issuing a recall of shares loaned, rules permit the borrower of the shares up to 3 business days to return them. The borrower of the shares is required to return them to us when we issue a recall, but if by business day 3 the shares have not been returned, IB may then issue a buy-in notice to begin the process of regaining possession of the shares. An additional 3 business days is generally needed for the purchased shares to settle and be delivered to the firm. Similarly if a counterparty fails to deliver by settlement date, shares to IB to settle a customer purchase, IB can issue a buy-in notice but the purchase of such shares are also subject to trade settlement in 3 days.

To summarize, if by the record date of a dividend certain shares have not been delivered to IB, the Firm will be paid an amount of cash that is equivalent to the dividend amount, but IB will not receive a qualified dividend payment directly from the issuer. In such cases, the Firm will receive PIL and will have no choice but to allocate such payment in lieu to customer accounts. The firm first allocates PIL to those accounts who hold the shares as collateral for a margin loan. If, after PIL is allocated to all shareholders whose accounts are not fully paid, any portion of PIL remains to be paid, it is allocated on a pro-rata basis to each remaining client account.

Account holders should be aware that a PIL may have different tax consequences than an ordinary dividend and should consult a tax advisor to understand such differences and whether they apply to their particular situation.

Monitoraggio Commissione di esposizione mediante Finestra conto

La Finestra conto fornisce informazioni generali che permettono il monitoraggio del proprio conto in tempo reale. Tali informazioni comprendono i saldi principali quali, per esempio, l'ammontare del capitale proprio e della liquidità, la composizione del portafoglio e i saldi di margine per la verifica della conformità ai requisiti e del potere d'acquisto disponibile. Da questa schermata si ottengono anche informazioni relative all'ultima commissione di esposizione addebitata e una stima della commissione successiva sulla base delle posizioni esistenti.

È possibile aprire la Finestra conto mediante:

• la postazione TWS classica, cliccando sull'icona Conto o selezionando Finestra conto dalla voce Conto del menu (Figura 1)

Figura 1

.jpg)

• la postazione TWS Mosaic, cliccando sulla voce Conto del menu e poi selezionando Finestra conto (Figura 2)

Figura 2

.jpg)

Dopo l'apertura della schermata è necessario scorrere verso il basso fino alla voce Requisiti di margine e poi cliccare sul segno + nell'angolo in alto a destra per espandere la sezione. Le commissioni di esposizione, denominate rispettivamente "ultima" e "prossima attesa", sono ivi dettagliate per ogni categoria di prodotto cui si applicano (es. azioni, petrolio). Si prega di notare che il saldo indicato alla voce "ultima" rappresenta la commissione aggiornata all'ultima data in cui è stata addebitata (si ricorda che le commissioni sono computerizzate in base alle posizioni in essere alla data di chiusura e addebitate di lì a breve). Il saldo "prossimo atteso" rappresenta la commissione attesa alla data di chiusura in essere sulla base dell'attività della posizione rispetto al calcolo precedente (Figura 3).

Figura 3.jpg)

In caso di sezione nascosta è possibile modificare la visualizzazione predefinita facendo un segno di spunta nella casellina a fianco di un elemento affinché tale elemento sia sempre visualizzato.

Si veda l'articolo KB2275 per informazioni sull'utilizzo di Risk Navigator relative alla gestione e alla stima della Commissione di esposizione e il KB2276 per verificare la Commissione di esposizione attraverso la schermata Anteprima ordine.

Anteprima ordine - Controllo impatto commissione di esposizione

IB permette ai titolari del conto di verificare l'eventuale impatto di un ordine sulla Commissione di esposizione attesa mediante una funzionalità pensata per un utilizzo prima dell'inoltro dell'ordine. Tale funzionalità fornisce un preavviso di commissione grazie al quale è possibile modificare l'ordine prima della sua trasmissione e diminuire o annullare la commissione stessa.

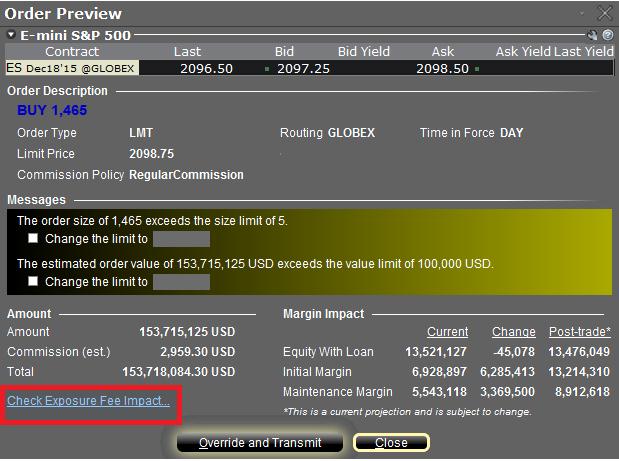

Per attivare questa funzionalità è necessario cliccare con il pulsante destro del mouse sulla riga dell'ordine, dopodiché si aprirà la finestra Anteprima ordine contenente un link denominato "Controllo impatto commissione di esposizione" (si veda il riquadro evidenziato in rosso nella Figura I qui di seguito).

Figura I

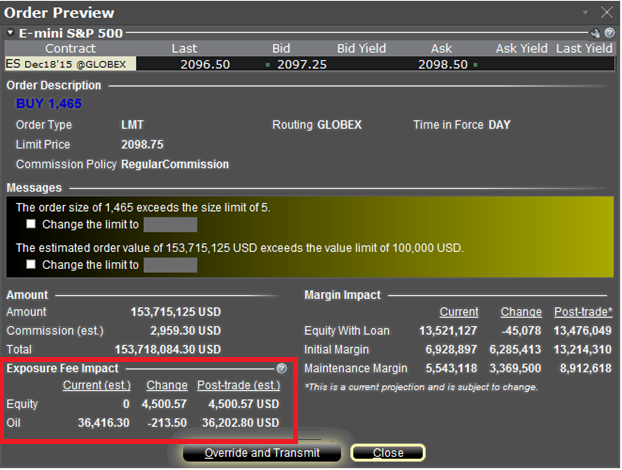

Cliccando sul link si aprirà una finestra raffigurante l'eventuale Commissione di esposizione associata alle posizioni esistenti, la variazione della commissione in caso di ordine processato e la commissione totale risultante una volta processato l'ordine (si veda il riquadro evidenziato in rosso nella Figura II qui di seguito). I saldi sono suddivisi ulteriormente per categoria di prodotto alla quale le commissioni si applicano (es. azioni, petrolio). I titolari del conto possono chiudere la finestra senza inoltrare l'ordine qualora ritengano l'impatto della commissione eccessivo.

Figura II

Si veda l'articolo KB2275 per informazioni sull'utilizzo di Risk Navigator relative alla gestione e alla stima della Commissione di esposizione e il KB2344 per il monitoraggio delle commissioni mediante la Finestra conto

Exposure Fee Monitoring via Account Window

The Account Window provides the high-level information suitable for monitoring one's account on a real-time basis. This includes key balances such as total equity and cash, the portfolio composition and margin balances for determining compliance with requirements and available buying power. This window also includes information relating to the most recently assessed exposure fee and a projection of the next fee taking into consideration current positions.

To open the Account Window:

• From TWS classic workspace, click on the Account icon, or from the Account menu select Account Window (Exhibit 1)

Exhibit 1

• From TWS Mosaic workspace, click on Account from the menu, and then select Account Window (Exhibit 2)

Exhibit 2

After opening the window, scroll down to the Margin Requirements section and click on the + sign in the upper-right hand corner to expand the section. There, the "Last" and "Estimated Next" exposure fees will be detailed for each of the product classifications to which the fee applies (e.g., Equity, Oil). Note that the "Last" balance represents the fee as of the date last assessed (note that fees are computed based upon open positions held as of the close of business and assessed shortly thereafter). The "Estimated Next" balance represents the projected fee as of the current day's close taking into account position activity since the prior calculation (Exhibit 3).

Exhibit 3

To set the default view when the section is collapsed, click on the checkbox alongside any line item and those line items will remain displayed at all times.

Please see KB2275 for information regarding the use of IB's Risk Navigator for managing and projecting the Exposure Fee and KB2276 for verifying exposure fee through the Order Preview screen.

Important Notes

1. The Estimated Next Exposure Fee is a projection based upon readily available information. As the fee calculation is based upon information (e.g., prices and implied volatility factors) available only after the close, the actual fee may differ from that of the projection.

2. Exposure Fee Monitoring via the Account window is only available for accounts that have been charged an exposure fee in the last 30 days

Order Preview - Check Exposure Fee Impact

IB provides a feature which allows account holders to check what impact, if any, an order will have upon the projected Exposure Fee. The feature is intended to be used prior to submitting the order to provide advance notice as to the fee and allow for changes to be made to the order prior to submission in order to minimize or eliminate the fee.

The feature is enabled by right-clicking on the order line at which point the Order Preview window will open. This window will contain a link titled "Check Exposure Fee Impact" (see red highlighted box in Exhibit I below).

Exhibit I

Clicking the link will expand the window and display the Exposure fee, if any, associated with the current positions, the change in the fee were the order to be executed, and the total resultant fee upon order execution (see red highlighted box in Exhibit II below). These balances are further broken down by the product classification to which the fee applies (e.g. Equity, Oil). Account holders may simply close the window without transmitting the order if the fee impact is determined to be excessive.

Exhibit II

Please see KB2275 for information regarding the use of IB's Risk Navigator for managing and projecting the Exposure Fee and KB2344 for monitoring fees through the Account Window

Important Notes

1. The Estimated Next Exposure Fee is a projection based upon readily available information. As the fee calculation is based upon information (e.g., prices and implied volatility factors) available only after the close, the actual fee may differ from that of the projection.

2. The Check Exposure Fee Impact is only available for accounts that have been charged an exposure fee in the last 30 days

Tools Provided to Monitor and Manage Margin

IB provides a variety of tools and information intended to provide account holders with real-time details as to their state of margin compliance so as to avoid forced liquidations. These include the following:

a. Account Window – The account window is available for real-time account activity monitoring. This window will display key values that update with every price change in the portfolio. Included are account balances (cash, Net Liquidation Value, Equity with Loan Value), margin requirements (current, look ahead, overnight and post expiration), and balances available for trading (Available Funds and Excess Equity).

b. Preview Order/Check Margin – Prior to transmitting an order it can be previewed including the impact upon the margin requirement were the order to be executed. Additional information may be found in KB644.

c. Communications – IB will act to send out communications via TWS bulletin and/or email when the margin cushion in an account reaches 10% and a margin deficiency is therefore approaching. Account holders may also create their own margin alerts based upon the margin cushion which, when triggered, may generate email or text message alerts, TWS pop-up messages and flashing rows, and sound alarms.

d. Reports – A Daily Margin Report is made available with Account Management which reflects key margin balances and for portfolio margin accounts, requirements broken down by security class.

In addition, IB provides a Last to Liquidate feature within the TWS Account window that allows customers to specify the positions they would prefer IB liquidate last in the event of a margin deficit. While IB will attempt on a best efforts basis to adhere to such requests, account positions and market conditions may make doing so impractical and IB therefore reserves the right to liquidate in the sequence it deems most optimal.

Trading on margin in an IRA account

IRA accounts, by definition, may not use borrowed funds to purchase securities and must pay for all long stock purchases in full, may not carry short stock positions and may not hold a debit cash balance (in any currency). IRA accounts are eligible to carry futures and option contracts. In addition, IB offers a specific form of IRA account referred to as a “Margin IRA” that allows the account holder to trade with unsettled funds, carry American style option spreads and maintain long balances in multiple currency denominations.

For additional information regarding trading permissions in an IRA account, refer to KB188.

How to determine if you are borrowing funds from IBKR

If the aggregate cash balance in a given account is a debit, or negative, then funds are being borrowed and the loan is subject to interest charges. A loan may still exist, however, even if the aggregate cash balance is a credit, or positive, as a result of balance netting or timing differences. The most common examples of this are as follows:

1. Long vs. Short Currency Balances – accounts holders may borrow cash denominated in one currency if it can be secured by a credit balance in another. Take, for example, a USD base currency account holding a long USD settled cash balance of 10,000, a short EUR settled cash balance of 5,000, with a EUR.USD exchange rate of 1.38:1. Here, for statement reporting and interest computation purposes, the overall cash balance is a USD credit of 3,088 (10,000 – (5,000 * 1.38)). As each currency is subject to a unique funding and reinvestment arrangement, the short balance would be subject to financing costs based upon its benchmark rate and tier. This cost may be offset by any interest earned on the long balance based upon its benchmark rate and tier.

2. Gross Balances by Segment – IBKR’s Universal Account contains multiple sub accounts or segments, each of which holds positions and collateral which, for regulatory and customer protection purposes, may not be commingled. This separation does not allow for netting of balances across segments and a credit in one segment may therefore not offset a debit in another. Take, for example, an IBLLC account holding both securities and commodities positions with the securities segment maintaining a debit cash balance of USD 3,000 and the commodities segment a credit cash balance of USD 8,000. While the account holds an overall net credit balance of USD 5,000, the short balance would be subject to an interest charge which may be partially offset by any interest earned on the long balance.

3. Short Sales – a short sale is a margin transaction in which the account holder is borrowing stock rather than cash. While the proceeds from the short sale are credited to the cash balance of the account, these funds must be posted with the lender of the shares as collateral to secure their return. As a result, and in recognition of the fact that the loan transaction is subject to its own financing terms, the cash collateralizing the loan is excluded for the purpose of determining whether a margin loan exists.

As example, consider an account reporting net liquidating equity (all balances in USD) of 9,000 comprised of a credit cash balance of 4,000, long stock valued at 10,000 and short stock valued at 5,000. In order to determine whether funds are being borrowed to finance the long stock position, the 5,000 portion of the cash pledged as collateral to the lender of the shares is deducted from the overall 4,000 cash balance, resulting in a 1,000 debit. This debit is subject to interest charges and the cash underlying the stock borrow either an interest charge in the case of hard to borrow shares or a short stock rebate if the shares are easy to borrow and reinvestment rates sufficiently high.

4. Unsettled Funds - borrowings are determined based upon settled funds and the time frame by which payment is due or received for a given transaction is product specific (e.g., stocks generally settle in 3 business days, spot currencies 2 and derivatives 1). For statement and trading platform purposes, cash balances are reported on a trade date rather than settlement date basis, as if settlement has completed.

As a result, an account reporting a credit cash balance may, in fact, still be carrying a margin loan if that balance includes proceeds from the sale of stock purchased with borrowed funds awaiting settlement. Similarly, an account may report a trade date based debit balance, but not yet incurring a margin loan and interest charges, as the trade has not yet settled.

For additional information regarding interest calculations, please refer to How Interest is Calculated.