IBSJマルチカレンシーについて

どの通貨で外国商品を取引できますか?

当社が指定する通貨建てで、どの商品でもお取引いただくことができます。

例: キャッシュ口座をお持ちのお客様が、米国株を購入する際の指定通貨は米ドルです。この場合、まず、お客様の保有資金(米ドルまたは他の通貨)で購入代金をカバーできるかをシステムにより判断し、購入に十分な残高がある場合に、注文を取引所に取次ぎます。

- お客様が保有する米ドル残高で注文代金が満たされる場合は、米ドルにて商品を購入します。

- 保有米ドル残高で注文代金が満たされない場合、不足分は他の通貨で保有している資金を当社所定のレートにて自動的に米ドルに交換のうえ、充当します。

- 米国株を売却する場合、売却代金である米ドルは他の通貨に自動交換することなく、米ドルのまま口座に入金されます。

- 米ドルで保有している資金は、米国株の購入に充当することも、お客様の銀行口座に出金することもできます。

- 出金や取引等に関連しない他の通貨への為替交換はできません。

- 入出金が可能な通貨は、日本円、ユーロ、米ドル、英ポンド(入出金対応通貨といいます)です。お客様の口座に出金額相当の残高があるかをシステムにて確認した後、お客様の指定した通貨の残高が指定額を満たしていない場合、不足分をその他の通貨より自動的に交換します。

注意事項

- 当社は、自動通貨交換のための手数料をお客様に別途請求することはありません。口座の仕様上、5米ドル相当以下の通貨の残高は自動的に日本円に交換されます。

- 外貨にて決済された資金をお客様の指示により日本円に交換(自動交換以外)する際は為替取引手数料がかかります。詳細は、当社ホームページにてご確認ください。

- 「入出金対応通貨」とは、お客様が入出金できる通貨をいいます。

FX取引や通貨交換に関連する情報

通貨の交換は、取引(例えば、株式の購入や売却等)とその結果生じるキャッシュフローに関連するものでなければなりません。そのため、お客様は取引プラットフォームにおいて、取引またはマイナス残高を解消する目的以外では通貨交換を行うことができません。

- 当社では、借り入れが発生するようなFX取引はできません。しかし、海外金融商品を取引するために、口座に保有されている資金から取引額相当分を商品の取引通貨へ自動交換します。

- 取引や保有ポジションからのキャッシュフロー(配当など)については、基本的に自動交換はされません。口座の仕様上、5米ドル相当以下の外国通貨の残高は自動的に日本円に交換されます。

- 入出金が可能な通貨は、日本円、ユーロ、米ドル、英ポンドです。お客様の口座に出金額相当の残高があるかをシステムにて確認した後、お客様の指定した通貨の残高が指定額を満たしていない場合、不足分をその他の通貨より自動的に交換します。

- 出金の際に、「出金可能金額を全額出金」のオプションを選択することにより、出金可能なすべての資金を指定通貨にて出金することができます。IBSJは、口座内の全ての対応通貨の残額を残すことなく、出金通貨に自動交換します。

その他、リスク等の詳細に関しましては、IBマルチカレンシー対応口座および外国為替取引に関する書面 をご確認ください。

注意事項

- 当社は、自動通貨交換のための手数料をお客様に別途請求することはありません。口座の仕様上、5米ドル相当以下の通貨の残高は自動的に日本円に交換されます。

- 外貨にて決済された資金をお客様の指示により日本円に交換(自動交換以外)する際は為替取引手数料がかかります。詳細は、当社ホームページにてご確認ください。

- 「入出金対応通貨」とは、お客様が入出金できる通貨をいいます。

- 基準通貨は、日本円となります。

- 出金指示をいただいた時点では、システム上に最大出金可能額(予想値)が表示されます。当該出金可能額全額を指定いただいた場合でも、為替レートの変動により、実際の出金額が異なる場合があります。

入出金が可能な通貨について

IBSJのお客様は、日本円、ユーロ、米ドル、英ポンドで入出金をすることができます。

出金いただく際は、お客様の口座に出金額相当の残高があるかをシステムにて確認した後、お客様の指定した通貨の残高が指定額を満たしていない場合、不足分をその他の通貨より自動的に交換します。

出金の際に、「出金可能金額を全額出金」のオプションを選択することにより、出金可能なすべての現金を出金通貨にて出金することができます。IBSJは、口座内の全ての対応通貨の残額を残すことなく、出金通貨に自動交換します。

その他、リスク等の詳細に関しましては、IBマルチカレンシー対応口座および外国為替取引に関する書面 をご確認ください。

注意事項

- 当社は、自動通貨交換のための手数料をお客様に別途請求することはありません。口座の仕様上、5米ドル相当以下の通貨の残高は自動的に日本円に交換されます。

- 外貨にて決済された資金をお客様の指示により日本円に交換(自動交換以外)する際は為替取引手数料がかかります。詳細は、当社ホームページにてご確認ください。

- 「入出金対応通貨」とは、お客様が入出金できる通貨をいいます。

- 基準通貨は、日本円となります。

- 出金指示をいただいた時点では、システム上に最大出金可能額(予想値)が表示されます。当該出金可能額全額を指定いただいた場合でも、為替レートの変動により、実際の出金額が異なる場合があります。

IBSJ Multi Currency

Can I trade foreign products in supported currencies at Interactive Brokers Securities Japan (IBSJ)?

Yes, clients can trade in any currency that has a product listed in.

For example: Client with a cash account wants to buy a US stock. Our system will check if the client has sufficient available funds in USD or other supported currencies to cover 100% of the trade and, if so, the order will be sent to the exchange.

- If client has enough balance in USD, it will be used for execution of the order.

- If not, IBSJ will automatically convert an equivalent amount of USD from other supported currencies with a positive balance.

- If the same client wishes to sell his USD denominated security at a later date, IBSJ will NOT convert the proceeds back to one of the supported currencies.

- Client can use proceeds in USD for purchasing US stocks or withdraw them.

- Conversion to other currencies not connected to withdrawing funds is not allowed.

- Client can withdraw funds in supported cashiering currencies (JPY, USD, EUR, GBP). If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBSJ will automatically convert positive balances in the supported currencies to the requested one.

Please Note

- IBSJ does NOT charge a commission to clients for automatic currency conversion.

- Commissions for currency conversion used for closing a non-JPY cash balance are presented on our website.

- Supported cashiering currency is a currency in which client can make deposits and withdrawals.

Can I trade Forex and convert currencies at Interactive Brokers Securities Japan (IBSJ)?

Currency conversion at IBSJ must be connected to an investment service transaction (purchasing a stock, for instance) and its resulting cash flows. To comply with this regulation, clients can make a currency conversion in a trading platform only to close the negative balance from borrowing. In other cases, IBSJ makes a conversion automatically.

- The client CANNOT open long positions that create cash debits (loans). Nevertheless, client can open long positions in any foreign product regardless of the currency in which it is denominated. IBSJ will auto convert the value of the transaction from the positive balance in supported currencies held in the account.

- Any positive cash that is generated as the result of a trade or cash flows from a position you hold (e.g. dividends, coupon, interest) will NOT be auto-converted.

- The client can withdraw funds in JPY, EUR, USD, GBP. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBSJ will automatically convert positive balances in the supported currencies to the requested one.

- The client can use the option “Withdraw All Available Cash”, which allows to withdraw all available funds in one currency: supported currencies or base currency. IBSJ will automatically convert positive balances to the requested one without leaving residuals.

For further information please see the IBSJ Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note

- IBSJ does NOT charge clients commissions for automatic currency conversion.

- Commissions for currency conversion used for closing a non-JPY cash balance are presented on our website.

- Supported cashiering currency is a currency in which client can make deposits and withdrawals.

- Base currency: JPY.

- System shows the projected Cash Available for Withdrawal. The final withdrawal amount may differ from the requested due to fluctuation in currency exchange rates.

What currencies are available for deposits and withdrawals at Interactive Brokers Securities Japan (IBSJ)?

IBSJ clients can make deposits in four Supported Cashiering Currencies.

Withdrawals are allowed in base currency and positive balances held in the account. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBSJ will automatically convert positive balances in the supported currencies to the requested one.

Client can use the option “Withdraw All Available Cash”, which allows to withdraw all available funds in one currency: supported currencies or base currency. IBSJ will automatically convert positive balances to the requested one without leaving residuals.

For further information please see the IBSJ Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note

- IBSJ does NOT charge clients commissions for automatic currency conversion.

- Commissions for currency conversion used for closing a non-JPY cash balance are presented on our website.

- Supported cashiering currency is a currency in which client can make deposits and withdrawals.

- Base currency: JPY.

- System shows the projected Cash Available for Withdrawal. The final withdrawal amount may differ from the requested due to fluctuation in currency exchange rates.

「EMIR」: 取引情報蓄積機関への報告義務およびお客様の義務達成をサポートするインタラクティブ・ブローカーズの代行サービス

1. 背景: 2009年、G20は、2008年の金融危機以降、店頭デリバティブ市場の透明性を高め、 取引当事者リスクを低減することを目的とした改革に取り組むことを 約束しました。欧州内でこの約束のほとんどをまとめる欧州市場インフラ規則(「EMIR」)はEUの規則であり、 2012年8月16日に発効となりました。

2. EMIRによる報告義務の対象となる金融銘柄および資産クラス: 次のクラスの店頭および取引所取引のデリバティブ: クレジット、利息、株式、 コモディティ、ならびに外国為替デリバティブ。取引所で取引されるワラントには適用されません。

3. EMIRによる報告義務の対象となる方: 報告義務は通常、自然人を除き、EUで設立されたすべての取引当事者に対して適用されます。適用対象:

* 金融取引先(「FC」)

* 決済基準を超える非金融取引先(「NFC+」)

* 決済基準以下の非金融取引先(「NFC-」)

* 一部の限られた状況においてEU圏外の第三国の事業体(「TCE」)

報告義務は基本的にEUで設立され、デリバティブコントラクトを取引した事業体すべてに適用となります。

4. 金融取引当事者(「FC」): 銀行、投資会社、クレジット機関、保険会社、AIFM管理のUCITS、年金制度、代替投資ファンドが含まれます。代替投資ファンド(「AIF」)はAIFのマネージャーが、「Alternative Investment FundManagers Directive(「AIFMD」)」の下で認可された場合のみ金融機関となるため、EU圏外のファンドがEMIRの報告義務の対象となる可能性があります。

5. 非金融取引当事者(「NFC」): NFCとは、EU 圏内で設立されたFCやクリアリング機関のような清算機関(「CCP」) として定義されるもの以外の事業を指します。NFCはFCに比べ義務が少なくなっていますが、 NFCは「清算基準」を超えた時点でNFC+になり、 FCとほぼ同等の義務の対象となります(担保および評価報告を含め)。 清算基準に満たないNFCはNFC-とみなされます。実際には、自然人以外の人物 (個人またはジョイント口座を持つ1人または1人以上の個人)はNFC-と定義され、

報告義務の対象となります。

インタラクティブ・ブローカーズによるお客様の報告義務の達成をサポートする報告サービスの代行

6. お客様が報告義務を果たすサポートとしてLEIの発行に加え、取引報告に関連して弊社で提供している代行サービス: 上に記載されるよう、FCおよびNFCは両方とも、公認の取引情報蓄積機関に取引(店頭およびETD)を報告する必要があります。この義務は、取引情報蓄積機関を通じて直接行うか、報告管理の部分を取引所やサードパーティ(代理として報告を行う)に委託することによって果たすことができます。

インタラクティブ・ブローカーズでは、業務上、法律上そして規制上の観点から可能な限りLEIの発行を促進し、お客様の同意に基づいて弊社が取引の約定および決済を行うお客様に対し、代理報告を行う意向です。

EMIR報告の対象となるお客様は、今後間もなく弊社のアカウント・マネジメントシステムよりLEIの申請および報告を、インタラクティブ・ブローカーズに委託できるようになります。

弊社では、法律上および規制上の観点から弊社にて評価報告を行うことが許容され、また取引当事者が評価報告を行うよう求められる場合(FCまたはNFC+に該当する場合)に限り、評価報告を行う予定です。

これは、報告用に弊社独自の取引評価を使用することが条件となります。

7EMIR報告の委託は可能なのか: EMIRでは、どちらの取引当事者にもサードパーティへの報告の委託を許可しています。取引当事者または清算機関がサードパーティに報告を委託した場合、報告義務を遵守する最終的な責任はサードパーティにあります。取引当事者または清算機関は、業務を委託するサードパーティが、正しい報告を行っていることを確認する必要があります。ブローカーやディーラーは、純粋に代理人として機能している場合には、報告義務を負いません。ブロック取引が複数の取引になった場合には、それぞれの取引を報告する必要があります。

ファンドおよびサブファンド - EMIRによる義務は取引当事者にありますが、これがファンドおよびサブファンドのことがあります。取引の主体であるファンドまたはサブファンドは、区分(FC、NFC+ またはNFC-)、委任報告の許可、ならびに取引主体識別コード(「LEI」)申請の詳細を提出する必要があります。

8. EMIR 条項 1(4) および 1(5) による免除: EMIR 条項 1(4) および 1(5) により、区分によって特定の事業体がEMIRにの設定する義務から免除される場合があります。条項 1(4)の下に免除を受ける事業体は、EMIRの設定するすべての義務を免除され、また条項 1(5) の下に免除を受ける事業体は、継続して適用となる報告義務以外の義務を免除されます。

9. EMIR 条項 1(4) および 1(5)による免除対象となる事業体: 条項 1(4) は当初、EUの中央銀行、公的債務の管理に関わる公的機関、ならびに国際決済銀行のみに適用されました。

その後、条項 1(4) の適用除外は、米国と日本の中央銀行および債権管理機構に拡大されました。委員会は、外国の中央銀行や債権管理機構に関しても、それらの管轄区において同等の規制が実施されていることの確認ができれば、今後追加される可能性があることを示唆しています。条項 1(5) は大まかに以下の事業体を免除対象としています:

- 国際開発金融機関

- 中央政府が所有し、また保証する非商業的な公共セクターの事業体、ならびに

- 欧州金融安定ファシリティおよび欧州安定メカニズム。

10. 店頭および上場投資デリバティブ: ESMAのレベル1既定、実施技術基準、ならびに規制技術基準において、上場投資デリバティブ(「ETD」)と店頭コントラクトの報告には、なんの違いもありません 。

コントラクトは、それぞれの商品個別の識別子で特定されます。また、それぞれの取引には個別の識別子が必要となります。世界的に同意されている商品識別子がない場合には、ISINコード、Alternative Instruments Identifiers(AII)、またはClassification of FinancialInstruments Codes(CFI)が代替として機能することもあります。

11. インタラクティブ・ブローカーズで使用している取引情報蓄積機関: Interactive Brokers (U.K.) Limited では、CMEグループの一部である、CME ETRのサービスを使用しています。

12. 取引主体識別(「LEI」)の発行

デリバティブの取引を行うすべてのEUの取引当事者は、報告義務の遵守のため、LEIの保有が必要となります。LEIは取引当事者データの報告目的で使用されます。

LEIとは、法人格のある個人や組織に付随し、金融取引の当事者の明確な識別を可能にするユニークな識別子、またはコードです。

「EMIR」: 取引情報蓄積機関の報告義務に関する詳細

13. NFCがNFC+、またはNFC-のどちらであるかを決定する際の基準: 以下の清算基準値のいずれかに違反する場合、これはNFC+の区分を意味します。ポジションは、想定される、30日の移動平均ベースでの計算となります:

• 店頭クレジット・デリバティブコントラクトの想定元本が10億ユーロ

• 店頭株式デリバティブコントラクトの想定元本が10億ユーロ

• 店頭金利デリバティブコントラクトの想定元本が30億ユーロ

• 店頭FXデリバティブコントラクトの想定元本が30億ユーロ

• 店頭コモディティ・デリバティブコントラクトの想定元本が30億ユーロ、ならびに 上に明記されない店頭デリバティブコントラクト

清算基準額に達したかどうかを計算するため、NFCはそのグループ内のすべての非金融事業体(また、これら事業体がEU圏内か圏外かを決定します)の取引を集計する必要がありますが、ヘッジや資金目的のために行われた取引は考慮に入れません。 ここでの「ヘッジ取引」とは、NFCまたはそのグループの商業活動や資金調達活動に直接関連するリスクを軽減するものとして、客観的に測定可能な取引を指します。

14. エクスポージャーの報告: FCおよびNFC+は以下の報告を行う義務があります:

* 各コントラクトの時価評価またはモデル評価価値

* 取引ベースまたはポートフォリベースで計上された、すべての担保の詳細(担保が取引ごとに計上されるのではなく、一連のコントラクトから生じるネットポジションに基づいて計算される場合)

15. 取引情報蓄積機関に報告するスケジュール: 報告開始日は、2014年2月12日になります:

* 2月12日以降に行われるコントラクト取引は取引日 +1

* 2012年8月16日以降のコントラクト取引において建てられたポジションが 2014年2月12日の時点でまだある場合には、 2014年2月14日までに取引情報蓄積機関に報告が必要になります

* 2012年8月16日以前のコントラクト取引において建てられたポジションが 2014年2月12日の時点でまだある場合には、2014年5月13日までに取引情報蓄積機関に報告が必要になります

* 評価および担保は、 2014年8月12日までに取引情報蓄積機関に報告が必要になります

* 2012年8月16日以前、当日またはこれ以降に行われたコントラクト取引において建てられたポジションが 2014年2月12日の時点でない場合には、 2017年2月12日までに取引情報蓄積機関に報告が必要になります。

16. 報告が必要となる内容および時期: 各取引の取引当事者(取引当事者データ)およびコントラクトそのもの(共通データ)に関する情報の報告が必要になります。

取引当事者データに関連しては26項目、また共通データに関連しては59項目の報告が必要となります。これらの項目は、取引情報蓄積機関に報告が必要となる最小限の内容に関するESMAの規制技術基準付属書の表1および表2に記載されています。

取引当事者および清算機関は、以下の場合に報告が必要となります:

* コントラクトが締結した時

* コントラクトが変更された時

* コントラクトが終了した時

締結、変更、終了の翌営業日内に報告する必要があります。

17. 報告が必要となる内容および報告責任者: 報告は、店頭デリバティブおよび取引所で取引されるデリバティブの両方に必要となります。報告義務は、区分には関係なく取引当事者に適用されます。以下にご注意下さい:

* 評価および担保の報告が必要となるのは、FCおよびNFC+のみです。

* 両タイプの取引先は通常、すべての取引を報告する必要があります。

この情報はインタラクティブ・ブローカーズで清算されるお客様のみを対象とします

留意点: 上記の情報は規制に対する包括的、完全、または確定的な解釈をであることを意図するものではなく、ESMAによるEMIR規制とそれに伴う取引レポジトリの報告義務のサマリーとなります。

Multi-Currency Trading at IBKR Central Europe

For Cash accounts (one without investment loan permissions), client can trade foreign products in all 10 supported currencies.

For example: Client with a cash account wants to buy a US stock. Our system will check if the client has sufficient available funds in USD or other supported currencies to cover 100% of the trade and, if so, the order will be sent to the exchange.

- If client has enough balance in USD, it will be used for execution of the order.

- If not, IBCE will automatically convert an equivalent amount of USD from other supported currencies with a positive balance.

- If the same client wishes to sell his USD denominated security at a later date, IBCE will NOT convert the proceeds back to one of the supported currencies.

- Client can use proceeds in USD for purchasing US stocks or withdraw them.

- Conversion to other currencies not connected to withdrawing funds is not allowed.

- Client can withdraw funds in Major Currencies, Home currency and positive balances held in the account. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBCE will automatically convert positive balances in the supported currencies to the requested one.

For Margin accounts (investment loan accounts), you can trade foreign products in supported currencies and have transactions that result in negative cash balances.

For example: Client with a margin account wants to buy an EU stock. Our system will check if the client has sufficient available funds in EUR or other supported currencies to meet initial margin requirements, and, if so, the order will be sent to the exchange.

- If client borrows EUR, he can decide what to do with the negative EUR balance. This negative balance can be closed by converting from any other supported currency or remain in the account.

- If the same client wishes to sell his EUR denominated security at a later date, IBCE will NOT convert the proceeds back to one of the supported currencies.

- Client can use proceeds in EUR for purchasing EU stocks or withdraw them.

- Conversion to other currencies not connected to withdrawing funds is not allowed.

- Client can withdraw funds in Major Currencies, Home currency and positive balances held in the account. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBCE will automatically convert positive balances in the supported currencies to the requested one.

For further information please see the IBCE Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note:

- IBCE does NOT charge clients for automatic currency conversion.

- Commissions for currency conversion used for closing a negative balance are presented on our website.

- Supported currency is a currency in which client can make deposits and hold a positive balance: EUR, USD, CHF, GBP, HUF, CZK, PLN, NOK, DKK and SEK.

- Major currencies: USD and EUR.

- Home currency: Currency of client’s country of legal residence.

For Cash accounts (one without investment loan permissions), you can trade foreign products in non-supported currencies. IBCE will auto convert the value of the transaction from the positive balance in supported currencies held in the account.

For example: Client with a cash account wants to buy a CAD stock. Our system will check if the client has sufficient available funds in the supported currencies to cover 100% of the trade and, if so, the order will be sent to the exchange.

On trade date, IBCE will automatically convert an equivalent amount of CAD from the positive balance in supported currencies held in the account, leaving no residual CAD cash balance in the account at the end of the day.

- If the same client wishes to sell his CAD denominated security at a later date, IBCE will auto convert the proceeds back to the base currency.

- The same process occurs when cash flows are generated from positions (e.g. dividends, interest). Conversion takes place when the cash is credited to or debited from the account, not when it is accrued.

For Margin accounts (one without investment loan permissions), you can trade foreign products in non-supported currencies and have transactions that result in negative cash balances. Proceeds and all positive balances in non-supported currencies will be automatically converted back to the base currency.

For example: Client with a margin account wants to buy a CAD stock. Our system is checking if the client has sufficient available funds in supported currencies to meet initial margin requirements and, if so, the order will be sent to the exchange.

- Client can decide what to do with the negative CAD balance. This negative balance can be closed by converting from any other supported currency or remain in the account.

- If the same client wishes to sell his CAD stock at a later date, IBCE will automatically convert the proceeds to the base currency as CAD is not a supported currency.

For further information please see the IBCE Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note:

- IBCE does NOT charge clients for automatic currency conversion.

- Commissions for currency conversion used for closing a negative balance are presented on our website.

- Supported currency is a currency in which client can make deposits and hold a positive balance: EUR, USD, CHF, GBP, HUF, CZK, PLN, NOK, DKK and SEK.

Currency conversion at IBCE must be connected to an investment service transaction (purchasing a stock, for instance) and its resulting cash flows. To comply with this regulation, clients can make a currency conversion in a trading platform only to close the negative balance from borrowing. In other cases, IBCE makes a conversion automatically.

- For Margin accounts, the client can open long positions that create cash debits (loans) in any currency. IBCE will not auto-convert your transaction but will create an investment loan in the currency of the trade. It will be the client’s discretion when to initiate a currency conversion to close the negative balance in part or in full.

- For Cash accounts, the client CANNOT open long positions that create cash debits (loans). Nevertheless, client can open long positions in any foreign product regardless of the currency in which it is denominated. IBCE will auto convert the value of the transaction from the positive balance in supported currencies held in the account.

- For both Margin and Cash accounts, any positive cash that is generated as the result of a trade or cash flows from a position you hold (e.g. dividends, coupon, interest) will NOT be auto-converted if it is the supported currency (EUR, USD, CHF, GBP, HUF, CZK, PLN, DKK, SEK and NOK).

- For both Margin and Cash accounts, any positive cash that is generated as the result of a trade or cash flows from a position you hold (e.g. dividends, coupon, interest) will be auto-converted if it is NOT the supported currency.

- For both Margin and Cash accounts, the client can withdraw funds in Major Currencies, Home currency and positive balances held in the account. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBCE will automatically convert positive balances in the supported currencies to the requested one.

- For both Margin and Cash accounts, the client can use the option “Withdraw All Available Cash”, which allows to withdraw all available funds in one currency: Major Currencies or Home currency. IBCE will automatically convert positive balances in the supported currencies to the requested one without leaving residuals.

For further information please see the IBCE Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note:

- IBCE does NOT charge clients for automatic currency conversion.

- Commissions for currency conversion used for closing a negative balance are presented on our website.

- Supported currency is a currency in which client can make deposits and hold a positive balance: EUR, USD, CHF, GBP, HUF, CZK, PLN, NOK, DKK and SEK.

- Major currencies: USD and EUR.

- Home currency: Currency of client’s country of legal residence.

- System shows the projected Cash Available for Withdrawal. The final withdrawal amount may differ from the requested due to fluctuation in currency exchange rates.

- Interactive Brokers Central Europe accounts are not allowed to withdraw funds on margin due to regulatory reasons.

- The same currency pairs can be traded as Forex CFD. Contracts For Difference are complex instruments, and we invite you to carefully review the CFDs risk warnings before trading these instruments.

IBCE clients can make deposits in all 10 Supported Currencies.

Withdrawals are allowed in Major currencies, Home currency and positive balances held in the account. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBCE will automatically convert positive balances in the supported currencies to the requested one.

Client can use the option “Withdraw All Available Cash”, which allows to withdraw all available funds in one currency: Major Currencies or Home currency. IBCE will automatically convert positive balances in the supported currencies to the requested one without leaving residuals.

For further information please see the IBCE Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note:

- IBCE does NOT charge clients for automatic currency conversion.

- Supported currency is a currency in which client can make deposits and hold a positive balance: EUR, USD, CHF, GBP, HUF, CZK, PLN, NOK, DKK and SEK.

- Major currencies: USD and EUR.

- Home currency: Currency of client’s country of legal residence.

- System shows the projected Cash Available for Withdrawal. The final withdrawal amount may differ from the requested due to fluctuation in currency exchange rates.

- Interactive Brokers Central Europe accounts are not allowed to withdraw funds on margin due to regulatory reasons.

- The changes mentioned above are effective since October 17, 2022.

ロシア・ルーブル(RUB)に関する重要なお知らせ

IBKRでは多くの金融機関と同様に、ロシア・ルーブル(RUB)へのエクスポージャーを減らしており、出金および通貨の換金を含めるすべての出納業務を停止致しました。

具体的には以下のようになります:

ルーブルでの入金: IBKRではルーブルでのご入金の受付を終了致しました。 ルーブルでの入金は、今後すべて拒否されます。

IBKRでは、お客様が口座をお持ちのIBKR事業体により、ルーブルの残高を定期的に米ドルまたはユーロに変換します。

|

IBKR事業体 |

変換先通貨 |

|

IBLLC |

USD |

|

IBCE |

EUR |

|

IBUK |

EUR |

|

IBIE |

EUR |

|

その他すべて |

USD |

ルーブルでの出金: IBKRではルーブルの出金を受付けることができません。

基準通貨: 現在IBKRにおきましては、ルーブルを基準通貨として保有することはできません。 これまでルーブルを基準通貨としてご利用されていた場合、どのIBKR事業体に口座が保管されているかによって米ドルまたはユーロに弊社にて変換致しました(上記の表をご参照下さい)。

IBKRでは、適用となるすべての制裁法の遵守に尽くします。ご理解ご協力のほどよろしくお願い申し上げます。

IMPORTANT NOTICE REGARDING THE RUSSIAN RUBLE (RUB)

In line with many financial institutions, IBKR has reduced exposure to the Russian Ruble, (“RUB”) and has discontinued all cashiering services for Russian Rubles, including all withdrawals and currency conversions.

Specifically:

Deposits in RUB: IBKR is no longer accepting deposits of RUB. Any deposit in RUB will be rejected.

IBKR will periodically convert RUB balances to USD or EUR, depending on the IBKR entity with which you have an account.

|

IBKR Entity |

Target Currency |

|

IBLLC |

USD |

|

IBCE |

EUR |

|

IBUK |

EUR |

|

IBIE |

EUR |

|

All Others |

USD |

Withdrawals in RUB: IBKR is not able to accommodate RUB withdrawals at this time.

Base Currency: IBKR does not currently allow clients to maintain RUB as their base currency. If you previously used RUB as your base currency, we converted it to USD or EUR depending on which IBKR entity your account is with (see chart above).

IBKR is fully committed to complying with all applicable sanctions laws. We appreciate your cooperation and your business.

ストップ注文の使用に関する追加情報

米国の株式市場では、時おり極端な変動や価格の崩壊が発生することがあります。 この現象は長引くこともあれば、短時間で終わることもあります。ストップ注文は価格の下落や市場の変動を助長する役割を果たし、トリガー価格から大幅に離れた価格で約定する可能性があります。

投資家は、株価が下落した場合や損失に歯止めをかけるため、売りのストップ注文を利用してポジションの利益を保護することができます。また、ショートポジションを保有している場合、価格が上昇する際には買いのストップ注文を利用して損失に歯止めをかけることができますが、ストップ注文は一度トリガーされると成行注文になるため、市場の状況変動が激しく予想価格から上下どちらとも大幅に離れた価格で約定する場合には特に、成行注文に伴うリスクにすぐに直面することになります。

ストップ注文はポジションの価格をモニターするにあたって便利なツールではありますが、ストップ注文に伴う潜在的なリスクがないわけではありません。ストップ注文を利用される際には、以下の点にご注意ください:

· ストップ価格は保証される約定価格ではありません。「ストップ注文」は「ストップ価格」に達した時点で「成行注文」となり、この結果となる注文は、その時点の市場価格で全て速やかに約定する必要があります。このため、ストップ注文が最終的に約定する価格は、投資家の「ストップ価格」と大幅に異なることがあります。従って、成行注文となったストップ注文が速やかに約定する可能性がある半面、市場の変動が激しい場合には、約定価格がストップ価格と大幅に異なる可能性があります。

· ストップ注文は短期で劇的な価格変動にトリガーされることがあります。市場の変動が激しい場合には短期間で株価が大幅に変動し、ストップ注文の約定をトリガーする可能性があります(また、後で以前の株価水準で取引を再開する可能性があります)。このような状況でストップ注文がトリガーされた場合、注文が期待に沿わない価格で約定することや、またその後、同じ取引日中に価格が安定する可能性がある事を理解する必要があります。

· 極端な変動の際、売りのストップ注文は価格の下落を悪化させることがあります。売りのストップ注文の発注により、有価証券の価格の下落につながる事があります。価格が急激に下落している際にストップ注文が発注されると、ストップ価格から大幅に低い価格で約定する可能性が高くなります。

· ストップ注文に「指値」を付けることによって、リスクによってはいくらか管理できるようになります。「指値価格」付きのストップ注文(「ストップリミット注文」)は、株価が「ストップ価格」に到達するかこれを上回ると「指値注文」になります。 「指値注文」は、指定した価格(「指値価格」)かそれよりも良い価格で銘柄を売買する注文です。普通のストップ注文の代わりにストップリミット注文を利用すると、株価をより確実にすることができますが、売り注文の場合、選択する指値価格以下(買い注文の場合は指値価格以上)での約定はありえないため、注文が全く約定しない可能性も考慮に入れておく必要があります。価格には関係なくすぐに約定することよりも、希望する目標価格を達成することを優先する場合には、指値注文の利用を検討する必要があります。

· ストップ注文に伴うリスクは市場の流動性がない時間や、市場の変動がより激しいオープンやクローズ時にはより高くなることがあります。これは流動性の低い株式の場合、その時点での価格レベルでは売却が難しく、市場の変動が激しい場合には特に価格が激しく上下する可能性があるため、特に重要になります。流動性の低い市場の時間帯や、市場の変動がより激しいオープンやクローズ時前後にストップ注文が発注されるのを防ぐため、ストップ注文の発注時間帯を制限することや、他の注文タイプの利用を検討する必要があります。

· ストップ注文に伴うリスクを考慮し、取引ニーズに一致するその他の注文タイプの利用も慎重に検討する必要があります。

口座に保有されていない通貨建ての商品を取引する場合

特定の商品の購入と決済にどの通貨が必要となるかは、IBKRではなく上場取引所によって決定されます。例として、お客様が保有されていない通貨建ての有価証券を購入する取引を行うとし、またお客様がマージン口座と十分な証拠金を保有される場合、IBKRではこの資産に対してローンを組みます。これは、クリアリングハウスとの取引を、指定されている通貨のみで決済する義務がIBKRにあるためです。ローンおよびこれによる金利の発生をご希望でない場合には、あらかじめ必要となる通貨と金額を口座に入金するか、口座内の資金を両替する必要があります。どちらもTWSより、IdealPro(USD 25,000または同等額以上の場合)または奇数ロット(USD 25,000または同等額以下の場合)を利用してできます。

また、ある通貨建ての有価証券ポジションを決済すると、この通貨が口座に選択されている基準通貨であるかどうかに関わらず、収益はこの通貨に留まることにご注意下さい。よってこういった収益は通貨を両替するか、またはこの収益をその他の類似の通貨建ての商品に利用するまで、基準通貨に対する為替レートのリスクの対象となります。

Glossary terms:

デイリーアクティビティーステートメントの「Cash FX Translation Gain/Loss」の項目は何を表し、どのように計算されているのですか?

概観:

ステートメントの作成にあたり、お客様の口座資産の包括的なスナップショットをご提供するために、お客様が基準通貨として指定した通貨以外の通貨で建てられたお客様の口座のロングまたはショートの現金残高は、その時点で実勢為替レートで換算する必要があります。為替レートは期間ごとに変動する傾向があるため、この変換処理により、現金FX換算残高はプラス(すなわち利益)またはマイナス(すなわち損失)になる可能性があります。 これらの損益は時価計算(すなわち、すべての非基軸通貨の残高が終日の為替レートで決済されたかのような計算)であり、実際の損益は非基軸通貨の残高が決済されるまで確定しないことに留意する必要があります。

ある非基軸通貨の現金為替換算損益は、まず、毎日の計算書期間の前後における基軸通貨の換算レートの差(為替レートC – 為替レートP、レートは各計算書の基軸通貨の為替レート欄に記載されています)を計算して求められます。この差額(プラスまたはマイナス)に、当明細書期間の開始時の現金残高を乗じて、現金為替換算の利益(プラスの場合)または損失(マイナスの場合)を決定します。基軸通貨以外のすべての明細(取引の純売却代金・純購入代金、手数料、利息など)は、通貨換算のために期末時点で計上されるため、定義上、換算損益はありません。

Glossary terms:

IBKR Metals CFDs – Facts and Q&A

概観:

The following article is intended to provide a general introduction to London Gold and Silver Contracts for Differences (CFDs) issued by IBKR.

Please follow these links for information on IBKR Share CFDs, Index CFDs and Forex CFDs.

Risk Warning

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage.

61% of retail investor accounts lose money when trading CFDs with IBKR.

You should consider whether you understand how CFDs work and whether you can afford to take the

high risk of losing your money.

ESMA Rules for CFDs (Retail Clients only)

The European Securities and Markets Authority (ESMA) has enacted new CFD rules effective 1st August

2018.

The rules include: 1) leverage limits on the opening of a CFD position; 2) a margin close out rule on a per

account basis; and 3) negative balance protection on a per account basis.

The ESMA Decision is only applicable to retail clients. Professional clients are unaffected.

Please refer to the following articles for more detail:

ESMA CFD Rules Implementation at IBKR (UK) and IBKR LLC

ESMA CFD Rules Implementation at IBIE and IBCE

Introduction

A London Gold CFD enables you to have exposure to price movements of physical Gold without actually owning it. A London Gold CFD is an agreement between you and IBKR to exchange the difference in price of the underlying over a period of time. The difference to be exchanged is determined by the change in the reference price of the underlying. Thus, if the price of physical Gold traded on the London bullion market rises and you are long the CFD, you receive cash from IBKR and vice versa. A London Gold CFD can be bought long or sold short to suit your view of market direction in the future.

Contract Specifications

| Contract | IBKR Symbol | Per Trade Fee | Minimum per Order | Multiplier |

| London Gold | XAUUSD | 0.015% | USD 2.00 | 1 |

| London Silver | XAGUSD | 0.03% | USD 2.00 | 1 |

Price Determination

The IBKR London Gold and Silver CFDs reference physical Gold and Silver traded on the London bullion market. The London bullion market is a wholesale over-the-counter market for the trading of precious metals. Trading is conducted among members of the London Bullion Market Association (LBMA). Most of the members are major international banks.

IBKR receives quote streams from approximately 10 such major banks, in much the same way it does for cash forex. IBKR Smart routes between the banks, and the best available price at any given time becomes the reference price for the CFDs. IBKR does not add a spread to the banks’ quotes.

Low Commissions and Financing Rates: Unlike other CFD providers IBKR charges a transparent

commission, rather than widening the spread. Commission rates are only 0.015% for London Gold and 0.03% for London Silver. Overnight financing rates are just benchmark +/- 1.5% (an additional 1% surcharge is added for retail accounts).

Transparent Quotes: Because IBKR does not widen the spread, the Metals CFD quotes accurately

represent the spreads and price movements of the related cash metal, as described above.

Margin Efficiency: IBKR establishes house-margin requirements based on historic volatility of the

underlying and other factors. Retail clients are subject to regulatory minimum initial margins of 5% for

London Gold or 10% for London Silver.

Trading Permissions: Same as for Share and Index CFDs.

Market Data Permissions: Metals CFD market data is free, but a permission is required for system

reasons.

Worked Trade Example (Professional Clients):

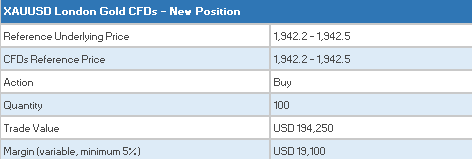

You purchase 100 XAUUSD CFDs at $1,942.5 for USD 194,250 which you then hold for 5 days.

![]()

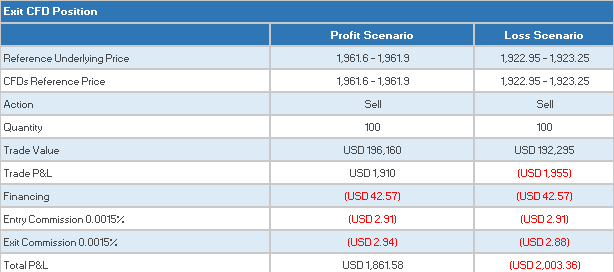

Closing the Position

CFD Resources

Below are some useful links with more detailed information on IB’s CFD offering:

Frequently asked Questions

Are short Metals CFDs subject to forced buy-in?

No.

Can I take delivery of the underlying metal?

No, IBKR does not support physical delivery for Metals CFDs.

Are there any market data requirements?

The market data for Metal CFDs is free, and is included the market data for Index CFDs. However, you need to subscribe to the permission for system reasons. To do this, log into Account Management, and click through the following tabs: Settings/User Settings/Trading Platform/Market Data Subscriptions. Alternatively you can set up an Index or Metals CFD in your TWS quote monitor and click the “Market Data Subscription Manager” button that appears on the quote line.

How are my CFD trades and positions reflected in my statements?

If you are a client of IBKR (U.K.) or IBKR LLC, your CFD positions are held in a separate account segment identified by your primary account number with the suffix “F”. You can choose to view Activity Statements for the F-segment either separately or consolidated with your main account. You can make the choice in the statement window in Account Management.

If you are a client of other IBKR entities, there is no separate segment. You can view your positions normally alongside your non-CFD positions.

In what type of IB accounts can I trade CFDs e.g., Individual, Friends and Family,

Institutional, etc.?

All margin and cash accounts are eligible for CFD trading.

Can I trade CFDs over the phone?

No. In exceptional cases we may agree to process closing orders over the phone, but never opening

orders.

Can anyone trade IB CFDs?

All clients can trade IB CFDs, except residents of the USA, Canada, Hong Kong, New Zealand and

Israel. There are no exemptions based on investor type to the residency-based exclusions.