IBSJ Multi Currency

Can I trade foreign products in supported currencies at Interactive Brokers Securities Japan (IBSJ)?

Yes, clients can trade in any currency that has a product listed in.

For example: Client with a cash account wants to buy a US stock. Our system will check if the client has sufficient available funds in USD or other supported currencies to cover 100% of the trade and, if so, the order will be sent to the exchange.

- If client has enough balance in USD, it will be used for execution of the order.

- If not, IBSJ will automatically convert an equivalent amount of USD from other supported currencies with a positive balance.

- If the same client wishes to sell his USD denominated security at a later date, IBSJ will NOT convert the proceeds back to one of the supported currencies.

- Client can use proceeds in USD for purchasing US stocks or withdraw them.

- Conversion to other currencies not connected to withdrawing funds is not allowed.

- Client can withdraw funds in supported cashiering currencies (JPY, USD, EUR, GBP). If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBSJ will automatically convert positive balances in the supported currencies to the requested one.

Please Note

- IBSJ does NOT charge a commission to clients for automatic currency conversion.

- Commissions for currency conversion used for closing a non-JPY cash balance are presented on our website.

- Supported cashiering currency is a currency in which client can make deposits and withdrawals.

Can I trade Forex and convert currencies at Interactive Brokers Securities Japan (IBSJ)?

Currency conversion at IBSJ must be connected to an investment service transaction (purchasing a stock, for instance) and its resulting cash flows. To comply with this regulation, clients can make a currency conversion in a trading platform only to close the negative balance from borrowing. In other cases, IBSJ makes a conversion automatically.

- The client CANNOT open long positions that create cash debits (loans). Nevertheless, client can open long positions in any foreign product regardless of the currency in which it is denominated. IBSJ will auto convert the value of the transaction from the positive balance in supported currencies held in the account.

- Any positive cash that is generated as the result of a trade or cash flows from a position you hold (e.g. dividends, coupon, interest) will NOT be auto-converted.

- The client can withdraw funds in JPY, EUR, USD, GBP. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBSJ will automatically convert positive balances in the supported currencies to the requested one.

- The client can use the option “Withdraw All Available Cash”, which allows to withdraw all available funds in one currency: supported currencies or base currency. IBSJ will automatically convert positive balances to the requested one without leaving residuals.

For further information please see the IBSJ Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note

- IBSJ does NOT charge clients commissions for automatic currency conversion.

- Commissions for currency conversion used for closing a non-JPY cash balance are presented on our website.

- Supported cashiering currency is a currency in which client can make deposits and withdrawals.

- Base currency: JPY.

- System shows the projected Cash Available for Withdrawal. The final withdrawal amount may differ from the requested due to fluctuation in currency exchange rates.

What currencies are available for deposits and withdrawals at Interactive Brokers Securities Japan (IBSJ)?

IBSJ clients can make deposits in four Supported Cashiering Currencies.

Withdrawals are allowed in base currency and positive balances held in the account. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBSJ will automatically convert positive balances in the supported currencies to the requested one.

Client can use the option “Withdraw All Available Cash”, which allows to withdraw all available funds in one currency: supported currencies or base currency. IBSJ will automatically convert positive balances to the requested one without leaving residuals.

For further information please see the IBSJ Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note

- IBSJ does NOT charge clients commissions for automatic currency conversion.

- Commissions for currency conversion used for closing a non-JPY cash balance are presented on our website.

- Supported cashiering currency is a currency in which client can make deposits and withdrawals.

- Base currency: JPY.

- System shows the projected Cash Available for Withdrawal. The final withdrawal amount may differ from the requested due to fluctuation in currency exchange rates.

“EMIR”:交易報告庫報告義務和盈透證券的委託報告服務

1. 背景:2008年金融危機爆發後,G20于2009年承諾推行一系列改革,旨在提高場外衍生品市場的透明度降低對手方風險。該等承諾大多數通過《歐洲市場基礎設施監管法規》(“EMIR”)在歐盟得以落實。EMIR是歐盟制定的監管法規,于2012年8月16日生效。

2. 根據EMIR可報告的金融産品和資産類別:以下資産類別的場外和交易所交易衍生品:信貸、利息、股票、商品和外匯衍生品。交易所交易的權證不需要報告。

3. 誰需要進行EMIR報告:正常情况下,所有在歐盟成立的交易對手方均需進行報告,不包括自然人。報告義務適用于:

* 金融交易對手方(“FC”)

* 高于清算門檻的非金融交易對手方(“NFC+”)

* 低于清算門檻的非金融交易對手方(“NFC-”)

* 某些極少數情况下歐盟以外的第三國實體(“TCE”)

基本上,任何在歐盟成立的且參與衍生品合約交易的實體都需要進行報告。

4. 金融交易對手方(“FC”):包括銀行、投資公司、信貸機構、保險公司、可轉讓證券集合投資計劃(UCITS)和養老金計劃以及由另類投資基金經理(AIFM)管理的另類投資基金。另類投資基金(AIF)只有在其基金經理系根據另類投資基金經理指令(AIFMD)獲得授權的情况下才會成爲金融交易對手方,因此,位于歐盟以外的基金可能會需要遵守EMIR報告要求。

5. 非金融交易對手方(“NFC”):非金融交易對手方是除FC和中央對手方(CCP)(如清算所)以外的在歐盟成立的企業。NFC承擔的義務比FC少。但是,如果突破了“清算門檻”,NFC就會成爲高于清算門檻的非金融交易對手方(“NFC+”),這時,其承擔的義務就與FC的幾乎一樣了(包括抵押品和估值報告)。低于清算門檻的非金融交易對手方稱爲NFC-。事實上,除自然個人(即單個個人或操作一個聯名賬戶的多名個人

)均被定義爲NFC-,需要承擔報告義務。

盈透證券的委托報告服務可助您履行報告義務

6. 盈透證券提供哪些服務幫助客戶履行報告義務(即盈透證券會提供委托交易報告服務和幫助簽發LEI嗎):如上文所述,FC和NFC都必須向授權交易報告庫(TR)上報其交易(場外和交易所交易衍生品)的詳細信息。該等義務可直接通過交易報告庫解除,也可以通過將報告操作委托給對手方或第三方(代爲提交報告)來達成。

對于由其提供執行和清算服務的客戶,盈透證券幫助簽發LEI幷提供委托報告服務,該等服務須征得客戶同意,幷且只在運營、法律和監管允許的範圍內提供。

如果您需要進行EMIR報告,很快您便可以登錄IB賬戶管理系統申請LEI幷將報告委托給盈透證券。

我們還會納入估值報告,但只有在法律和監管允許的範圍內,且在對手方被要求上報的情况下(即對手方是FC或NFC+的情况下)才會進行。

但是,盈透證券會使用自己的交易估值進行報告。

7. EMIR報告可以委托嗎:EMIR允許交易的任意一方將報告委托給第三方。交易的任意一方或CCP將報告委托給了第三方後,仍對遵守報告義務負有最終責任。同樣,交易的任意一方或CCP必須確保接受其委托的第三方正確地進行報告。經紀商和交易商如果僅僅只是以代理的身份行事則沒有報告義務。如果一筆大宗買賣導致出現多筆交易,則每筆交易都需上報。

基金與子基金 - EMIR規定的義務是針對交易對手方而言的,而交易對手方可能是基金或子基金。作爲交易主角的基金或子基金須提供有關其分類(FC、NFC+或NFC-)的詳細信息,還須提供委托報告和法律實體識別號碼(“LEI”)申請相關 的授權。

8. EMIR第1(4)和1(5)條的豁免規定:EMIR第1(4)和1(5)條提到,某些實體根據其分類可免除EMIR規定的部分或全部義務。具體來說,第1(4)條的豁免實體可免除EMIR規定的所有義務,而第1(5)條的豁免實體可免除報告義務以外的所有義務,也就是仍須履行報告義務。

9. 符合EMIR第1(4)條和1(5)條要求的實體:第1(4)條最初只適用于歐盟國家的中央銀行、涉及公共債務管理的歐盟公共機構和國際清算銀行。後來,

第1(4)條豁免的適用範圍得以擴展,納入了美國和日本的的中央銀行和債務管理辦公室。歐盟委員會表示,未來會有更多外國中央銀行和債務管理辦公室被納入豁免範疇,前提是委員會確信該等行政轄區內有同等力度的監管。第1(5)條對以下類別的實體予以豁免:

- 多邊開發銀行;

- 由中央政府所有且提供擔保的非商業公營實體;以及

- 歐洲金融穩定基金和歐洲穩定機制。

10. 場外和交易所交易衍生品:從第一層法規、執行技術標準和歐洲證券和市場管理局(ESMA)的監管技術標準來看,交易所交易衍生品和場外交易合約的報告幷沒有什麽不同。

合約會采用獨一無二的産品識別碼進行識別。此外,交易還需要有獨一無二的交易識別碼。如果沒有一個全球公認的産品識別碼系統,則建議考慮用國際證券識別碼(ISIN)、另類産品識別碼(AII)或金融産品分類編碼(CFI)作爲替代。

11. 盈透證券使用的交易報告庫:盈透證券(英國)有限公司將使用CME ETR(從屬CME集團)的服務。

12. LEI的簽發

所有參與衍生品交易的歐盟交易對手方均必須持有LEI才能履行報告義務。LEI將用于報告交易對手方數據。

LEI是與法人或法律結構挂鈎的唯一識別號碼或代碼,可供準確識別金融交易的各方。

“EMIR”:有關報告義務的更多信息

13. 用于確定一個NFC是NFC+還是NFC-的門檻值:超出下方任意一項清算門檻均意味著將被歸類爲NFC+。持倉必須按30天滾動平均值計算(名義價值):

• 場外信用衍生品合約爲10億歐元總名義價值;

• 場外股票衍生品合約爲10億歐元總名義價值;

• 場外利率衍生品合約爲30億歐元總名義價值;

• 場外外匯衍生品合約爲30億歐元總名義價值;

• 場外大宗商品衍生品合約和上方未提及的其它場外衍生品合約爲30億歐元總名義價值。

在計算是否突破清算門檻時,NFC必須將其集團內所有非金融實體的交易加總在一起(需確定該等實體是在歐盟以內還是在歐盟以外),但要减去爲了對沖或財務目的進行的交易。這裏的“對沖交易”是指客觀可衡量爲降低與NFC或其所屬集團的商業活動或融資活動直接相關之風險的交易。

14. 風險敞口報告:FC和NFC必須上報以下信息:

* 各合約的按市值計價或按模型計價價值

* 提供的所有抵押品的詳細信息,按交易或者按投資組合(即按一系列合約産生的淨持倉計算抵押品,而不是按單筆交易提供的抵押品)報告

15. 向交易報告庫進行報告的時間安排:開始報告的日期爲2014年2月12日:

* 2月12日或之後達成的新合約,按T+1報告;

* 由2012年8月16日或之後達成之合約産生的、且到2014年2月12日仍未平倉的倉位必須在2014年2月12日之前上報至交易報告庫;

* 由8月16日之前達成之合約産生的、且到2014年2月12日仍未平倉的合約必須在2014年5月13日之前上報至交易報告庫;

* 估值和抵押品必須在2014年8月12日之前上報至交易報告庫;

* 2012年8月16日之前、當天或之後達成的合約,如果到2014年2月12日已平倉,則必須在2017年2月12日之前上報至交易報告庫。

16. 需要上報的信息以及上報時間:必須上報每筆交易的交易對手方(交易對手方數據)和合約(通用數據)。

交易對手方數據有26項,通用數據有59項。ESMA監管技術標準附件的表1和2詳細列出了該等需要上報至交易報告庫的項目。

在以下情形下,交易對手方和CCP必須進行上報:

* 達成合約時

* 修改合約時

* 終止合約時

上報時間必須不晚于合約達成、修改或終止後一個工作日。

17. 什麽産品需要上報以及誰負責上報:場外交易衍生品和交易所交易衍生品都需要上報。交易的對手方無論其分類如何,都有報告義務。請注意:

* 只有FC和NFC+需要進行估值和抵押品報告

* 每筆交易交易雙方都需要上報。

本信息僅用于指導使用盈透證券清算服務的客戶

注:以上信息不作爲全面窮盡式指南,也不是對法規的權威性解釋,而是對ESMA的EMIR法規和對應交易報告庫報告義務相關信息的總結。

Multi-Currency Trading at IBKR Central Europe

For Cash accounts (one without investment loan permissions), client can trade foreign products in all 10 supported currencies.

For example: Client with a cash account wants to buy a US stock. Our system will check if the client has sufficient available funds in USD or other supported currencies to cover 100% of the trade and, if so, the order will be sent to the exchange.

- If client has enough balance in USD, it will be used for execution of the order.

- If not, IBCE will automatically convert an equivalent amount of USD from other supported currencies with a positive balance.

- If the same client wishes to sell his USD denominated security at a later date, IBCE will NOT convert the proceeds back to one of the supported currencies.

- Client can use proceeds in USD for purchasing US stocks or withdraw them.

- Conversion to other currencies not connected to withdrawing funds is not allowed.

- Client can withdraw funds in Major Currencies, Home currency and positive balances held in the account. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBCE will automatically convert positive balances in the supported currencies to the requested one.

For Margin accounts (investment loan accounts), you can trade foreign products in supported currencies and have transactions that result in negative cash balances.

For example: Client with a margin account wants to buy an EU stock. Our system will check if the client has sufficient available funds in EUR or other supported currencies to meet initial margin requirements, and, if so, the order will be sent to the exchange.

- If client borrows EUR, he can decide what to do with the negative EUR balance. This negative balance can be closed by converting from any other supported currency or remain in the account.

- If the same client wishes to sell his EUR denominated security at a later date, IBCE will NOT convert the proceeds back to one of the supported currencies.

- Client can use proceeds in EUR for purchasing EU stocks or withdraw them.

- Conversion to other currencies not connected to withdrawing funds is not allowed.

- Client can withdraw funds in Major Currencies, Home currency and positive balances held in the account. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBCE will automatically convert positive balances in the supported currencies to the requested one.

For further information please see the IBCE Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note:

- IBCE does NOT charge clients for automatic currency conversion.

- Commissions for currency conversion used for closing a negative balance are presented on our website.

- Supported currency is a currency in which client can make deposits and hold a positive balance: EUR, USD, CHF, GBP, HUF, CZK, PLN, NOK, DKK and SEK.

- Major currencies: USD and EUR.

- Home currency: Currency of client’s country of legal residence.

For Cash accounts (one without investment loan permissions), you can trade foreign products in non-supported currencies. IBCE will auto convert the value of the transaction from the positive balance in supported currencies held in the account.

For example: Client with a cash account wants to buy a CAD stock. Our system will check if the client has sufficient available funds in the supported currencies to cover 100% of the trade and, if so, the order will be sent to the exchange.

On trade date, IBCE will automatically convert an equivalent amount of CAD from the positive balance in supported currencies held in the account, leaving no residual CAD cash balance in the account at the end of the day.

- If the same client wishes to sell his CAD denominated security at a later date, IBCE will auto convert the proceeds back to the base currency.

- The same process occurs when cash flows are generated from positions (e.g. dividends, interest). Conversion takes place when the cash is credited to or debited from the account, not when it is accrued.

For Margin accounts (one without investment loan permissions), you can trade foreign products in non-supported currencies and have transactions that result in negative cash balances. Proceeds and all positive balances in non-supported currencies will be automatically converted back to the base currency.

For example: Client with a margin account wants to buy a CAD stock. Our system is checking if the client has sufficient available funds in supported currencies to meet initial margin requirements and, if so, the order will be sent to the exchange.

- Client can decide what to do with the negative CAD balance. This negative balance can be closed by converting from any other supported currency or remain in the account.

- If the same client wishes to sell his CAD stock at a later date, IBCE will automatically convert the proceeds to the base currency as CAD is not a supported currency.

For further information please see the IBCE Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note:

- IBCE does NOT charge clients for automatic currency conversion.

- Commissions for currency conversion used for closing a negative balance are presented on our website.

- Supported currency is a currency in which client can make deposits and hold a positive balance: EUR, USD, CHF, GBP, HUF, CZK, PLN, NOK, DKK and SEK.

Currency conversion at IBCE must be connected to an investment service transaction (purchasing a stock, for instance) and its resulting cash flows. To comply with this regulation, clients can make a currency conversion in a trading platform only to close the negative balance from borrowing. In other cases, IBCE makes a conversion automatically.

- For Margin accounts, the client can open long positions that create cash debits (loans) in any currency. IBCE will not auto-convert your transaction but will create an investment loan in the currency of the trade. It will be the client’s discretion when to initiate a currency conversion to close the negative balance in part or in full.

- For Cash accounts, the client CANNOT open long positions that create cash debits (loans). Nevertheless, client can open long positions in any foreign product regardless of the currency in which it is denominated. IBCE will auto convert the value of the transaction from the positive balance in supported currencies held in the account.

- For both Margin and Cash accounts, any positive cash that is generated as the result of a trade or cash flows from a position you hold (e.g. dividends, coupon, interest) will NOT be auto-converted if it is the supported currency (EUR, USD, CHF, GBP, HUF, CZK, PLN, DKK, SEK and NOK).

- For both Margin and Cash accounts, any positive cash that is generated as the result of a trade or cash flows from a position you hold (e.g. dividends, coupon, interest) will be auto-converted if it is NOT the supported currency.

- For both Margin and Cash accounts, the client can withdraw funds in Major Currencies, Home currency and positive balances held in the account. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBCE will automatically convert positive balances in the supported currencies to the requested one.

- For both Margin and Cash accounts, the client can use the option “Withdraw All Available Cash”, which allows to withdraw all available funds in one currency: Major Currencies or Home currency. IBCE will automatically convert positive balances in the supported currencies to the requested one without leaving residuals.

For further information please see the IBCE Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note:

- IBCE does NOT charge clients for automatic currency conversion.

- Commissions for currency conversion used for closing a negative balance are presented on our website.

- Supported currency is a currency in which client can make deposits and hold a positive balance: EUR, USD, CHF, GBP, HUF, CZK, PLN, NOK, DKK and SEK.

- Major currencies: USD and EUR.

- Home currency: Currency of client’s country of legal residence.

- System shows the projected Cash Available for Withdrawal. The final withdrawal amount may differ from the requested due to fluctuation in currency exchange rates.

- Interactive Brokers Central Europe accounts are not allowed to withdraw funds on margin due to regulatory reasons.

- The same currency pairs can be traded as Forex CFD. Contracts For Difference are complex instruments, and we invite you to carefully review the CFDs risk warnings before trading these instruments.

IBCE clients can make deposits in all 10 Supported Currencies.

Withdrawals are allowed in Major currencies, Home currency and positive balances held in the account. If the client wants to withdraw funds, the system checks first if there is sufficient available funds in the requested or other supported currencies to cover 100% of the withdrawal amount. If there is no sufficient funds in the requested currency, IBCE will automatically convert positive balances in the supported currencies to the requested one.

Client can use the option “Withdraw All Available Cash”, which allows to withdraw all available funds in one currency: Major Currencies or Home currency. IBCE will automatically convert positive balances in the supported currencies to the requested one without leaving residuals.

For further information please see the IBCE Multi-Currency Account Foreign Exchange Restrictions Disclosure.

Please Note:

- IBCE does NOT charge clients for automatic currency conversion.

- Supported currency is a currency in which client can make deposits and hold a positive balance: EUR, USD, CHF, GBP, HUF, CZK, PLN, NOK, DKK and SEK.

- Major currencies: USD and EUR.

- Home currency: Currency of client’s country of legal residence.

- System shows the projected Cash Available for Withdrawal. The final withdrawal amount may differ from the requested due to fluctuation in currency exchange rates.

- Interactive Brokers Central Europe accounts are not allowed to withdraw funds on margin due to regulatory reasons.

- The changes mentioned above are effective since October 17, 2022.

有關俄羅斯盧布(RUB)的重要信息

跟許多金融機構一樣,IBKR已降低對俄羅斯盧布(RUB)的風險敞口,幷已停止俄羅斯盧布的所有資金服務,包括所有取款和貨幣兌換。

具體而言:

盧布存款:IBKR不再接受盧布存款。任何盧布存款均會被拒絕。

IBKR會根據您賬戶所屬IBKR實體定期將盧布餘額兌換成美元或歐元。

|

IBKR實體 |

目標貨幣 |

|

IBLLC |

USD |

|

IBCE |

EUR |

|

IBUK |

EUR |

|

IBIE |

EUR |

|

所有其它實體 |

USD |

盧布取款:IBKR現在無法支持盧布取款。

基礎貨幣:目前IBKR不允許客戶將盧布作爲基礎貨幣。 如果您賬戶的基礎貨幣是盧布,我們會根據您賬戶所在的IBKR實體將其更改爲美元或歐元(見上表)。

IBKR完全遵守所有適用的制裁法律。感謝您的理解與配合。

IMPORTANT NOTICE REGARDING THE RUSSIAN RUBLE (RUB)

In line with many financial institutions, IBKR has reduced exposure to the Russian Ruble, (“RUB”) and has discontinued all cashiering services for Russian Rubles, including all withdrawals and currency conversions.

Specifically:

Deposits in RUB: IBKR is no longer accepting deposits of RUB. Any deposit in RUB will be rejected.

IBKR will periodically convert RUB balances to USD or EUR, depending on the IBKR entity with which you have an account.

|

IBKR Entity |

Target Currency |

|

IBLLC |

USD |

|

IBCE |

EUR |

|

IBUK |

EUR |

|

IBIE |

EUR |

|

All Others |

USD |

Withdrawals in RUB: IBKR is not able to accommodate RUB withdrawals at this time.

Base Currency: IBKR does not currently allow clients to maintain RUB as their base currency. If you previously used RUB as your base currency, we converted it to USD or EUR depending on which IBKR entity your account is with (see chart above).

IBKR is fully committed to complying with all applicable sanctions laws. We appreciate your cooperation and your business.

如果我交易的產品是以我賬戶中沒有的幣種計價的會怎麼樣?

買賣給定的產品所需的特定幣種是交易所決定的,不是IBKR決定的。例如,當您下單買入某種以您的賬戶中沒有的幣種計價的證券,假設您使用的是保證金賬戶且在滿足了保證金要求後有多餘的資產,則IBKR會借入該幣種的資金。請注意,IBKR有義務以指定的計價幣種和清算所結算該交易。如您不希望我們借入資金進而產生利息成本,則您需先向您的賬戶存入所需的幣種及金額的資金,或通過IdealPro或各種零數(odd lot)交易場所將賬戶中的資金兌換為所需的幣種及金額——對於超過25,000美元或等值的金額,通過IdealPro兌換;對於小於25,000美元或等值的金額,通過零數交易場所兌換,這兩種渠道都可在TWS中找到。

需注意的還有,當您平倉了以特定幣種計價的證券,所獲資金將始終以該幣種保留在您的賬戶中,不論該幣種是否是您為賬戶選擇的基礎貨幣。相應地,這部分資金相對於您的基礎貨幣將存在匯率風險,直至您完成換匯或用這些資金交易其它以該幣種計價的產品。

Glossary terms:

關於使用止損單的更多信息

美股市場偶爾會發生極端波動和價格混亂。 有時這類情況持續時間很長,有時又很短。止損單可能會對價格施加下行壓力、加劇市場波動,且可能使委託單在大幅偏離觸發價格的位置上成交。.

投資者可能會在股價下跌時使用止損賣單鎖定盈利或限制損失。此外,在價格上漲時,持有空頭的投資者可能會使用止損買單來限制損失。然而,由於止損單一旦被觸發就會變為市價單,投資者將立即面臨和市價單一樣的風險——尤其是當市場波動很大時,委託單可能會在大幅高於或低於預期價格的位置上成交。

儘管止損單是一種能夠幫助投資者監控持倉價格的有用工具,但它也有潛在的風險。如您選擇使用止損單,請記住以下幾點:

· 止損價格不一定是執行價格。當“止損價格”被觸及,“止損單”就會成為“市價單”,而市價單會以當前的市場價格立即執行全部的交易量。. 因此,止損單最終被執行的價格可能和投資者設置的“止損價格”大相徑庭。相應地,在波動的市場環境下,客戶的止損單一旦變為市價單,就會立即成交。如果價格快速變動,執行價格可能會大幅偏離止損價格。

· 止損單可能會被短暫、劇烈的價格變動觸發。在市場波動巨大的時期,股票價格可能在極端的時間內大幅變動並觸發止損單被執行(之後又會恢復到之前的水平)。投資者應理解,如果止損單在這種情況下被觸發,則其委託單可能會以不理想的價格成交,且價格可能在同一個交易日內又企穩。

· 在極端波動的市場下,止損賣單可能會加劇價格的下跌。止損賣單的激活會給證券價格施加下行壓力。如果止損賣單在價格大幅向下跳空的情況下被觸發,則該委託單更有可能以大幅低於止損價格的價格成交。

· 為止損單附加“限價”有助於降低前述風險。當股價觸及或超過“止損價格”,帶有“限價”的止損單(“止損限價單”)會變為“限價單”。“限價單”是以不差於特定價格(即“限價”)的價格買賣證券的一種委託單。通過使用止損限價單而不是常規的止損單,客戶可提高委託單成交價格的確定性。. 然而,投資者也應注意,由於賣單不能以低於限價的價格成交(或者,買單不能以高於限價的價格成交),委託單最終可能無法成交。當客戶更看重以理想的目標價格成交而不是不管價格在什麼位置、都希望立即成交,這種情況下可考慮使用限價委託單。

· 在市場缺乏流動性或開盤和收盤等波動較大的時段,止損單的風險更大。. 這對缺乏流動性的股票尤為重要。此類股票在前述時段更難以當時的市價賣出,且在市場極端波動時,價格可能更離譜。客戶應考慮限制止損單可被觸發的時間段,以防止止損單在缺乏流動性的時段或開盤和收盤等波動率較大的時段被激活,也可考慮在這些時段使用其它委託單類型。

· 考慮到使用止損單的風險,客戶應謹慎考慮是否要使用符合其交易需求的其它委託單類型。

每日活動報表中的現金外匯轉換盈虧表示什麽?如何計算?

Overview:

為了對賬戶資產進行全面概覽、生成報表,賬戶中所有以非基礎貨幣計價的多頭或空頭現金餘額都將按現行匯率進行轉換。由於匯率隨時會變,這一轉換過程就可能導致現金外匯轉換餘額呈正(即盈利)或呈負(即虧損)。請注意,這些盈虧只是市場計算的一種標記(即假設所有非基礎貨餘額都以日末匯率平倉),實際的盈虧(如有)直到非基礎貨幣餘額平倉之後才能確定。

要計算非基礎貨幣的現金外匯轉換盈虧,首先要計算當前的基礎貨幣匯率和前一個每日報表週期基礎貨幣匯率之間的差額(匯率C – 匯率P,匯率可,參見每份報表的基礎貨幣匯率部分)。然後用這個差額(或正或負)乘以當前報表週期的期初現金餘額,所得結果就是現金外匯轉換盈利(如果是正數)或虧損(如果是負數)。由於所有其它非基礎貨幣項目(如淨賣出和買入、傭金、利息等)均在日末記帳,其本質上就沒有轉換盈虧。

IBKR Metals CFDs – Facts and Q&A

Overview:

The following article is intended to provide a general introduction to London Gold and Silver Contracts for Differences (CFDs) issued by IBKR.

Please follow these links for information on IBKR Share CFDs, Index CFDs and Forex CFDs.

Risk Warning

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage.

61% of retail investor accounts lose money when trading CFDs with IBKR.

You should consider whether you understand how CFDs work and whether you can afford to take the

high risk of losing your money.

ESMA Rules for CFDs (Retail Clients only)

The European Securities and Markets Authority (ESMA) has enacted new CFD rules effective 1st August

2018.

The rules include: 1) leverage limits on the opening of a CFD position; 2) a margin close out rule on a per

account basis; and 3) negative balance protection on a per account basis.

The ESMA Decision is only applicable to retail clients. Professional clients are unaffected.

Please refer to the following articles for more detail:

ESMA CFD Rules Implementation at IBKR (UK) and IBKR LLC

ESMA CFD Rules Implementation at IBIE and IBCE

Introduction

A London Gold CFD enables you to have exposure to price movements of physical Gold without actually owning it. A London Gold CFD is an agreement between you and IBKR to exchange the difference in price of the underlying over a period of time. The difference to be exchanged is determined by the change in the reference price of the underlying. Thus, if the price of physical Gold traded on the London bullion market rises and you are long the CFD, you receive cash from IBKR and vice versa. A London Gold CFD can be bought long or sold short to suit your view of market direction in the future.

Contract Specifications

| Contract | IBKR Symbol | Per Trade Fee | Minimum per Order | Multiplier |

| London Gold | XAUUSD | 0.015% | USD 2.00 | 1 |

| London Silver | XAGUSD | 0.03% | USD 2.00 | 1 |

Price Determination

The IBKR London Gold and Silver CFDs reference physical Gold and Silver traded on the London bullion market. The London bullion market is a wholesale over-the-counter market for the trading of precious metals. Trading is conducted among members of the London Bullion Market Association (LBMA). Most of the members are major international banks.

IBKR receives quote streams from approximately 10 such major banks, in much the same way it does for cash forex. IBKR Smart routes between the banks, and the best available price at any given time becomes the reference price for the CFDs. IBKR does not add a spread to the banks’ quotes.

Low Commissions and Financing Rates: Unlike other CFD providers IBKR charges a transparent

commission, rather than widening the spread. Commission rates are only 0.015% for London Gold and 0.03% for London Silver. Overnight financing rates are just benchmark +/- 1.5% (an additional 1% surcharge is added for retail accounts).

Transparent Quotes: Because IBKR does not widen the spread, the Metals CFD quotes accurately

represent the spreads and price movements of the related cash metal, as described above.

Margin Efficiency: IBKR establishes house-margin requirements based on historic volatility of the

underlying and other factors. Retail clients are subject to regulatory minimum initial margins of 5% for

London Gold or 10% for London Silver.

Trading Permissions: Same as for Share and Index CFDs.

Market Data Permissions: Metals CFD market data is free, but a permission is required for system

reasons.

Worked Trade Example (Professional Clients):

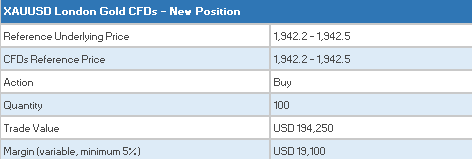

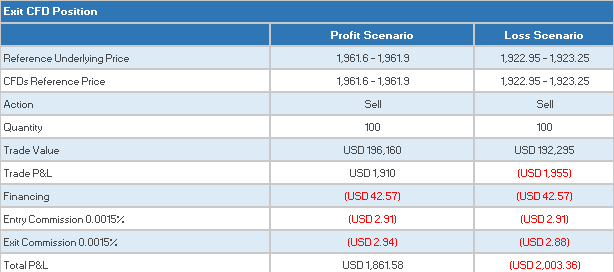

You purchase 100 XAUUSD CFDs at $1,942.5 for USD 194,250 which you then hold for 5 days.

![]()

Closing the Position

CFD Resources

Below are some useful links with more detailed information on IB’s CFD offering:

Frequently asked Questions

Are short Metals CFDs subject to forced buy-in?

No.

Can I take delivery of the underlying metal?

No, IBKR does not support physical delivery for Metals CFDs.

Are there any market data requirements?

The market data for Metal CFDs is free, and is included the market data for Index CFDs. However, you need to subscribe to the permission for system reasons. To do this, log into Account Management, and click through the following tabs: Settings/User Settings/Trading Platform/Market Data Subscriptions. Alternatively you can set up an Index or Metals CFD in your TWS quote monitor and click the “Market Data Subscription Manager” button that appears on the quote line.

How are my CFD trades and positions reflected in my statements?

If you are a client of IBKR (U.K.) or IBKR LLC, your CFD positions are held in a separate account segment identified by your primary account number with the suffix “F”. You can choose to view Activity Statements for the F-segment either separately or consolidated with your main account. You can make the choice in the statement window in Account Management.

If you are a client of other IBKR entities, there is no separate segment. You can view your positions normally alongside your non-CFD positions.

In what type of IB accounts can I trade CFDs e.g., Individual, Friends and Family,

Institutional, etc.?

All margin and cash accounts are eligible for CFD trading.

Can I trade CFDs over the phone?

No. In exceptional cases we may agree to process closing orders over the phone, but never opening

orders.

Can anyone trade IB CFDs?

All clients can trade IB CFDs, except residents of the USA, Canada, Hong Kong, New Zealand and

Israel. There are no exemptions based on investor type to the residency-based exclusions.

外匯(FX)入門

Overview:

IB提供的交易場所和交易平臺既適用於專注外匯交易的交易者也適用於因多幣種股票和/或衍生品交易需要偶爾進行外匯交易的交易者。下方文章概述了在TWS平臺上下達外匯定單的基本要點以及報價管理和頭寸報告相關信息。

Background:

外匯(FX)交易涉及同時買入一種貨幣並賣出另一種貨幣,兩種貨幣組合在一起通常被稱為交叉貨幣對。在下方例子中,EUR.USD交叉貨幣對中的前一種貨幣(EUR)為交易者想買入或賣出的交易貨幣,後一種貨幣(USD)則為結算貨幣。

跳轉至指定主題;

外匯報價

貨幣對即外匯市場上一種貨幣單位相對於另一種貨幣單位的相對價值的報價。用以作為參考的貨幣被稱為報價貨幣,而參考該貨幣給出報價的貨幣則被稱為基礎貨幣。在TWS中,每個貨幣對有一個交易代碼。您可以使用外匯交易者(FXTrader)調換報價方向。交易者買入或賣出基礎貨幣的同時在賣出或買入報價貨幣。例如,EUR/USD貨幣對的代碼為:

EUR.USD

其中:

- EUR為基礎貨幣

- USD為報價貨幣

上方貨幣對的價格表示需要多少單位的USD(報價貨幣)能交易一個單位的EUR(基礎貨幣)。也就是說,1 EUR是在按USD報價。

EUR.USD的買單表示買入EUR並賣出同等金額的USD,具體取決於交易價格。

創建報價行

在TWS添加外匯報價行具體步驟如下:

1. 輸入交易貨幣(如EUR),然後按回車鍵(enter)。

2. 選擇產品類型——外匯

3. 選擇結算貨幣(如USD),然後選擇外匯交易場所。

.jpg)

注:

IDEALFX對於超過其最低數量要求(通常為25,000美元)的定單可直接接入銀行間外匯報價。傳遞到IDEALFX但未達到其最低數量要求的定單基本會被自動傳遞到小額定單交易場所進行外匯轉換。點擊此處瞭解IDEALFX的最低數量要求和最高數量限制相關信息。

外匯交易商會按特定方向對外匯貨幣對進行報價。因此,交易者需通過調整輸入的貨幣代碼來查找想要的貨幣對。例如,如果輸入貨幣代碼CAD,交易者會發現合約選擇窗口中沒有結算貨幣USD。這是因為,該貨幣對是按USD.CAD報價的,只能先輸入底層代碼USD,然後再選擇貨幣對。

下單

具體取決於顯示的欄標頭,貨幣對將顯示如下:

合約(Contract)和描述(Description)欄將按交易貨幣.結算貨幣的形式顯示貨幣對(如EUR.USD)。底層代碼(Underlying)欄則只顯示交易貨幣。

點擊此處瞭解如何更改更改顯示的數據欄標頭。

1. 要輸入定單,左鍵點擊買價(下賣單)或賣價(下買單).

2. 指定想要買入或賣出的交易貨幣的數量。定單的數量按基礎貨幣(即貨幣對中的前一種貨幣)顯示。

盈透證券在外匯交易上沒有代表固定金額基礎貨幣的合約的概念,您的交易尺寸便是所需交易的基礎貨幣金額。

例如,100,000單位EUR.USD的買單會買入100,000單位EUR,並根據顯示的匯率賣出等值USD。

3. 指定想使用的定單類型、匯率(價格),然後傳遞定單。

注:下達的定單必須是完整的貨幣單位,除上述交易場所最低數量要求外,沒有最低合約或手數要求。

點值

點(pip)是貨幣對變化的衡量單位,對於大多數貨幣對來說其代表最小變化,但有時也允許存在非整點的變化。

例如,在EUR.USD中,1個點是0.0001,而在USD.JPY中,1個點事0.01。

要計算報價貨幣1個點的點值,可採用以下公式:

(名義金額) x (1個點)

例如:

- 代碼 = EUR.USD

- 金額 = 100,000 EUR

- 1個點 = 0.0001

1個點點值 = 100’000 x 0.0001= 10 USD

- 代碼 = USD.JPY

- 金額 = 100’000 USD

- 1個點 = 0.01

1個點點值 = 100’000 x (0.01)= JPY 1000

要計算基礎貨幣1個點的點值,可採用以下公式:

(名義金額) x (1個點/匯率)

例如:

- 代碼 = EUR.USD

- 金額 = 100’000 EUR

- 1個點 = 0.0001

- 匯率 = 1.3884

1個點點值 = 100’000 x (0.0001/1.3884)= 7.20 EUR

- 代碼 = USD.JPY

- 金額 = 100’000 USD

- 1個點 = 0.01

- 匯率 = 101.63

1個點點值 = 100’000 x (0.01/101.63)= 9.84 USD

頭寸(交易後)報告

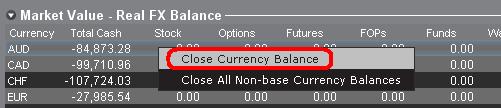

外匯頭寸信息是在IB進行交易的一個重要方面,在真實賬戶中開始交易之前需對其進行充分瞭解。IB的交易軟件在兩個不同的地方反映了外匯頭寸,二者均可在賬戶窗口查看。

1. 市場價值

賬戶窗口的市場價值部分反映的是實時貨幣頭寸,按貨幣(而非貨幣對)顯示。

賬戶窗口的市場價值部分是唯一一個可供交易者查看實時外匯頭寸信息的地方。持有多種貨幣頭寸的交易者不一定要使用開倉時用的貨幣對來平倉。例如,買了EUR.USD(買EUR賣USD)還買了USD.JPY(買USD賣JPY)的交易者也可以通過交易EUR.JPY(賣EUR買JPY)來平倉頭寸。

注:

市場價值部分可展開/收起。交易者應點擊淨清算價值欄上方的符號確保顯示出綠色“減號”。如果是綠色“加號“,某些頭寸可能被隱藏。

交易者可以從市場價值部分發起平倉交易:右鍵點擊想要平倉的貨幣,選擇”平倉貨幣餘額“或”平倉所有非基礎貨幣餘額“。

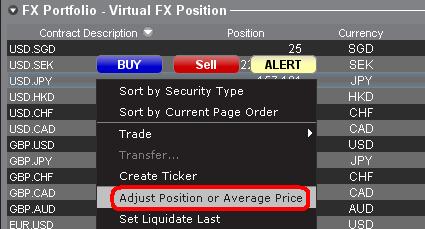

2. 外匯投資組合

賬戶窗口的外匯投資組合部分展示的是虛擬頭寸,以貨幣對的形式顯示頭寸信息,這與市場價值部分按貨幣顯示不同。這種特定的顯示形式是為了考慮機構外匯交易者的常用慣例,零售或非頻繁外匯交易者基本上可以無視該部分信息。外匯投資組合的頭寸數量並不反映所有外匯活動,但是,交易者可以對此部分顯示的頭寸數量和平均成本進行修改。這一無需執行交易便可隨意調整頭寸和平均成本信息的功能對於除交易非基礎貨幣產品外還參與其它貨幣交易的交易者可能會有幫助。其可讓交易者手動將自動貨幣轉換(交易非基礎貨幣產品時會自動發生)與單純的外匯交易活動分隔開來。

外匯投資組合部分的外匯頭寸和盈虧信息均來自所有其它交易窗口顯示的信息。這在確定真實的實時頭寸信息時可能會造成一定困惑。為減少或消除此類困惑,交易者可以選擇以下操作:

a. 收起外匯投資組合部分

點擊外匯投資組合(FX Portfolio)文字左邊的箭頭可收起外匯投資組合部分。收起該部分後,虛擬頭寸信息便不再在各交易頁面顯示。(注:這並不會讓市場價值信息顯示出來,其只會阻止外匯投資組合信息顯示。)

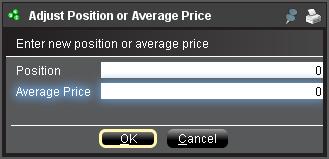

b. 調整頭寸或平均價格

右鍵點擊賬戶窗口的外匯投資組合部分,交易者可以選擇調整頭寸或平均價格。交易者平倉掉所有非基礎貨幣頭寸並確定市場價值部分反映了被平倉的所有非基礎貨幣頭寸後,便可將頭寸和平均價格區域重置為0。此操作會重置外匯投資組合部分的頭寸數量,可讓交易者在交易界面看到更加準確的頭寸和盈虧信息。(注:這是手動操作,每次貨幣頭寸平倉後都需進行一次)。交易者應隨時對市場價值部分的頭寸信息進行確認,確保傳遞的定單達到開倉或平倉頭寸想要的結果)

我們鼓勵交易者在真實賬戶中開始交易前,先在模擬交易或演示賬戶中熟悉一下外匯交易。如關於以上信息仍有任何疑問,請聯繫IB。

其它常見問題: