Chicago Personal Property Tax

Chicago has a personal property tax which applies to a non-possessory computer lease by a Chicago resident. The Chicago tax authorities have ruled that tax is to be applied in cases where a customer pays for electronic research/use of an interactive site. The passive receipt or streaming of information is not subject to the tax.

Clients whose permanent residential address or principal business address is Chicago will have this tax passed through to their accounts.

The tax rate, as of October 2017, is 9%. The tax will be charged on the research and news feeds a client is subscribed to. Should a research and news feed be eligible to a waiver based upon commissions generated, the tax will not be applied.

As of October 2017, research and news subscriptions which would be subject to the tax would include

Base IBIS Research Platform and the IBIS Research Essentials Subscription Bundle

Cusip

Dow Jones News Service

Dow Jones Real Time News

US Press Release Feed

Reuters Global Newswire

Reuters StreetEvents Calendars

Reuters Fundamentals

Reuters Basic Newfeed

Morningstar Equity, ETF and Credit Reports

Wall Street Horizons

Zacks Equity Research Reports

The above list is provided on a best efforts basis and is subject to change. Clients will be responsible for any pass through tax regardless of any discrepancy from the list provided above.

Ritenuta alla fonte sui pagamenti equivalenti ai dividendi - Domande frequenti

Premessa

A partire dal 1 gennaio 2017 i nuovi regolamenti dell'IRS imporranno ritenute alla fonte statunitensi sui pagamenti equivalenti ai dividendi statunitensi in favore di soggetti non statunitensi detentori di posizioni in derivati su titoli statunitensi. In precedenza, le ritenute alla fonte statunitensi non erano imposte su tali pagamenti. I suddetti regolamenti richiedono agli intermediari, noi compresi, di agire in veste di sostituti d'imposta e riscuotere la ritenuta statunitense a nome dell'IRS. Di seguito è illustrata una panoramica della ritenuta, delle modalità in cui viene stabilita e dei prodotti ai quali si applica tale regolamento.

Panoramica

Qual è la finalità del regolamento?

Il regolamento trova origine nella Sezione 871(m) dell'Internal Revenue Code ("Codice Tributario Statunitense") ed è inteso ad armonizzare il trattamento fiscale statunitense imposto ai soggetti non statunitensi in relazione ai dividendi sui titoli statunitensi e ai pagamenti equivalenti ai dividendi corrisposti sui contratti derivati che replicano (in misura elevata) la proprietà di tale titolo.

Per esempio, si consideri un contratto total return swap avente IBM come sottostante. Un soggetto non statunitense in possesso di una posizione sul titolo IBM sarebbe soggetto a una ritenuta alla fonte statunitense del 30% (ridotta dalla convenzione fiscale) sul versamento del dividendo. Al contrario, prima dell'applicazione della Sezione 871(m), un soggetto non statunitense con un'esposizione lunga a IBM sul contratto swap avrebbe potuto percepire pagamenti equivalenti ai dividendi senza l'imposizione della ritenuta alla fonte statunitense. Era proprio così, nonostante i pagamenti replicassero una simile esposizione economica. Ora, invece, ai sensi della Sezione 871(m) tali "pagamenti equivalenti ai dividendi" sono soggetti alla ritenuta alla fonte statunitense.

Cosa si intende per "pagamento equivalente al dividendo"?

Per pagamento equivalente al dividendo si intende un importo lordo riconducibile al versamento di un dividendo su un titolo azionario statunitense e usato per calcolare ciascun importo netto trasferito alla o dalla parte long, anche qualora la parte long effettui un pagamento in favore della parte short o il pagamento netto sia pari a zero. Di conseguenza, tale pagamento includerebbe non solamente il versamento effettivo in sostituzione del dividendo, bensì anche la stima del pagamento del dividendo implicitamente tenuto in considerazione nel calcolo di uno o più termini della transazione, compresi il tasso di interesse, l'importo nozionale o il prezzo di acquisto.

Si consideri, per esempio, un'opzione call quotata su un titolo azionario statunitense: il titolare della call non ha diritto a percepire dividendi a meno che l'opzione non sia esercitata prima della data di stacco cedola. Ciononostante, il premio corrisposto dal titolare per l'acquisto dell'opzione tiene implicitamente conto del valore presente del dividendo atteso nel corso della durata dell'opzione.[1] Dato che questo fattore serve a ridurre il pagamento dovuto dall'acquirente dell'opzione al venditore, è considerato un pagamento equivalente al dividendo potenzialmente soggetto alle suddette normative.

Chi è soggetto alla ritenuta alla fonte sui pagamenti equivalenti ai dividendi?

La ritenuta si applica alle posizioni che soddisfino i requisiti previsti e siano detenute in conti di contribuenti non statunitensi. Al contrario, non si applica ai contribuenti statunitensi. I conti appartenenti ai contribuenti non statunitensi, in genere, sono documentati tramite l'invio del modulo IRA W-8 e possono comprendere le seguenti tipologie: individuali, cointestati, fiduciari e conti per organizzazioni.

Quali sono gli strumenti derivati potenzialmente soggetti alla ritenuta alla fonte sui pagamenti equivalenti ai dividendi?

I regolamenti vigenti adottano un test in due passaggi per stabilire se gli strumenti derivati sono soggetti o meno a tali normative. Innanzitutto, tali strumenti derivati devono essere riconducibili al dividendo su un titolo azionario statunitense. Per esempio:

- opzioni su azioni

- SSF (future su singole azioni) regolati

- future su indici e opzioni su future su indici regolati

- titoli strutturati ed ETN (exchange traded notes)

- contratti per differenza

- obbligazioni convertibili

- operazioni per il prestito di titoli

- derivati su panieri personalizzati e

- warrant

Il presupposto è che la posizione sottostante sia un titolo azionario statunitense. La Borsa sulla quale lo strumento è negoziato e l'identità della controparte non incidono sull'applicazione di tali normative. In altre parole, un derivato può essere soggetto alle normative sia che si tratti di uno strumento quotato in Borsa, fuori Borsa, negoziato negli Stati Uniti o all'estero.

In secondo luogo, lo strumento derivato deve replicare in modo sostanziale le condizioni economiche del titolo statunitense sottostante al momento della sua emissione. Per effettuare tale decisione, le normative considerano il delta (per i contratti semplici) e il test di equivalenza sostanziale (per i contratti complessi).

Il delta è una misura di correlazione che calcola il rapporto tra la variazione del valore equo di mercato dello strumento derivato e la variazione del valore equo di mercato del titolo azionario statunitense al quale il derivato fa riferimento. In generale, ai fini di tale regolamento, il delta è stabilito una volta sola nel corso della durata dello strumento derivato, ovvero, al momento della sua "emissione", e non viene ricalcolato al variare del valore equo di mercato del titolo sottostante o una volta rivenduto lo strumento derivato nel mercato secondario.

Le seguenti normative si applicano alla maggior parte dei contratti:

· Prima del 2017: gli strumenti derivati emessi prima del 1 gennaio 2017 (es. qualsiasi strumento che il cliente detenga presso di noi al 31 dicembre 2016) non sono soggetti alle nuove normative in materia di ritenute di imposta.

· 2017: gli strumenti derivati emessi nel 2017 sono potenzialmente soggetti al nuovo regime di imposizione alla fonte se, al momento dell'emissione, hanno un delta di 1.0.

· Dopo il 2017: gli strumenti derivati emessi dopo il 31 dicembre 2017 sono potenzialmente soggetti alle nuove normative in materia di imposizione alla fonte se, al momento della loro emissione, hanno un delta di 0.8 o superiore.

Il test del delta non è applicabile agli strumenti derivati classificati come "complessi". Al contrario, in questo caso, si ricorre al test di equivalenza sostanziale.

Quindi, quando avviene l'emissione di uno strumento derivato?

L'identificazione della data di emissione di uno strumento derivato è di grande importanza. Stabilisce se lo strumento è soggetto o meno alle normative (gli strumenti emessi prima del 2017 non lo sono) e la data in cui viene effettuato il calcolo del delta. In generale, la data di "emissione" di un strumento corrisponde al momento nel quale esso viene creato, ovvero alla sua data di inizio o rilascio iniziale. Per "emissione" dello strumento non si intende il momento in cui esso è rivenduto nel mercato secondario

Di conseguenza, vi sono differenze tra le varie norme di emissione relative a opzioni, future, prodotti negoziati su altre Borse e prodotti scambiati fuori Borsa. Per esempio, l'emissione di un'opzione quotata e scambiata su una Borsa statunitense, in genere, non avviene la prima volta in cui questa è quotata su una Borsa come disponile per il trading. Al contrario, l'emissione dell'opzione quotata avviene (ovvero, il suo delta è stabilito) quando l'opzione è aperta dal cliente. Peraltro, nel caso dei derivati trasferibili come, per esempio, ETN (exchange traded note), obbligazioni e warrant convertibili, la relativa emissione corrisponderebbe esclusivamente al momento della loro prima vendita. Il delta stabilito in tale momento proseguirebbe anche dopo la vendita al successivo acquirente.

Sono previste eccezioni?

Le norme prevedono poche eccezioni alla ritenuta; eccone alcuni esempi:

• strumenti derivati che riflettono un "indice qualificato" - in genere, un ampio indice passivo pubblicamente disponibile su titoli azionari statunitensi come S&P 500, NASDAQ 100 o Russell 2000.

• strumenti derivati che riflettono un indice con scarsa o nessuna composizione azionaria statunitense, per esempio l'indice Hang Seng.

• il pagamento equivalente al dividendo (o una sua parte) non è soggetto alla ritenuta alla fonte statunitense se il soggetto non statunitense possiede direttamente il titolo sottostante. Ciò si verifica solitamente con gli strumenti derivati su fondi comuni statunitensi, fondi immobiliari REIT (Real Estate Investment Trust) e fondi negoziati in Borsa eroganti "dividendi" ricaratterizzati come distribuzioni di plusvalenze di capitale o rendimento del capitale.

Sono disponibili esempi di casi in cui tali normative trovano o meno applicazione?

• Il 2 gennaio 2017 un cliente acquista un SSF sul titolo IBM e il future ha un delta di 1.0: il contratto future è soggetto alla normativa.

• Il 28 dicembre 2016 il cliente acquista un'opzione CCC quotata profondamente in the money sul titolo IBM e il future ha un delta di 1.0. In questo caso, l'opzione non è soggetta alla normativa, in quanto emessa prima del 2017.

• Il 15 gennaio 2017 il cliente acquista un future su indice a base ristretta. Si ipotizzi che l'indice non sia un "indice qualificato". Il tal caso, il future sarebbe soggetto alla normativa.

• Il 2 gennaio 2017 il cliente acquista un ETN con un delta di 1.0 che riproduce titoli azionari statunitensi e il titolo è stato emesso il 1 luglio 2016: l'opzione non è soggetta alla normativa, in quanto emessa prima del 2017

Come viene calcolata l'imposizione sul pagamento equivalente al dividendo?

Se lo strumento derivato è soggetto al nuovo regolamento della Sezione 871(m), il pagamento equivalente al dividendo di tale strumento sarà pari al dividendo per azione sul titolo azionario statunitense sottostante, moltiplicato per il numero di azioni sottostanti alle quali lo strumento fa riferimento, moltiplicato per il delta (es. un contratto di opzioni con consegna di 100 azioni di un titolo erogante un dividendo di 1.00 dollari e avente un delta di .80 sarebbe soggetto a un'imposta sulla base del pagamento equivalente al dividendo di 80.00 dollari).

In caso di contratti derivati complessi, l'equivalente del dividendo sarebbe pari al dividendo per azione sul sottostante, moltiplicato per la copertura del contratto equivalente al sottostante - secondo il calcolo effettuato al momento dell'emissione del contratto.

Come viene effettuata la combinazione dei contratti per la determinazione del delta?

A partire dal 2018 i clienti che procedano all'acquisto di uno strumento derivato, come, per esempio, un'opzione call long con un delta inferiore alla soglia di .80, e vendano un'opzione put sullo stesso sottostante e con la stessa quantità di azioni entro 2 giorni l'una dall'altra, si vedranno combinare tali posizioni al fine di stabilire se è stata oltrepassata la soglia prevista (es. l'acquisto di una call long con un delta di 0.60 accoppiata con la vendita di una put con un delta di .40 porterebbe a un delta long di 1.0).

Nel 2017 solamente gli strumenti negoziati fuori Borsa sono potenzialmente soggetti alla combinazione per creare uno strumento con delta 1.0.

Quali sono le misure previste per informare i clienti in merito alle posizioni coinvolte da tale regolamento?

Per ridurre al minimo l'esposizione alla ritenuta alla fonte, forniremo un messaggio di avvertimento in TWS nel momento in cui i soggetti non statunitensi creino ordini che possano generare tale imposta. Tale avviso consentirebbe ai clienti di annullare l'ordine per evitare la ritenuta, oppure inviare l'ordine ed eventualmente pagare la ritenuta al momento del versamento del dividendo. I clienti possono evitare il pagamento della ritenuta alla fonte nel caso in cui non siano in possesso del derivato alla data della ritenuta (ovvero, in genere, alla data di registrazione del dividendo).

ATTENZIONE: non forniamo alcun tipo di consulenza fiscale, legale o finanziaria. Consigliamo vivamente a tutti i clienti di consultare il proprio consulente per stabilire l'impatto dei regolamenti della Sezione 871(m) sulla propria attività di trading.

[1] Mentre il titolare di un'opzione call non percepisce alcun dividendo, il premio corrisposto dal titolare per l'opzione tiene implicitamente conto dei dividendi attesi (in quanto, secondo le previsioni, il prezzo del titolo dovrebbe diminuire dell'importo del dividendo alla data di stacco cedola; i dividendi in contanti implicano premi call minori).

How to update the US Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) on your account

Background:

If you have been informed or believe that your account profile contains an incorrect US SSN/ITIN, you may simply log into your Account Management to update this information. Depending on your taxpayer status, you can update your US SSN/ITIN by modifying one of the following documents:

1) IRS Form W9 (if you are a US tax resident and/or US citizen holding a US SSN/ITIN)

2) IRS Form W-8BEN (if you are a Non-US tax resident holding a US SSN/ITIN)

Please note, if your SSN/ITIN has already been verified with the IRS you will be unable to update the information. If however the IRS has not yet verified the ID, you will have the ability to update through Account Management.

How to Modify Your W9/W8

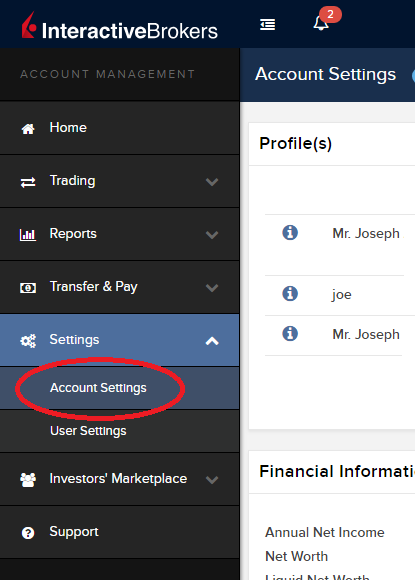

1) To submit this information change request, first login to Account Management

2) Click on the Settings section followed by Account Settings

3) Find the Profile(s) section. Locate the User you wish to update and click on the Info button (the "i" icon) to the left of the User's name

.png)

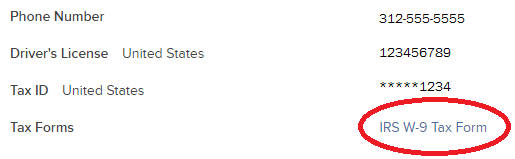

4) Scroll down to the bottom where you will see the words Tax Forms. Next to it will be a link with the current tax form we have for the account. Click on this tax form to open it

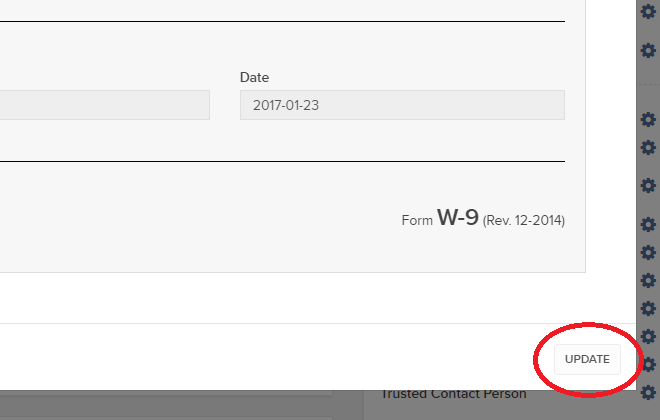

5) Review the form. If your US SSN/ITIN is incorrect, click on the UPDATE button at the bottom of the page

6) Make the requisite changes and click the CONTINUE button to submit your request.

7) If supporting documentation is required to approve your information change request, you will receive a message. Otherwise, your information change request should be approved within 24-48 hours.

Withholding Tax on Dividend Equivalent Payments - FAQs

Background

Beginning January 1, 2017, new IRS regulations will impose U.S. withholding taxes on US dividend equivalent payments to non-US persons holding derivative positions on US equities. Previously, US withholding tax was not imposed on these payments. The regulations require intermediaries, such as us, to act as withholding agents and collect US tax on behalf of the IRS. An overview of the tax, how it’s determined and the products impacted is provided below.

Overview

What is the purpose of the regulation?

The regulation derives from Section 871(m) of the Internal Revenue Code and is intended to harmonize the US tax treatment imposed on non-U.S. persons with respect to dividends on U.S. stock and dividend equivalent payments paid on derivative contracts that replicate (to a high degree) ownership of such stock.

An example of this would be a total return swap having IBM as its underlying. A non-U.S. person holding an IBM stock position would be subject to a 30% US withholding tax (reduced by treaty) on dividend payments. On the other hand prior to the implementation of Section 871(m), a non-U.S. person holding long exposure to IBM on the swap could receive payments equivalent to the dividends without imposition of U.S. withholding tax. This was the case even though the payments replicated similar economic exposure. Section 871(m) now considers those ‘dividend equivalent payments’ subject to US withholding tax.

What is a dividend equivalent payment?

A dividend equivalent payment is any gross amount that references the payment of a dividend on a U.S. equity and that is used to compute any net amount transferred to or from the long party, even if the long party make a net payment to the short party or the net payment is zero. Accordingly, such payments would include not only an actual payment in lieu of a dividend but also an estimated dividend payment that is implicitly taken into account in computing one or more of the terms of the transaction, including interest rate, notional amount or purchase price.

In the case of a listed call option on a U.S. stock, for example, the holder of the call is not entitled to receive a dividend unless the option is exercised prior to the dividend ex-date. Nonetheless, the premium paid by the holder to purchase the option implicitly takes into account the present value of the expected dividends over the option term.[1] Since this factor serves to lower the payment from the option buyer to the seller, it is viewed as a dividend equivalent payment potentially subject to the rules.

Who is subject to the dividend equivalent withholding tax?

The tax applies to qualifying positions held in an account of a non-U.S. taxpayer. It does not apply to U.S. taxpayers. Accounts of non-U.S. taxpayers generally are evidenced by the submission of an IRS Form W-8 and can include the following account types: individual, joint, organization and trust.

What derivative instruments potentially are subject to the dividend equivalent withholding tax?

The regulations adopt a two-part test to determine if a derivative instrument is subject to the rules. First, the derivative instruments must reference the dividend on a U.S. equity security. Examples include:

- equity options

- regulated single stock futures

- regulated index futures and options on index futures

- structured and exchange traded notes

- CFD contracts

- convertible bonds

- securities lending transactions

- derivatives on custom baskets and

- warrants

If the underlying position is a U.S. equity. The exchange upon which the instrument is traded and the identity of the counterparty do not affect the application of the rules. That is, a derivative can be subject to the rules, whether it is exchange listed or over the counter or trades in the United States or overseas.

Second, the derivative instrument must substantially replicate the economics of the underlying U.S. equity at the time of issuance. The rules look to delta (for simple contracts) and a substantially equivalency test (for complex contracts) to make this determination.

Delta is a correlation measurement that computes the ratio of the change in the fair market value of the derivative instrument to a change in the fair market value of the U.S. equity referenced by the derivative. In general, for purposes of this regulation, delta is only determined once over the life of the derivative instrument – at the time it is ‘issued’. It is not recomputed as the fair market value of the underlying security changes or when the derivative instrument is re-sold in the secondary market.

For most contracts, the rules are as follows:

· Pre-2017 – a derivative instrument issued prior to January 1, 2017 (i.e., anything held by a customer with us on December 31, 2016) is not subject to the new withholding tax rules.

· 2017 - a derivative instrument issued in 2017 is potentially subject to the new withholding tax regime if the delta at the time of issuance is 1.0.

· After 2017 – a derivative instrument issued after December 31, 2017 is potentially subject to the new withholding tax rules if the delta at the time of issuance is 0.8 or greater.

If the derivative is classified as “complex,” the delta test does not apply and instead the substantial equivalency test applies.

So When Is a Derivative Instrument Issued?

Identified when a derivative instrument is issued is very important. It determines if the instrument is subject to the rules (pre-2017 issued instruments are not) and when the delta computation is made. In general, an instrument is ‘issued’ when it comes into existence, its inception date or date of original issuance. Instruments are not issued when re-sold in the secondary market.

As a result, there are differences in the issuance rules for listed options, futures, other exchange traded products and over-the-counter products. For example, a listed option traded on a US exchange, generally, is not issued when first listed by an exchange as available for trading. Instead, the listed option is issued (delta determined) when the option is entered into by the customer. On the other hand, for transferable derivatives, such as exchange traded notes, convertible bonds and warrants, they would be issued only when first sold. The delta determined at that time would carryover when sold to a subsequent purchaser.

Are There Any Exceptions?

The rules do provide limited exceptions to withholding. These include:

• a derivative instrument that references a “qualified index” - generally, a passive broad publicly available index on U.S. equities such as the S&P 500, NASDAQ 100 or Russell 2000.

• a derivative instrument that references an index with little or no U.S. equity composition – such as the Hang Seng Index.

• if the dividend equivalent payment (or portion thereof) would not be subject to U.S. withholding tax if the non-US person owned the underlying security directly. This most often will occur for derivative instruments on U.S. mutual funds, REITs and exchange traded funds that pay ‘dividends’ which are re-characterized as capital gain distributions or returns of capital.

Can you provide some examples of when the rules will or will not apply?

• Customer purchases single stock futures on IBM on January 2, 2017. The delta of the future is 1.0. The future is subject to the rule.

• Customer purchases a deep in the money OCC listed option on IBM on December 28, 2016. The delta of the future is 1.0. The option is not subject to the rule as it was issued prior to 2017.

• Customer purchases index future on a narrow based index on January 15, 2017. Assume the index is not a ‘qualified index.’ The future is subject to the rule.

• Customer purchases an exchange trade note that tracks U.S. equities on January 2, 2017 with a delta of 1.0. The note was issued on July 1, 2016. The option is not subject to the rule as it was issued prior to 2017

How is the dividend equivalent withholding computed?

If the derivative instrument is subject to the new Section 871(m), a dividend equivalent payment with respect to such instrument equals the per share dividend on the underlying U.S. equity, multiplied by the number of underlying shares referenced by the instrument, multiplied by the delta (e.g., an option contract delivering 100 shares of a stock paying $1.00 dividend and having a delta of .80 would be subject to a tax based upon $80.00 dividend equivalent payment).

In the case of a complex derivative contract, the dividend equivalent will be equal to the per share dividend on the underlying, multiplied by the contract’s hedge equivalent to the underlying as calculated when the contract was issued.

How are contracts combined for purposes of determining delta?

Starting in 2018, customers who purchase derivative instrument such as a long call having a delta below the .80 threshold and selling a put on the same underlying and same share quantity within 2 days of one another will have those positions combined for the purpose of determining whether the threshold has been exceeded (e.g., the purchase of a long call with a delta of 0.60 coupled with the sale of a put with a delta of .40 would result in a long delta of 1.0).

In 2017, only over-the-counter instruments are potentially subject to combination to create a delta 1.0 instrument.

What information do we provide to inform clients about impacted positions?

To minimize exposure to the withholding tax, we intend to provide a TWS warning message will be provided when non-U.S. persons create an order that could generate the tax. This will give customers the option of canceling the order to avoid potential withholding or submitting the order and possibly paying the tax when a dividend occurs. Customers may avoid the potential withholding tax by not owning the derivative on the applicable withholding date (i.e., generally the dividend Record Date).

IMPORTANT NOTE: We do not provide tax, legal or financial advice. Each customer must speak with the customer’s own advisors to determine the impact that the Section 871(m) rules may have on the customer’s trading activity.

[1] While the holder of the call option does not receive a dividend, the premium paid by the holder for the option implicitly takes expected dividends into account (i.e., because the stock price is expected to drop by the amount of the dividend on the ex-dividend date, cash dividends imply lower call premiums).

Common Reporting Standard (CRS)

The Common Reporting Standard (CRS), referred to as the Standard for Automatic Exchange of Financial Account Information (AEOI), calls on countries to obtain information from their financial institutions and exchange that information with other countries automatically on an annual basis. The CRS sets out the financial account information to be exchanged, the financial institutions required to report, the different types of accounts and taxpayers covered, as well as common due diligence procedures to be followed by financial institutions. For more information about CRS, please visit the OECD website.

Interactive Brokers entities comply with the requirements of CRS as implemented in the jurisdictions where they are located, and report account information to the applicable government authorities. Clients reported by Interactive Brokers under CRS will receive a CRS Client Report in the Client Portal shortly after the reporting deadlines specified below. The CRS Client Report provides an overview of the information that was reported by Interactive Brokers.

- What information is reported under CRS:

- Account number

- Name

- Address

- Tax ID Number

- Tax residency country

- Date of birth

- Year-end account balance

- Gross proceeds (all sales)

- Interest income

- Dividend income

- Other income

- When and where is the information reported:

- Interactive Brokers Australia Pty. Ltd. reports to the Australian Taxation Office (ATO) by July 31.

- Interactive Brokers Canada Inc. reports to the Canada Revenue Agency (CRA) by May 1.

- Interactive Brokers Central Europe Zrt. reports to the National Tax and Customs Administration of Hungary (NAV) by June 30.

- Interactive Brokers Hong Kong Limited reports to the Inland Revenue Department of Hong Kong SAR (IRD) by May 31.

- Interactive Brokers India Pvt. Ltd. reports to the Reserve Bank of India/Central Board of Direct Taxes (RBI/CBDT) by May 31.

- Interactive Brokers Ireland Limited reports to the Office of the Revenue Commissioners of Ireland by June 30.

- Interactive Brokers Securities Japan Inc. reports to the National Tax Agency of Japan (NTA) by April 30.

- Interactive Brokers Singapore Pte. Ltd. reports to the Inland Revenue Authority of Singapore (IRAS) by May 31.

- Interactive Brokers U.K. Limited reports to Her Majesty's Revenue and Customs of the United Kingdom (HMRC) by May 31.

- Additional Notes:

- Information relating to clients of Introducing Brokers is not reported by Interactive Brokers. Introducing Brokers are responsible for their own reporting under CRS.

- Accounts held by Interactive Brokers LLC are not reported under CRS as the United States has not signed the CRS.

FATCA Procedures - Grantor Trust Tax Information Submission

Overview:

Interactive Brokers is required to collect certain documentation from clients to comply with U.S. Foreign Account Tax Compliance Act (“FATCA”) and other international exchange of information agreements.

This guide contains instructions for a Trust to complete the online tax information and to electronically submit a W-9 or W-8BEN.

U.S. Tax Classification

Your U.S. income tax classification determines the tax form(s) required to document the account.

You must login to Account Management with the trust's primary username to access the Tax Form Collection page.

1. Tax Form Collection

The Tax Form Collection page lets account holders review and update important tax-related information and lets account holders electronically fill out an IRS Form W-9 (U.S. taxpayers) and IRS Form W-8 (non-U.S. taxpayers).

Accessing the Tax Form Collection Page

a. Click Manage Account > Account Information > Tax Information > Tax Forms.

b. Click the Update Tax Forms button to access the Collection page.

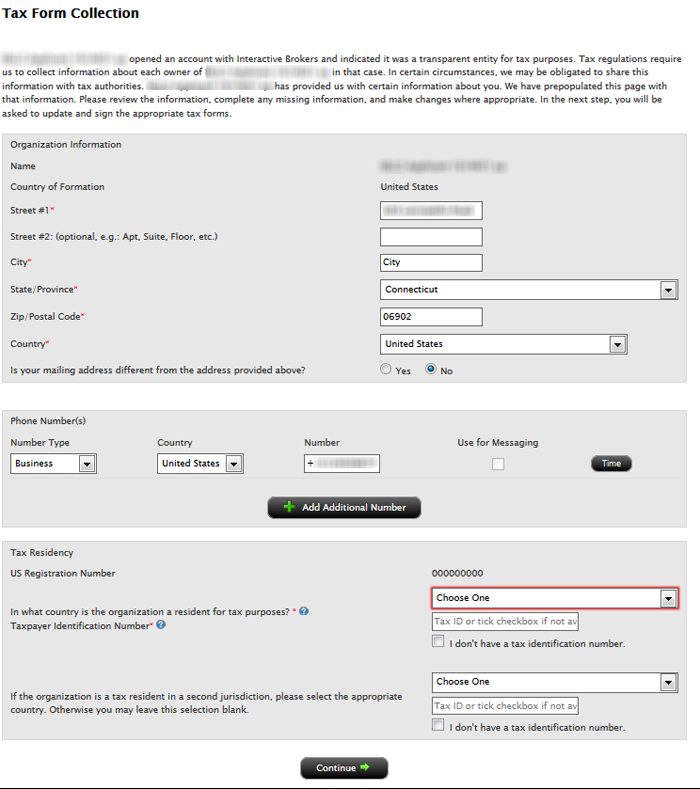

The Tax Form Collection page opens, displaying a form with tax-related information that should already be completed. (Advisors and brokers can check the status of client updates to this page on the Dashboard Pending Items tab.

c. Review the Trust’s information and update as required.

Confirm the primary tax residency of the trust beside the Tax Residency question, "In what country is the trust a resident for tax purposes?" Select the appropriate country in the drop down menu.

Select in the Tax Residency drop down menu the applicable country.

d. Click Continue.

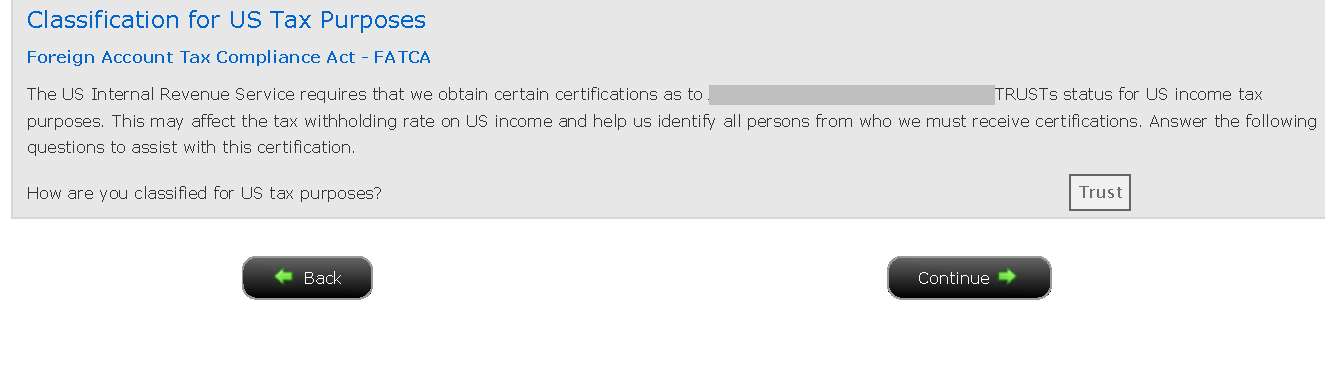

2. Classification for US Tax Purposes

Confirming the Trust’s classification for U.S. purposes

a. Review the Trust’s status by confirming the question, “How are you classified for US tax purposes?” The answer is pre-filled based upon your information completed during the account application process.

b. Click the Continue button to confirm the trust classification and complete the Form W-8 or W-9 for the entity.

c. Click the Continue button to identify each Grantor.

3. Identify Grantors

a. Click Manage Account > Account Information > Tax Information > Tax Forms.

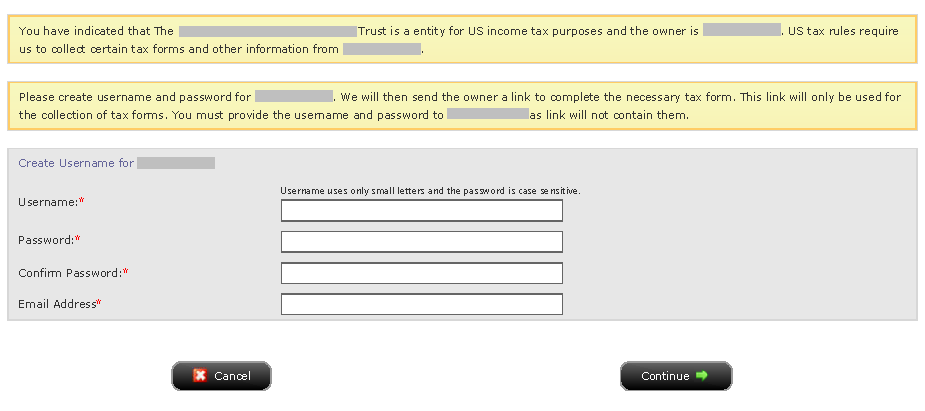

b. Click the Create button beside each grantor to send each user the applicable tax questionnaire and to submit the tax certification form (W-8 or W-9).

Also, update the "Percentage of Ownership" to add up to 100%, if necessary.

.png)

c. Enter the required fields for the username and password for specified grantor and click the Continue button to complete the email delivery of the link.

We will then send the owner a link to complete the necessary tax form. This link will only be used for the collection of tax forms. You must provide the username and password to the Grantor as link will not contain them.

Each Grantor must login with the username/password created and complete the pending tasks by going to Manage Account > Account Information > Tax Information > Tax Forms > Update Tax Forms.

d. Click the Continue button upon creating and sending usernames to each Grantor.

Disclaimer

This guide does not constitute tax or legal advice and Interactive Brokers cannot advise you on how to complete an IRS Forms W-8 or W-9. Instructions are for information purposes only and do not address all possible scenarios. Please consult your tax professional if you are unsure how to complete.

Indice delle domande frequenti relative all'accordo FATCA

Di seguito sono elencati i collegamenti a una serie di domande frequenti relative all'accordo FATCA suddivise per argomento. Per una panoramica generale dell'accordo FATCA, si prega di consultare l'articolo KB1986.

1. Generale (Si veda l'articolo KB2602)

2. Problematiche relative al luogo di nascita negli Stati Uniti (Si veda l'articolo KB2603)

3. Problematiche relative ai titolari di carta verde statunitense (Si veda l'articolo KB2604)

4. Problematiche relative al passaporto statunitense o ad altri documenti prova della cittadinanza statunitense (Si veda l'articolo KB2605)

5. Problematiche relative a indirizzi o numeri di telefono staunitensi (Si veda l'articolo KB2606)

6. Problematiche relative al disaccordo tra il Paese aderente alla convenzione fiscale e l'indirizzo fornito (Si veda l'articolo KB2607)

Si prega di notare che non forniamo alcuna consulenza fiscale. Per supporto alla compilazione dei moduli fiscali e per la definizione del proprio status di contribuente, si prega di consultare il proprio consulente fiscale.

Entity and FATCA Classification for Non-Financial Entities

Introduction

Interactive Brokers (“IB”, “we” or “us”) is required to collect certain documentation from clients (“you”) to comply with U.S. Foreign Account Tax Compliance Act (“FATCA”) and other international exchange of information agreements.

This guide contains a series of flowcharts and accompanying notes that summarize IRS rules relating to:

1. The tax classification for purposes of determining which W-8 or W-9 tax form an entity is required to complete; and

2. The FATCA classification required of entities completing the W-8 tax form (Part I, Section 5).

![]() Note: The flowcharts and notes contained herein do not cover every possible scenario and other scenarios not presented here exist and may more closely align with your situation. You should consult a tax professional regarding your particular circumstances if you are still unsure of your U.S. entity and/or FATCA classification after reading this guide.

Note: The flowcharts and notes contained herein do not cover every possible scenario and other scenarios not presented here exist and may more closely align with your situation. You should consult a tax professional regarding your particular circumstances if you are still unsure of your U.S. entity and/or FATCA classification after reading this guide.

What is NOT Covered in this Guide

The guide is directed to non-U.S. entities that (i) are the beneficial owners of the payments made to the account and (ii) are not financial institutions. This guide does not apply to:

• Individuals (use W-9 or W-8BEN)

• U.S. entities (use W-9)

• Entities acting as an intermediary (such as a nominee, broker, custodian, investment advisor) on behalf of another person (use W-8IMY).

• Non-U.S. Tax-Exempt Organizations and Private Foundations

• Financial Institutions

![]() Note: The U.S. entered into bilateral agreements called Intergovernmental Agreements (IGAs) with many countries regarding the implementation of FATCA. In some cases, the provisions of an applicable IGA could modify the results described in this guide. Entities are covered by an IGA should refer to the IGA and/or consult a tax professional for their filing requirements.

Note: The U.S. entered into bilateral agreements called Intergovernmental Agreements (IGAs) with many countries regarding the implementation of FATCA. In some cases, the provisions of an applicable IGA could modify the results described in this guide. Entities are covered by an IGA should refer to the IGA and/or consult a tax professional for their filing requirements.

1. U.S. Tax Classification

Your U.S. income tax classification determines the tax form(s) required to document the account. The flow chart below may help you determine your tax classification and the tax form to be completed.

Important: The U.S. imposes income tax on its residents’ worldwide income. On the other hand, nonresidents are only subject to withholding tax on certain limited types of US source investment income (dividends from U.S. companies, etc.). Completion of a W-8 series tax form certifies you are NOT taxable as a U.S. resident. A W-8 form may also be used to claim a reduced rate of withholding tax under a U.S. income tax treaty.

Flowchart for Determining Tax Classification and Required Tax Form (Non-Trust Entities)

.png)

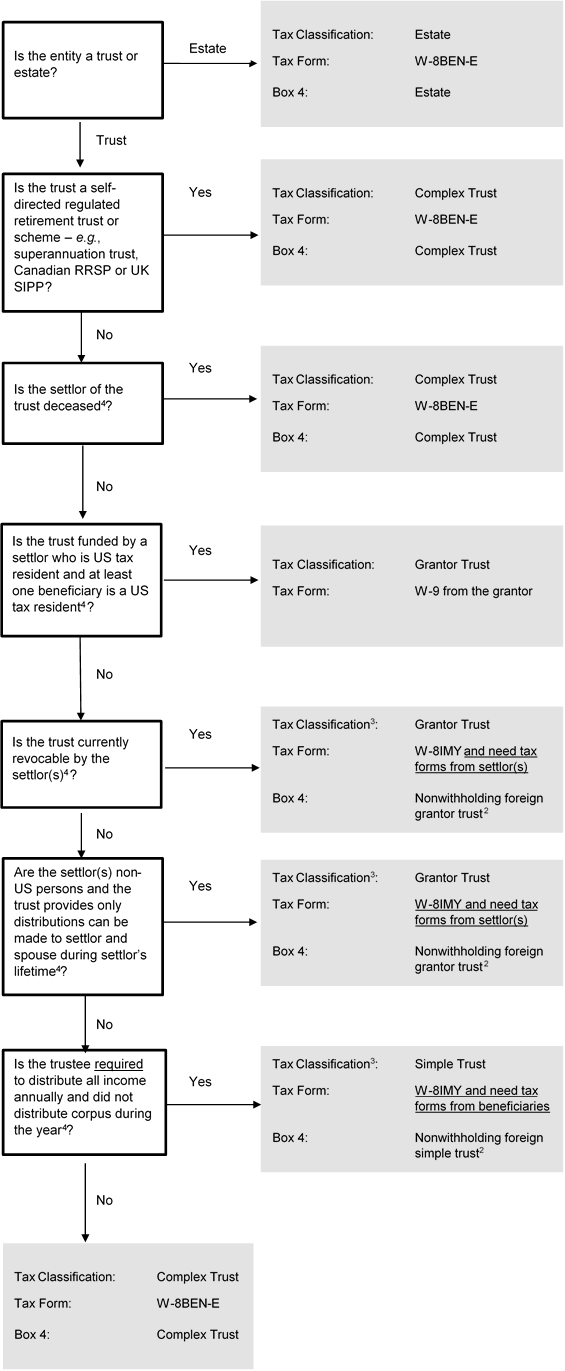

Flowchart for Determining Tax Classification and Required Tax Form (Trusts)

2. FATCA Classification

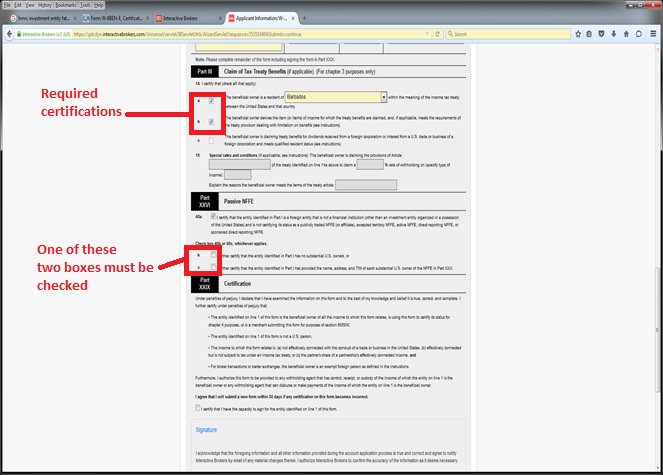

The W8 tax forms are also used to collect FATCA classifications. Many countries have executed “Intergovernmental Agreements (IGA)” with the U.S. requiring its local financial institutions to classify its customers for FATCA purposes. The classification rules under an IGA may not exactly match the classification rules established by the IRS. Other institutions have agreed with the IRS to become FATCA compliant and determine their customers’ FATCA classifications under the IRS rules. We are required to collect this information. The flowchart below applies the IRS default FATCA classification rules and is general in nature. The flowchart is accompanied by sample W-8BEN-E screenshots for a common account structure: a non-U.S. corporation classified for FATCA purposes as a Passive Non-Financial Foreign Entity (NFFE), which qualifies for treaty witholding rates.

![]() Note: It is important to recognize many organizations meet the qualifications for multiple FATCA types and you must select the most appropriate classification. Your specific situation may not fall within the general guidance. We recommend you seek your own independent advice as we are not in a position to make this determination for you and the rules are complex.

Note: It is important to recognize many organizations meet the qualifications for multiple FATCA types and you must select the most appropriate classification. Your specific situation may not fall within the general guidance. We recommend you seek your own independent advice as we are not in a position to make this determination for you and the rules are complex.

Flowchart for Determining FATCA Classification

.png)

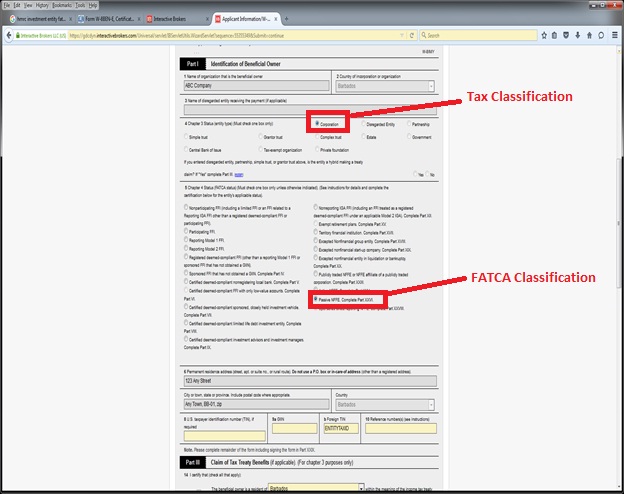

Example: A corporation is a common form of entity ownership, involving two or more owners with none having any personal liability for the debts of entity. As outlined in the Tax Classification flowchart above, an entity of this type would be required to complete the W-8BEN-E. Assuming the corporation is not classified as a Foreign Financial Entity (e.g. bank, broker, investment manager, hedge fund, mutual fund, insurance company) as discussed in footnote 5 below, then its FATCA classification would be Passive NFFE. Screenshots of the W-8BEN-E for this sample entity are provided below.

Sample Screenshots - W-8BEN-E (Passive NFFE)

Footnotes

1 The US Internal Revenue Service (IRS) established rules for determining the tax classification of entities formed outside the United States. These rules apply regardless of how the entity is classified in its country of organization or residency.

Generally corporate entities are treated as the beneficial owners of an account and should complete a W-8BEN-E and select “corporation” unless they elect otherwise (discussed below).

IRS regulations assign a default classification to each entity type. This default classification may be overridden by making a filing with the IRS and obtaining an US employer identification number. Certain entities cannot change their classification and are treated as corporations in all events (e.g., Sociedad Anonima, Public Limited Company and Aktiengesellschaft). A complete list may be found at US Treasury Regulation Section 301.7701-2(b)(8).

The IRS default classification usually depends on (i) the number of owners and (ii) whether any owner is personally liable for the debts of the entity based on the organizing statute (i.e., bank guarantees or other contractual agreements by owners are ignored). The following table summarizes the default rules:

|

|

Number of Owners

|

Owners have Limited Liability?

|

|

|||

|

|

Yes?

|

No?

|

|

|||

|

|

1 Owner

|

Corporation

|

Disregarded Entity

|

|

||

|

|

2+ Owners

|

Corporation

|

Partnership

|

|

||

|

|

|

|

||||

Note: Since the entity tax classification of a disregarded entity is determined by its owner, a US disregarded entity may find the flowchart helpful if the owner is a non-US entity.

A fiscally transparent entity (such as a partnership, simple trust or grantor trust) using IRS Form W-8IMY must provide IRS tax forms for all of its beneficial owners (partners in a partnership, beneficiaries for a simple trust and settlors for a grantor trust) for the account to be documented for US tax purposes.

Certain unit investment trusts (generally where there is an ability to vary the investments) are not considered trusts for US tax purposes. These investment trusts are treated in the same manner as a traditional business entity under the rules discussed above (i.e., corporation, partnership or disregarded entity).

Finally, a trust (other than a unit investment trust treated as a business entity) is considered a non-US trust for US tax purposes if (1) a court outside the United States is able to exercise primary supervision over the administration of the trust, and (2) any non-US person has the ability to control (or veto) any “substantial decision” of the trust.

The flowchart assumes that the default entity classification rules apply and the entity is not a per se corporation.

2 A partnership or simple or grantor trust may enter into a withholding agreement with the IRS pursuant to which the partnership or simple or grantor trust agrees to withhold US taxes on the account. The flowchart assumes no withholding agreement was executed.

3 In general, US tax treaty benefits are granted to the beneficial owner of the income determined under US tax principles. For fiscally transparent entities (such as partnerships, simple or grantor trusts or disregarded entities), this means the owners of the entity, NOT THE ENTITY ITSELF, claim US tax treaty benefits. These benefits are claimed on the beneficial owners’ W8 tax forms. However in certain limited cases, an entity may be considered fiscally transparent for US tax purposes but not fiscally transparent by the country with which the US has an income tax treaty. This type of an entity is called a “hybrid entity.” In certain cases, a hybrid entity, not the owners, may claim US tax treaty benefits if the hybrid entity meets the so-called qualified resident test under the applicable tax treaty. A qualifying “hybrid entity” claims the benefits of a US tax treaty by providing a Form W-8BEN-E, in addition to the form required by the flowchart. Importantly, electing hybrid status does not eliminate the need to document all beneficial owners. We note it is unusual for a hybrid entity to claim treaty benefits. The more common scenario is the beneficial owners claim treaty benefits on their tax forms.

4 The rules for classifying trusts are difficult and complex. The flowchart applies generalized rules only. There are many nuances to be considered when classifying a trust which are not addressed in the flowchart. For example, simple trusts cannot have charitable beneficiaries.

5 What is a foreign financial institution for FATCA purpose?

The various FATCA classifications can be broken down into two major categories: foreign financial institutions (FFI) and non-financial foreign (NFFE). Very generally, a financial institution is an entity that is a:

• Depository Institution

• Custodial Institution

• Investment Entity

• Insurance Company that issues certain cash value insurance or annuity contracts.

An FFI typically is required to register with the IRS, obtain a Global Intermediary Identification Number and report on its customers / owners to the appropriate tax authorities. If the entity does not meet the definition of a Financial Institution, it is considered an NFFE and covered by this guide book.

Subject to variations under IRS regulations and intergovernmental agreements:

• a Depository Institution is an institution that accepts deposits in the ordinary course of a banking or similar business. This includes banks and credit unions.

• a Custodial Institution is an institution which holds financial assets for the account of others as a substantial portion of its business. This includes brokers, custodial banks, trust companies, clearing organizations, etc.

• an Investment Entity is any entity if either

(i) the entity generates 50%+ of its gross income from (i) trading in money market instruments, foreign currency, transferrable securities, interest rates, futures, etc.; (ii) portfolio management or (iii) otherwise investing, administering or managing funds or financial assets on behalf of other persons (generally, broker-dealers and investment managers);

or

(ii) 50%+ of the entity gross income is attributable to investing, reinvesting, or trading in financial assets AND it is managed by a Financial Institution (mutual funds, hedge funds, and collective investment vehicles are examples);

or

(iii) the entity holds itself out as an entity created to invest, reinvest, or trade invest in financial assets (mutual funds, hedge funds, and collective investment vehicles are examples).

An individual cannot be an FFI. Thus, an organization managed by a professional individual investment advisor (as opposed to an employee of an organization) would not be considered an Investment Entity under (ii) above because it is not managed by a financial institution.

Trusts, family investment companies and funds may fall within the definition of an Investment Entity when they are professionally managed by a financial institution – i.e. where a financial institution handles the day-to-day functions of the entity or has discretionary authority over the fund.

Example: Individual created a non-US Trust A and appoints X, a non-US bank or other financial institution, as the trustee. X, as trustee, is responsible for the management and administration of Trust A. Trust A is an Investment Entity and a Foreign Financial Institution because it is managed by a Foreign Financial Institution.

Example: Individual created a non-US Trust A and appoints Y, an individual professional manager, as the trustee. Y, as trustee, is responsible for the management and administration of Trust A. Trust A is not an Investment Entity or a Foreign Financial Institution because it is not managed by a Foreign Financial Institution. Individuals cannot be financial institutions.

6 The IRS has a list of countries with which it has executed intergovernmental agreements (IGAs) to authorize the implementation of FATCA in that jurisdiction. The list of IGAs can be found at https://www.treasury.gov/resource-center/tax-policy/treaties/Pages/FATCA....

7 See #4 for the definition of Financial Institution. An organization that is not considered a financial institution is considered a non-financial foreign entity (NFFE). There are 3 types of NFFEs; Excepted, Active and Passive. An Active NFFE is an operating business where less than 50% of (i) its gross income is considered passive income and (ii) its average assets are held for the production of passive income. Any NFFE that is not Excepted or Active is a Passive NFFE and must provide us with a certification of its substantial US owners (if any) – generally 10%+ direct or indirect ownership. Some IGAs modify the means of substantial US owners and refer to them as Controlling Persons.

8 Other possible choices include nonfinancial group entity, excepted nonfinancial start-up company, excepted non-financial entity in liquidation or bankruptcy, publicly traded NFFE or sponsored NFFE. See the instructions to the W-8 for further information.

Disclaimer

This guide does not constitute tax or legal advice and Interactive Brokers cannot advise you on how to complete IRS Forms W-8. Examples included in this guide are for illustration only and do not address all possible scenarios. Please consult your tax professional if you are unsure how to complete IRS Forms W-8.

FATCA FAQs - Issues Involving Mismatch Between Tax Treaty Country and Address

FATCA related FAQs involving mismatches between tax treaty country and address. See KB2601 for other FATCA related FAQ topics.

Q1: I claimed treaty benefits in one country but have an address outside that treaty country. Why did I receive an email asking for additional documentation?

A1: We are required to verify your connection with the treaty country since you also have an address outside that country. We can process your claim for treaty benefits if you provide one document from Category (A) AND one document from Category (B) below.

|

Category (A)

|

AND

|

Category (B)

|

|

ANY OF the following unexpired documents issued by the treaty country:

|

ANY OF the following documents that match your address in the treaty country:

|

|

|

· Driver’s license

|

· Driver’s license

|

|

|

· Passport

|

· Bank or brokerage statement*

|

|

|

· National identity card

|

· Utility bill*

|

*Bank or brokerage statements and utility bills must be less than 12 months old. Alternatively, if you cannot provide documents from both categories, please provide a written explanation as to why you are entitled to treaty benefits together with any supporting documentation. Note: we may request further information or documentation from you depending on the explanation provided.

Q2: I submitted a proof of address and I received an email that the document submission did not resolve the issue. Why?

A2: Please confirm that the proof of identity you submitted was issued by the treaty country and that the proof of address relates to your address in the treaty country. A proof of address document alone is not sufficient to resolve the matter. Sometimes, customers inadvertently submit documentation for the other address. Please check the date of the proof of address document. We can only accept documents dated less than 12 months old. Also confirm you submitted a proof of identity document from the treaty country.

Q3: I live in Hong Kong and chose China as my tax treaty country on my Form W-8BEN. I received a notification saying the proof of address and proof of identity I submitted was not sufficient to claim benefits under the U.S.-China tax treaty. Hong Kong is a Special Administrative Region of the People’s Republic of China, so the U.S.-China tax treaty applies to it, correct?

A3: No. According to the US Internal Revenue Service, the U.S.-People’s Republic of China tax treaty does NOT apply to Hong Kong. Unless you can provide a proof of address and identity in the People’s Republic of China or provide other evidence that you are a tax resident of People’s Republic of China, you may not claim Chinese tax treaty benefits.

Q4: I live in Macau and chose China as my tax treaty country on my Form W-8BEN. I received an e-mail saying that the proof of address I submitted for my Macau address was not sufficient to claim benefits under the U.S.-China tax treaty. Macau is a Special Administrative Region of the People’s Republic of China, so the U.S.-China tax treaty applies to it, correct?

A4: No. According to the U.S. Internal Revenue Service, the U.S.- People’s Republic of China tax treaty does NOT apply to Macau. Unless you can provide a proof of address and identity in the People’s Republic of China or provide other evidence that you are a tax resident of People’s Republic of China, you may not claim Chinese tax treaty benefits.

Q5: I live in Taiwan, ROC and chose China as my tax treaty country on my Form W-8BEN. I received an e-mail saying that the proof of address I submitted for my address in Taiwan, ROC was not sufficient to claim benefits under the U.S.-China tax treaty. Taiwan, ROC is formally known as the Republic of China, so the U.S.-China tax treaty applies to it, correct?

A5: No. According to the US Internal Revenue Service, the U.S.- People’s Republic of China tax treaty does NOT apply to Taiwan, ROC. Unless you can provide a proof of address in People’s Republic of China or provide other evidence that you are a tax resident of People’s Republic of China, you may not claim Chinese tax treaty benefits.

Q6: The information you have in your master file is out-of-date. I moved so that the address you identified as outside the treaty country is incorrect. What should I do?

A6: The fastest and most effective way to remedy the situation is to provide the requested information (see FAQ#1 above) so that our records are complete. You should also log into Account Management and make any required changes to your personal information.

We do not provide tax advice. Please consult your tax advisor for advice in completing tax forms and determining your taxpayer status.

FATCA FAQs - Issues Involving U.S. Address or Telephone Number

FATCA related FAQs involving U.S. address or telephone number. See KB2601 for other FATCA related FAQ topics.

Q1: I received a notification that a review of my file indicated a U.S. address or telephone and additional information is required. What additional information do I need to provide?

A1: You need to provide one document from Category (A) AND one document from Category (B) from the table below AND a written explanation explaining the U.S. address.

|

Category (A)

|

AND

|

Category (B)

|

AND

|

Category (C)

|

|

ANY OF the following documents issued by a non-US country:

|

ANY OF the following documents that match your foreign address:

|

A reasonable written explanation supporting your claim of non-US status.

|

||

|

· Driver’s license

|

· Driver’s license

|

|||

|

· Passport

|

· Bank or brokerage statement*

|

|||

|

· National identity card

|

· Utility bill*

|

*Bank or brokerage statements and utility bills must be less than 12 months old.

Q2: The day count table on the account application says I am a U.S. tax resident and will not let me complete IRS Form W-8. What should I do?

A2: The US Internal Revenue Service generally considers individuals who spend a significant number of days in the United States each year to be U.S. taxpayers. The table flags customers who exceed those IRS rules for U.S. income tax residency and requires a W-9. Alternatively, it may be possible for you to satisfy the “closer connection test” or utilize a U.S. tax treaty to avoid U.S. tax residency. Please refer to IRS Publication 519 for details or consult a tax professional regarding IRS rules for counting days, the closer connection test and U.S. tax treaties.

Q3: I am a studying in the U.S. and present on an F-1 visa. I responded to your email and provided a copy of my F-1 visa. I received an email saying my response was insufficient to resolve the issue. Why?

A3: Please check the expiration date of your visa. If your visa has expired, please provide other evidence of your status, such as an Optional Practical Training (OPT) card, a copy of Form I-20 endorsed by the DSO for your school or another Employment Authorization Document (EAD). Also confirm you submitted the necessary proof of identify and address documentation.

Q4: I use my daughter’s address to receive all mail. She lives in the United States. What should I do?

A4: In this case, you can probably satisfy the substantial presence test noted in the notification you've received . Please provide the number of days you spent or plan to spend in the U.S. in the current and prior two years (e.g., 2015, 2014 and 2013). Also refer to the documentation requirements outlined in FAQ#1 above.

Q5: The address or telephone you noted in your email is out-of-date. I have since moved out of the United States. What should I do?

A5: The fastest and most effective way to remedy the situation is to provide the information as requested in the notification you've received (see FAQ#1 above), so that our records are complete. You should also log into Account Management and make any required changes to your personal information of record.

We do not provide tax advice. Please consult your tax advisor for advice in completing tax forms and determining your taxpayer status.