Key Information Documents (KID)

Overview:

IBKR is required to provide EEA and UK retail customers with Key Information Documents (KID) for certain financial instruments.

Relevant products include ETFs, Futures, Options, Warrants, Structured Products, CFDs and other OTC products. Funds include both UCITS and non-UCITS funds available to retail investors.

Generally KIDs must be provided in an official language of the country in which a client is resident.

However, clients of IBKR have agreed to receive communications in English, and therefore if a KID is available in English all EEA and UK clients can trade the product regardless of their country of residence.

In cases where a KID is not available in English, IBKR additionally supports other languages as follows:

| Language | Can be traded by residents or citizens* of |

| German | Germany, Austria, Belgium, Luxembourg and Liechtenstein |

| French | France, Belgium and Luxembourg |

| Dutch | the Netherlands and Belgium |

| Italian | Italy |

| Spanish | Spain |

*regardless of country of residence

EMIR: обязательства по отчетности в торговые репозитарии и услуги Interactive Brokers по предоставлению отчетности за клиентов

1. Общая информация. В 2009 году G20 договорились о проведении реформ, призванных повысить прозрачность и уменьшить контрагентский риск на внебиржевом рынке деривативов после финансового кризиса 2008 года. Проведение этих реформ в ЕС закреплено Правилами регулирования инфраструктуры европейского финансового рынка ("EMIR"). EMIR является регламентом Европейского союза, который вступил в силу 16 августа 2012 г.

2. Финансовые инструменты, подотчетные согласно регламенту EMIR – биржевые и внебиржевые деривативы следующих классов активов: кредитные, процентные, товарные, валютные деривативы, а также деривативы на акции. Обязательства по предоставлению отчетности не распространяются на биржевые варранты.

3. К кому относятся обязательства об отчетности EMIR. Как правило, отчетные обязательства действуют в отношении всех контрагентов, учрежденных в ЕС, кроме физических лиц. Данные обязательства должны соблюдать:

* Финансовые контрагенты (ФК);

* Нефинансовые контрагенты, превышающие клиринговый порог (НФК+)

* Нефинансовые контрагенты, не превышающие клиринговый порог (НФК-)

* Лица из третьих стран, не входящих в ЕС – в отдельных случаях.

Другими словами, обязательства распространяются на все юридические лица, учрежденные в ЕС, которые совершают сделки с деривативами.

4. Финансовые контрагенты (ФК) включают банки, инвестиционные компании, кредитные и страховые организации, соглашения о совместных инвестициях в ценные бумаги (UCITS), пенсионные фонды и фонды альтернативных инвестиций под управлением менеджера. Альтернативный инвестиционный фонд (АИФ) является ФК только в том случае, если менеджер этого фонда зарегистрирован согласно Директиве ЕС о менеджерах фондов альтернативных инвестиций, поэтому обязательства о предоставлении отчетности EMIR также могут распространяться на фонды за пределами ЕС.

5. Нефинансовые контрагенты (НФК) – это организации, учрежденные в ЕС, которые не подпадают под определение финансового контрагента или центрального контрагента (например, клиринговые палаты). НФК имеют меньше обязательств, чем ФК. Однако когда НФК превышает установленный "клиринговый порог", он становится НФК+, и тогда для него начинают действовать почти те же требования, как и для ФК (включая отчетность об обеспечении и оценке стоимости). НФК, не превышающие клиринговый порог, обозначаются как "НФК-". На практике к НФК- относятся все лица, кроме частных физических лиц (в т.ч. частных лиц, владеющих совместным счетом).

СЕРВИС ДЕЛЕГИРОВАННОЙ ОТЧЕТНОСТИ INTERACTIVE BROKERS ДЛЯ ПОМОЩИ В СОБЛЮДЕНИИ ОТЧЕТНЫХ ОБЯЗАТЕЛЬСТВ

6. Какие услуги предоставляет Interactive Brokers, чтобы помочь своим клиентам соблюсти требования о предоставлении отчетов, включая делигирование ведения отчетности о сделках и получения LEI. Как описано выше, ФК и НФК обязаны передавать данные о транзакциях (с биржевыми и внебиржевыми деривативами) в уполномоченные торговые репозитарии. Данное обязательство можно исполнить напрямую через торговый репозитарий или перепоручив исполнение этих обязательств контрагенту или сторонней организации (которые предоставят отчеты за своих клиентов).

Interactive Brokers оказывает помощь в получении LEI и предоставлении отчетов для клиентов, для которых компания исполняет сделки и проводит клиринг, в объеме, разрешенном в рамках ведения деятельности и действующего законодательства (при получении соответствующего разрешения от клиента).

Если на Вас распространяется требование о предоставлении отчетов EMIR, в ближайшее время Вы сможете войти в систему управления счетом IB, подать заявку на LEI и поручить Interactive Brokers передавать за Вас данные.

Сервис также включает отчетность об оценке стоимости, однако только в том случае, в той мере и до того срока, которые установлены нормативно-правовыми требованиями, и пока контрагент несет такие обязательства (т.е. когда он является ФК и НФК+).

Примите к сведению, что в рамках отчетности Interactive Brokers использует собственные данные об оценке стоимости.

7. Можно ли делегировать предоставление отчетности EMIR. EMIR позволяет любому контрагенту делегировать свои обязательства по отчетности сторонней организации. Если контрагент или центральный контрагент делегируют свои отчетные обязательства сторонней организации, он все равно несет полную ответственность за соблюдение требований об отчетности. Аналогичным образом, контрагент или центральный контрагент должны проконтролировать, чтобы данная сторонняя организация правильно передала необходимые данные. Брокеры и дилеры не обязаны предоставлять отчеты, если они выступают только в роли посредника. Если для выполнения крупной сделки совершаются несколько транзакций, то в отчете должна быть отражена каждая транзакция.

ФОНДЫ И СУБФОНДЫ – обязательства EMIR могут распространяться на фонды и субфонды. Фонды и субфонды, которые выступают в транзакции в роли принципала, должны предоставить данные о своем статусе (ФК, НФК+ или НФК-), разрешение на делегирование отчетности и заявление на получение кода идентификации юр. лица LEI (Legal Entity Identifier).

8. Исключения согласно статье 1(4) и 1(5) регламента EMIR. Статьи 1(4) и 1(5) EMIR описывают случаи, в которых некоторые организации частично или полностью освобождаются от обязательств, оговоренных в EMIR, в зависимости от категории. А именно, организации, подпадающие под положения статьи 1(4), освобождаются от всех обязательств EMIR, а организации, подпадающие под положения статьи 1(5), освобождаются от всех обязательств кроме требований об отчетности.

9. Организации, подпадающие под положения статьей 1(4) и 1(5) EMIR. Статья 1(4) изначально применялась только к центральным банкам ЕС, государственным органам, связанным с управлением государственным долгом, и Банку международных расчетов. Впоследствии сфера применения статьи 1(4) была расширена и стала включать центральные банки и органы управления гос. долгом США и Японии. Комиссия сообщила, что в дальнейшем к данному положению могут быть добавлены другие иностранные центральные банки и органы управления гос. долгом, если в их юрисдикции будут приняты аналогичные нормы. Статья 1(5) в общих чертах оговаривает исключение для следующих категорий организаций:

- Многосторонние банки развития;

- Некоммерческие государственные компании во владении и под гарантией центрального правительства; и

- Европейский фонд финансовой стабильности (EFSF) и Европейский стабилизационный механизм (ESM).

10. Биржевые и внебиржевые деривативы. В рамках регламента I уровня, для биржевых и внебиржевых деривативов действуют одинаковые требования по отчетности, применения технических стандартов и нормативных технических стандартов ESMA.

Контракт должен быть идентифицирован с помощью уникального кода. Кроме того, у каждой транзакции должен быть свой уникальный код. Если не выработана общепризнанная система кодов для продукта, в качестве альтернативы рекомендуется использовать международный идентификационный код ISIN, альтернативный идентификатор инструмента AII или классификационный код финансового инструмента CFI.

11. Торговый репозитарий, который использует Interactive Brokers. Interactive Brokers (U.K.) Limited пользуется услугами Европейского торгового репозитария CME ETR, который входит в CME Group.

12. Получение идентификатора юр. лица LEI

В целях соблюдения отчетных обязательств, любой европейский контрагент, участвующий в сделках с деривативами, должен иметь идентификатор юридического лица LEI (Legal Entity Identifier). LEI используется для передачи данных контрагента.

LEI – это уникальный код, закрепленный за юридическим лицом или структурой, который позволяет однозначно определить стороны финансовой транзакции.

EMIR: дополнительная информация по предоставлению отчетов в торговые репозитарии.

13. Порог для определения статуса НФК как НФК+ или НФК-. При достижении любого из указанных ниже клиринговых порогов контрагент классифицируется как НФК+. Позиции рассчитываются на основе номинальной, скользящей средней величины за 30 дней:

• 1 млрд евро в валовом номинальном выражении для внебиржевых кредитных деривативных контрактов;

• 1 млрд евро в валовом номинальном выражении для внебиржевых деривативных контрактов на акции;

• 3 млрд евро в валовом номинальном выражении для процентных деривативных контрактов;

• 3 млрд евро в валовом номинальном выражении для валютных деривативных контрактов; и

• 3 млрд евро в валовом номинальном выражении для товарных деривативных контрактов и других внебиржевых деривативных контрактов, не перечисленных выше.

Чтобы рассчитать, достиг ли НФК установленного порога, контрагент должен объединить транзакции всех нефинансовых организаций в своей группе (и определить, находятся ли они в ЕС или нет) и вычесть транзакции, совершенные в целях хеджирования. Термин "хеджевая сделка" в данном случае означает транзакции, которые объективно снижают риск, напрямую связанный с коммерческой деятельностью или финансовой деятельностью НФК или его группы.

14. Отчет о рисках. ФК и НФК+ должны предоставлять следующие отчеты:

* Переоценка стоимости каждого контракта по рынку или модели.

* Данные об обеспечении для каждой транзакции или всего портфеля (т.е. в случае, когда обеспечение рассчитывается на основе чистых позиций, полученных в результате нескольких контрактов, а не предоставляется для каждой транзакции по отдельности).

15. График предоставления отчетности в торговые репозитарии. Предоставлять отчет необходимо с 12 февраля 2014 года:

* Для новых контрактов, созданных с 12 февраля – на следующий день (T + 1);

* Для позиций, открытых по контрактам, созданным с 16 августа 2012 г. и все еще открытым по состоянию на 12 февраля 2014 г. – отчет должен быть отправлен в торговый репозитарий до 12 февраля 2014 г.;

* Для позиций, открытых по контрактам, созданным до 16 августа и все еще открытым по состоянию на 12 февраля 2014 г. – отчет должен быть отправлен в торговый репозитарий до 13 мая 2014 г.;

* Отчет об оценке стоимости и обеспечении должен быть отправлен в торговый репозитарий до 12 августа 2014 г.;

* По контрактам, созданным до, после или 16 августа 2012 г., но не открытые по состоянию на 12 февраля 2014 г., отчет должен быть отправлен в торговый репозитарий до 12 февраля 2017 г.

16. Что должно быть в отчете и сроки. В отчете необходимо предоставить информацию о контрагентах по каждой сделке (данные контрагентов) и о самих контрактах (общие данные).

В отношении контрагентов необходимо предоставить информацию по 26 пунктам, а отчет по общим данным состоит из 59 пунктов. Эти пункты содержатся в таблицах 1 и 2 Приложения к Нормативным техническим стандартам ESMA об обязательных данных для передачи в торговые репозитарии.

Контрагенты и центральные контрагенты должны подавать отчет:

* когда контракт создается;

* когда контракт меняется;

* когда контракт закрывается.

Отчет должен быть отправлен не позже, чем окончание рабочего дня, следующего за созданием, изменением или окончанием контракта.

17. Что должно быть включено в отчет, и кто должен его предоставить. Отчет необходимо отправлять по биржевым и внебиржевым деривативам. Отчетные обязательства распространяются на контрагентов в сделке вне зависимости от их классификации. Примечание:

* Отчет об оценке стоимости и обеспечении должны предоставлять только ФК и НФК+.

* Отчет о сделке, как правило, должны предоставлять оба контрагента.

ЭТА ИНФОРМАЦИЯ ПРЕДНАЗНАЧЕНА ДЛЯ КЛИЕНТОВ ТОЛЬКО В СЛУЧАЯХ, КОГДА КЛИРИНГ ПО ИХ СДЕЛКАМ ОСУЩЕСТВЛЯЕТ INTERACTIVE BROKERS

ВНИМАНИЕ! ДАННАЯ ИНФОРМАЦИЯ НЕ ЯВЛЯЕТСЯ ВСЕОБЪЕМЛЮЩИМ ИЛИ ИСЧЕРПЫВАЮЩИМ ТОЛКОВАНИЕМ УПОМЯНУТЫХ ПОЛОЖЕНИЙ, А ПРЕДСТАВЛЯЕТ СОБОЙ ОБЩИЙ ОБЗОР ПРАВИЛ EMIR, УСТАНОВЛЕННЫХ ESMA, И СВЯЗАННЫХ С НИМИ ОТЧЕТНЫХ ОБЯЗАТЕЛЬСТВ.

Исполнение правил ESMA в отношении операций с CFD для розничных клиентов IBIE и IBCE

Overview:

|

CFD – это сложные инструменты, которые сопряжены с высоким риском убытков из-за использования кредитного плеча. 68,7% счетов розничных инвесторов терпят убытки при торговле CFD через IBKR. Убедитесь, что Вы понимаете принцип работы CFD и в состоянии принять на себя высокий риск убытков. |

Европейская служба по ценным бумагам и рынкам (ESMA) ввела новые правила по CFD для розничных клиентов, вступившие в силу 1 августа 2018 года. Они не распространяются на профессиональных клиентов.

Государственные регулирующие органы приняли положения ESMA на постоянной основе.

В правила входят: 1) ограничения кредитного плеча; 2) правило ликвидации согласно марже конкретного счета; 3) защита счета от отрицательного баланса; 4) ограничение поощрительных программ по торговле CFD; и 5) стандартное предупреждение о рисках.

Большинство клиентов (за исключением регулируемых юр. лиц) изначально классифицируются как розничные. В некоторых случаях IBKR может согласиться изменить статус розничного клиента на "профессиональный" или наоборот. Подробнее можно узнать в статье "Классификация MiFID".

Следующие разделы описывают, как решение ESMA соблюдается в IBKR.

1. Ограничения кредитного плеча

1.1. Маржа согласно правилам ESMA

ESMA установила ограничения кредитного плеча, отличающиеся в зависимости от андерлаинга:

- 3,33% для основных валютных пар. Основные валютные пары – это любые комбинации USD; CAD; EUR; GBP; CHF; JPY.

- 5% для прочих валютных пар и основных индексов;

- Прочие (не основные) валютные пары – это комбинации, в которые входит валюта, не указанная выше (например, USD.CNH)

- Основные индексы: IBUS500; IBUS30; IBUST100; IBGB100; IBDE40; IBEU50; IBFR40; IBJP225; IBAU200

- 10% для прочих фондовых индексов: IBES35; IBCH20; IBNL25; IBHK50

- 20% для отдельных акций

1.2. Применяемая маржа – стандартные требования

Вдобавок к марже ESMA, компания IBKR устанавливает свои собственные минимальные маржинальные требования ("Маржа IB") согласно исторической волатильности андерлаинга и прочим факторам, описанным ниже.Маржа IB применяется, если она выше предписанной ESMA.

Подробнее о действующих маржинальных требованиях IB и ESMA можно узнать здесь.

1.2.1. Применяемая маржа – минимальный уровень концентрации

С портфеля взимается плата за концентрацию, если он состоит из малого числа позиций с CFD или его основной вес приходится на две крупнейшие позиции. Мы проводим тест для портфеля, моделируя неблагоприятный сдвиг в 30% для двух крупнейших позиций и в 5% – для остальных. Если общий убыток превышает стандартное маржинальное требование, то он устанавливается в качестве минимального требования. Обратите внимание, что плата за концентрацию – это единственный случай, когда маржа для позиций с CFD и акциями рассчитывается вместе.

1.3. Обеспечение начальных маржинальных требований

Выполнение начальных маржинальных требований при открытии позиции по CFD возможно только за счет денежных средств.

Изначально все денежные средства, внесенные на счет, доступны для сделок с CFD. Любые начальные маржинальные требования для других инструментов и средства, использованные для покупки акций, уменьшают сумму доступных средств. Если покупка акций привела к образованию маржинального кредита, то для торговли CFD не осталось доступных средств, даже если на Вашем счете есть большой капитал. Согласно правилам ESMA, IBKR не может увеличить маржинальный кредит для обеспечения маржи для CFD.

Реализованная прибыль по CFD включается в денежный остаток и становится доступна сразу – расчета ждать не нужно. В то же время нереализованный доход не может использоваться для покрытия начальной маржи.

2. Правило ликвидации

2.1. Расчет минимальной маржи и ликвидация

Согласно правилам ESMA, IBKR обязана ликвидировать CFD-позиции до того, как доступный остаток счета опустится ниже 50% от начальной маржи, внесенной при открытии этих позиций. IBKR может закрыть позиции раньше, если внутренние правила в отношении риска являются более строгими. В рассматриваемый для этих целей капитал входят денежные средства по CFD и нереализованная ПиУ по CFD (положительная и отрицательная). Обращаем Ваше внимание, что денежные средства по CFD не включают средства, обеспечивающие маржинальные требования для других инструментов.

Основой расчета служат начальные маржинальные требования, действовавшие при открытии позиции по CFD. Другими словами, в отличие от расчетов маржи других продуктов сумма начальной маржи СFD не меняется при росте/снижении стоимости соответствующих открытых позиций.

2.1.1. Пример

Денежный остаток на Вашем счете составляет 2000 EUR, и на нем нет открытых позиций. Вы хотите купить 100 CFD на XYZ по лимитной цене в 100 EUR. Сначала выполняется покупка первых 50 CFD, а затем оставшихся 50. Сумма Ваших доступных средств уменьшается по мере исполнения:

|

|

Наличные средства |

Капитал* |

Позиция |

Цена |

Стоимость |

Нереализ. ПиУ |

НМ |

ММ |

Доступные средства |

Нарушение ММ |

|

Перед сделкой |

2000 |

2000 |

|

|

|

|

|

|

2000 |

|

|

После сделки 1 |

2000 |

2000 |

50 |

100 |

5000 |

0 |

1000 |

500 |

1000 |

Нет |

|

После сделки 2 |

2000 |

2000 |

100 |

100 |

10000 |

0 |

2000 |

1000 |

0 |

Нет |

*Капитал – это денежный остаток (наличные) плюс нереализованная ПиУ.

Цена вырастает до 110. Теперь Ваш капитал равен 3000, но Вы не можете открывать дополнительные позиции, поскольку Ваши доступные денежные средства все еще составляют 0, и, согласно правилам ESMA, начальная и минимальная маржа не меняются.

|

|

Наличные средства |

Капитал |

Позиция |

Цена |

Стоимость |

Нереализ. ПиУ |

НМ |

ММ |

Доступные средства |

Нарушение ММ |

|

Изменение |

2000 |

3000 |

100 |

110 |

11000 |

1000 |

2000 |

1000 |

0 |

Нет |

Затем цена опускается до 95. Ваш капитал снижается до 1500, что не нарушает требования маржи, поскольку он все еще превышает 1000:

|

|

Наличные средства |

Капитал |

Позиция |

Цена |

Стоимость |

Нереализ. ПиУ |

НМ |

ММ |

Доступные средства |

Нарушение ММ |

|

Изменение |

2000 |

1500 |

100 |

95 |

9500 |

(500) |

2000 |

1000 |

0 |

Нет |

Цена снова снижается до 85, что приводит к нарушению маржинальных требований и ликвидации:

|

|

Наличные средства |

Капитал |

Позиция |

Цена |

Стоимость |

Нереализ. ПиУ |

НМ |

ММ |

Доступные средства |

Нарушение ММ |

|

Изменение |

2000 |

500 |

100 |

85 |

8500 |

(1500) |

2000 |

1000 |

0 |

Да |

3. Защита от отрицательного капитала

Решение ESMA ограничивает Вашу ответственность по контрактам CFD до суммы, выделенной на сделки с ними. Для устранения дефицита маржи CFD не могут быть ликвидированы другие финансовые инструменты (например, акции или фьючерсы)*.

Поэтому другие активы не подвергаются риску при торговле CFD.

Если Вы потеряете больше, чем выделили на торговлю CFD, IB обязана списать эти убытки.

Поскольку защита от отрицательного капитала представляет дополнительный риск для IBKR, с розничных инвесторов будет взиматься дополнительная надбавка в 1% за позиции с CFD, переносимые на следующий день. Точные ставки финансирования CFD указаны на этой странице.

Хотя для покрытия недостающей маржи по CFD нельзя ликвидировать позиции с другими активами, позиции с CFD могут быть ликвидированы для устранения дефицита маржи других инструментов.

Окно "Счет" в TWS для клиентов IBKR Ireland и IBKR Central Europe

Overview:

В данной статье описывается содержимое раздела "Счет" в TWS для клиентов IBKR из ЕС.

|

CFD – это сложные инструменты, которые сопряжены с высоким риском убытков из-за использования кредитного плеча. 63,7% счетов розничных инвесторов терпят убытки, торгуя CFD через IBKR. Убедитесь, что Вы понимаете принцип работы CFD и в состоянии принять на себя высокий риск убытков. |

Background:

Для розничных клиентов, проживающих в ЕЭЗ и имеющих счет в одном из европейских филиалов IBKR – IBIE или IBCE – действуют нормативы ЕС в отношении левериджа и другие ограничения для транзакций с контрактами на разницу (CFD).

В частности, данные нормативы обязывают использовать свободные денежные средства для соблюдения маржинальных требований для CFD и запрещают розничным клиентам использовать ценные бумаги на своем счете в качестве залога для займа средств с целью открыть или сохранить позицию с CFD. Подробнее можно узнать в статье Обзор положений ESMA в отношении операций с CFD для розничных клиентов IBIE и IBCE.

Счета клиентов в европейских филиалах IBKR являются универсальными счетами, на которых клиенты могут торговать всеми классами активов, доступных на платформе IBKR, но, в отличие от филиалов IBKR в США и Великобритании, счет нельзя разделить на сегменты с независимыми балансами.

Ниже приведены примеры применения данного ограничения и информация о том, как клиенты могут следить за доступным свободным остатком для транзакций с CFD.

Раздел "Счет"

Чтобы соблюсти правило в отношении свободных средств, IBKR рассчитывает объем средств, доступных для торговли CFD в реальном времени, отклоняет новые ордера и ликвидирует существующие позиции, если на счете недостаточно свободных средств для покрытия начальной и минимальной маржи для CFD.

Клиенты IBKR могут проверить остаток свободных средств, доступных для транзакций с CFD, в разделе "Счет" в TWS. Важно отметить, что если средства показаны как доступные для торговли CFD, то это не значит, что они хранятся в отдельном сегменте счета. В окне просто отображается часть баланса, доступная для сделок с CFD.

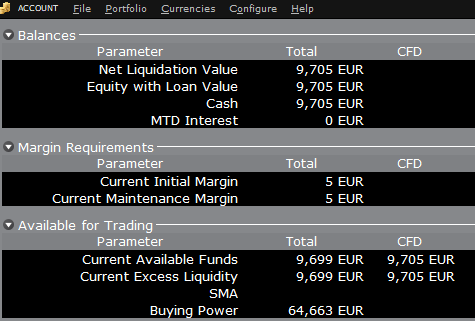

Например, представим, что на счете есть средства на сумму 9 705 EUR и нет позиций. Вся эта сумма доступна для открытия позиции с CFD или любым другим классом активов:

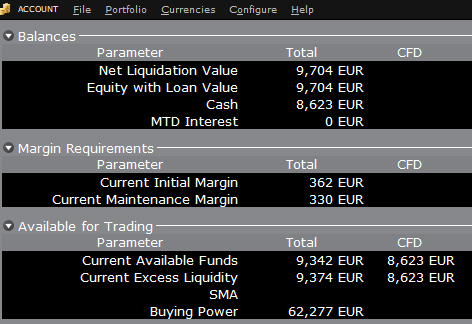

Если инвестор покупает 10 акций AAPL на общую сумму 1 383 USD, то баланс счета

уменьшается на соответствующую сумму в EUR и средства, доступные для сделок с CFD, уменьшаются

на эту же сумму:

При этом общий доступный баланс уменьшается на меньшую сумму в соответствии с маржинальным требованием для акций.

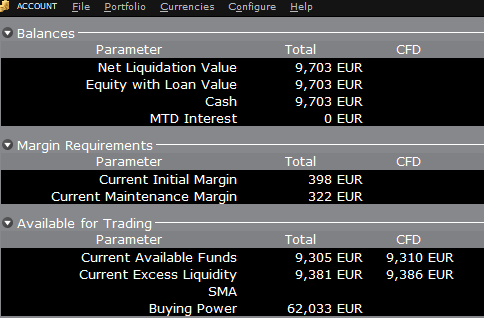

Если вместо акций AAPL инвестор покупает 10 контрактов CFD на AAPL, то результат будет другой. Поскольку инвестор покупает деривативный контракт, а не андерлаинг, то денежный баланс счета не уменьшается, но сумма средств, доступных для торговли CFD, уменьшается на размер маржинального требования для CFD в целях обеспечения контракта:

В таком случае общий доступный баланс и средства, доступные для сделок с CFD, уменьшаются на равную сумму – размер маржинального требования для CFD.

Внесение средств

Как уже говорилось выше, счета в ЕС не делятся на сегменты, поэтому клиентам не нужно выполнять внутренние переводы. Средства доступны для сделок со всеми классами активов на суммы, указанные в разделе "Счет", без необходимости автоматических списаний и переводов.

Если инвестор взял маржинальный кредит, т.е. на счете отрицательный баланс, то он не сможет открыть позиции с CFD, поскольку маржинальное требование по CFD должно быть обеспечено за счет свободного – т.е. положительного – остатка. Если Вы взяли маржинальный кредит и хотите торговать CFD, то Вам необходимо закрыть маржинальные позиции (и, тем самым, кредит) или внести дополнительные средства на счет на сумму, достаточную, чтобы покрыть маржинальный кредит и создать резерв для соблюдения маржинальных требований по CFD.

TWS Account Window for Retail Clients of IBKR Ireland and Central Europe

Overview:

This article describes the information provided in the TWS account window for IBKRs EU based entities.

|

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 61% of retail investor accounts lose money when trading CFDs with IBKR. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. |

Background:

Retail clients who are residents of the EEA and therefore maintain an account with one of IBKR’s European brokers, IBIE or IBCE, are subject to EU regulations which introduce leverage and other restrictions applicable to CFD transactions.

Notably the regulations require the use of free cash to satisfy CFD margin requirements and prohibit retail clients from using securities in the account as collateral to borrow funds to initiate or maintain a CFD position. Please see Overview of ESMA CFD Rules Implementation for Retail Clients at IBIE and IBCE for full details.

The accounts of IBKRs EU entities are universal accounts in which clients can trade all asset classes available on IBKRs platform, but unlike IBKRs US and UK entities, there are no separately funded segments.

Working examples of how this restriction is applied, along with details as to how clients can monitor free cash available for CFD transactions, are outlined below.

Account Window

IBKR enforces the restriction relating to free cash by calculating the funds available for CFD trading on a real-time basis, rejecting new orders and liquidating existing positions when the available free cash is insufficient to cover CFD initial and maintenance margin requirements.

IBKR offers clients the ability to monitor free cash available for CFD transactions via an enhancement to the TWS Account Window which displays the level of free cash in the account. Importantly, the funds shown as available for CFD trading do not imply that cash is held in a separate segment. It simply indicates what proportion of total account balances is available for CFD trading.

For example, assume that an account has EUR 9,705 in cash and no positions. All the cash is available to open CFD positions, or positions in any other asset class:

If the account now purchases 10 shares of AAPL stock for an aggregate value of USD 1,383 the cash in the account is reduced by a corresponding amount in EUR, and the funds available for CFD trading are reduced by the

same amount:

Note that Total available funds are reduced by a smaller amount, corresponding to the stock margin requirement.

If, instead of buying AAPL stock, the account buys 10 AAPL CFDs the impact will be different. As the transaction involves a derivative contract rather than the purchase of the underlying asset itself, there’s no reduction in cash but the funds available for CFDs are reduced by the CFD margin requirement to secure performance on the contract:

In this case Total available funds and CFD available funds are reduced by an equal amount; the CFD margin requirement.

Funding

As noted above, EU-based accounts do not have segments and therefore there is no need for internal transfers. Funds are available for trades in all asset classes in the amounts indicated in the account window, without the need for sweeps or transfers.

Note also that should an account have a margin loan, i.e. negative cash, it will not be possible to open CFD positions since the CFD margin requirement must be satisfied by free, positive cash. Should you have a margin loan and wish to trade CFDs you must first either close margin positions to eliminate the loan, or add cash to the account in an amount that covers the margin loan and creates a cash buffer sufficient for the necessary CFD margin.

IBKR Metals CFDs – Facts and Q&A

Overview:

The following article is intended to provide a general introduction to London Gold and Silver Contracts for Differences (CFDs) issued by IBKR.

Please follow these links for information on IBKR Share CFDs, Index CFDs and Forex CFDs.

Risk Warning

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage.

61% of retail investor accounts lose money when trading CFDs with IBKR.

You should consider whether you understand how CFDs work and whether you can afford to take the

high risk of losing your money.

ESMA Rules for CFDs (Retail Clients only)

The European Securities and Markets Authority (ESMA) has enacted new CFD rules effective 1st August

2018.

The rules include: 1) leverage limits on the opening of a CFD position; 2) a margin close out rule on a per

account basis; and 3) negative balance protection on a per account basis.

The ESMA Decision is only applicable to retail clients. Professional clients are unaffected.

Please refer to the following articles for more detail:

ESMA CFD Rules Implementation at IBKR (UK) and IBKR LLC

ESMA CFD Rules Implementation at IBIE and IBCE

Introduction

A London Gold CFD enables you to have exposure to price movements of physical Gold without actually owning it. A London Gold CFD is an agreement between you and IBKR to exchange the difference in price of the underlying over a period of time. The difference to be exchanged is determined by the change in the reference price of the underlying. Thus, if the price of physical Gold traded on the London bullion market rises and you are long the CFD, you receive cash from IBKR and vice versa. A London Gold CFD can be bought long or sold short to suit your view of market direction in the future.

Contract Specifications

| Contract | IBKR Symbol | Per Trade Fee | Minimum per Order | Multiplier |

| London Gold | XAUUSD | 0.015% | USD 2.00 | 1 |

| London Silver | XAGUSD | 0.03% | USD 2.00 | 1 |

Price Determination

The IBKR London Gold and Silver CFDs reference physical Gold and Silver traded on the London bullion market. The London bullion market is a wholesale over-the-counter market for the trading of precious metals. Trading is conducted among members of the London Bullion Market Association (LBMA). Most of the members are major international banks.

IBKR receives quote streams from approximately 10 such major banks, in much the same way it does for cash forex. IBKR Smart routes between the banks, and the best available price at any given time becomes the reference price for the CFDs. IBKR does not add a spread to the banks’ quotes.

Low Commissions and Financing Rates: Unlike other CFD providers IBKR charges a transparent

commission, rather than widening the spread. Commission rates are only 0.015% for London Gold and 0.03% for London Silver. Overnight financing rates are just benchmark +/- 1.5% (an additional 1% surcharge is added for retail accounts).

Transparent Quotes: Because IBKR does not widen the spread, the Metals CFD quotes accurately

represent the spreads and price movements of the related cash metal, as described above.

Margin Efficiency: IBKR establishes house-margin requirements based on historic volatility of the

underlying and other factors. Retail clients are subject to regulatory minimum initial margins of 5% for

London Gold or 10% for London Silver.

Trading Permissions: Same as for Share and Index CFDs.

Market Data Permissions: Metals CFD market data is free, but a permission is required for system

reasons.

Worked Trade Example (Professional Clients):

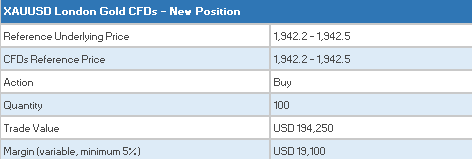

You purchase 100 XAUUSD CFDs at $1,942.5 for USD 194,250 which you then hold for 5 days.

![]()

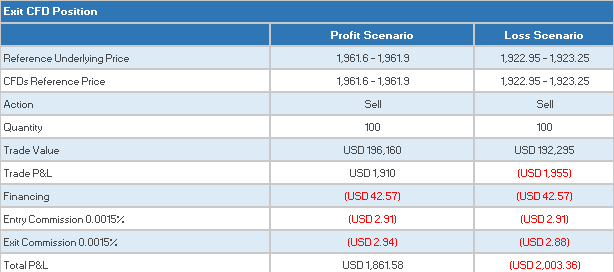

Closing the Position

CFD Resources

Below are some useful links with more detailed information on IB’s CFD offering:

Frequently asked Questions

Are short Metals CFDs subject to forced buy-in?

No.

Can I take delivery of the underlying metal?

No, IBKR does not support physical delivery for Metals CFDs.

Are there any market data requirements?

The market data for Metal CFDs is free, and is included the market data for Index CFDs. However, you need to subscribe to the permission for system reasons. To do this, log into Account Management, and click through the following tabs: Settings/User Settings/Trading Platform/Market Data Subscriptions. Alternatively you can set up an Index or Metals CFD in your TWS quote monitor and click the “Market Data Subscription Manager” button that appears on the quote line.

How are my CFD trades and positions reflected in my statements?

If you are a client of IBKR (U.K.) or IBKR LLC, your CFD positions are held in a separate account segment identified by your primary account number with the suffix “F”. You can choose to view Activity Statements for the F-segment either separately or consolidated with your main account. You can make the choice in the statement window in Account Management.

If you are a client of other IBKR entities, there is no separate segment. You can view your positions normally alongside your non-CFD positions.

In what type of IB accounts can I trade CFDs e.g., Individual, Friends and Family,

Institutional, etc.?

All margin and cash accounts are eligible for CFD trading.

Can I trade CFDs over the phone?

No. In exceptional cases we may agree to process closing orders over the phone, but never opening

orders.

Can anyone trade IB CFDs?

All clients can trade IB CFDs, except residents of the USA, Canada, Hong Kong, New Zealand and

Israel. There are no exemptions based on investor type to the residency-based exclusions.

Bonus Certificates Tutorial

Introduction

Bonus certificates are designed to provide a predictable return in sideways markets, and market returns in rising markets.

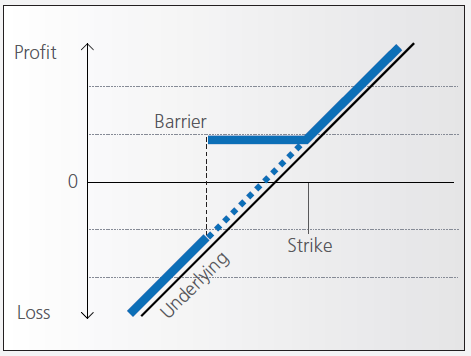

At the time they’re issued, bonus certificates normally have a term to maturity of two to four years. You will receive a specified cash pay-out (“bonus level” or “Strike”) if at maturity the price of the underlying is below or at the strike, as long as the underlying instrument has not touched or fallen below an established price level (“safety threshold” or “barrier”) during the term of the certificate.

Unless the certificate has a cap, you continue to participate in the price gains if the underlying instrument rises above the bonus level. In this case you either receive the corresponding number of shares or a cash settlement reflecting the value of the underlying instrument on the maturity date.

However, if the barrier is breached, you will no longer be entitled to the bonus payment. The value of the certificate then corresponds to the value of the underlying (times the ratio). In other words, once the barrier has been touched the certificate effectively converts to an index certificate. You will receive either the corresponding number of shares or a cash settlement reflecting the value of the underlying instrument on the maturity date.

Although there is no structured leverage, the presence of the barrier creates effective leverage. When the price of the underlying instrument approaches the barrier the probability of a breach increases, affecting the price of the certificate disproportionately.

Pay-out Profile

Example

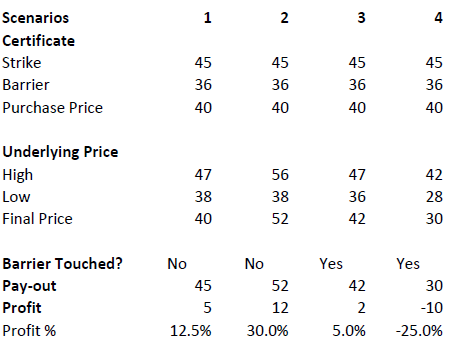

Assume a bonus certificate on ABC share. The certificate has a strike of EUR 45.00 and a barrier set at EUR 36.00. The table below shows scenarios depending on the trading range of the underlying, the final price of the underlying and whether the barrier has been touched or not.

Warrant Tutorial

Introduction

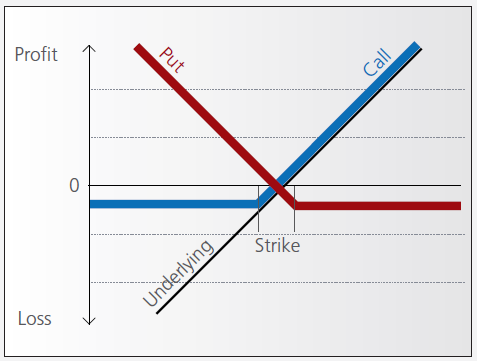

A warrant confers the right to buy (call-warrant) or sell (put-warrant) a specific quantity of a specific underlying instrument at a specific price over a specific period of time.

Pay-out Profile

With some warrants, the option right can only be exercised on the expiration date. These are referred to as “European-style” warrants. With “American-style” warrants, the option right can be exercised at any time prior to expiration. The vast majority of listed warrants are cash-exercised, meaning that you cannot exercise the warrant to obtain the underlying physical share. The exception to this rule is Switzerland, where physically settled warrants are widely available.

IBKR does allow for US and Canadian warrant exercise. Customers wishing to do so should submit a Customer Service ticket stating the name/symbol of the warrant, the quantity of shares and the intended action (i.e. exercise). The broker will pass through all associated exercise costs to the customer upon completion of the request. US or Canadian warrants are not eligible for auto-exercise at expiration. Warrants remaining in an account at expiration will be removed as worthless.

Factors that influence pricing

Not only do changes in the price of the underlying instrument influence the value of a warrant, a number of other factors are also involved. Of particular importance to investors in this regard are changes in volatility, i.e. the degree to which the price of the underlying instrument fluctuates. In addition, changes in interest rates and the anticipated dividend payments on the underlying instrument also play a role.

However, changes in implied volatility - as well as interest rates and dividends - only affect the time value of a warrant. The primary driver - intrinsic value - is solely determined by the difference between the price of the underlying instrument and the specified exercise price.

Historical and implied volatility

In addressing this topic, a differentiation has to be made between historical and implied volatility. Implied volatility reflects the volatility market participants expect to see in the financial instrument in the days and months ahead. If implied volatility for the underlying instrument increases, so does the price of the warrant.

This is because the probability of profiting from a warrant during a particular time-frame increases if the price of the underlying instrument is highly volatile. The warrant is therefore more valuable.

Conversely, if implied volatility decreases, that leads to a decline in the value of warrants and hence occasionally to nasty surprises for warrant investors who aren’t familiar with the concept and influence of volatility.

Interest rates and dividends

Issuers hedge themselves against price changes in the warrant through purchases and sales of the underlying instrument. Due to the leverage afforded by warrants, the issuer needs considerably more capital to hedge its exposure than you require to buy the warrants. The issuer’s interest expense associated with that capital is included in the price of the warrant. The amount of embedded interest reduces over time and at expiration is zero.

In the case of puts, the situation is exactly the opposite. Here, the issuer sells the underlying instrument

short to establish the necessary hedge, and in so doing receives capital that can earn interest. Thus interest reduces the price of the warrant by an amount that decreases over time.

As the issuer owns shares as a part of its hedging operations, it is entitled to receive the related dividend

payments. That additional income reduces the price of call warrants and increases the price for puts. But if the dividend expectations change, that will have an influence on the price of the warrants. Unanticipated special dividends on the underlying instrument can lead to a price decline in the related warrants.

Key valuation factors

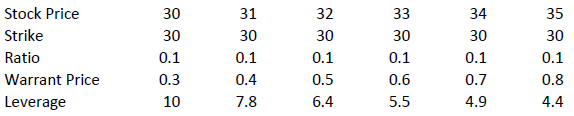

Let’s assume the following warrant:

Warrant Type: Call

Term to expiration: 2 years

Underlying : ABC Share

Share price: EUR 30.00

Strike: EUR 30.00

Exercise ratio: 0.1

Warrant’s price: EUR 0.30

Intrinsic value

Intrinsic value represents the amount you could receive if you exercised the warrant immediately and then bought (in the case of a call) or sold (put) the underlying instrument in the open market.

It’s very easy to calculate the intrinsic value of a warrant. In our example the intrinsic value is EUR 00.00

and is calculated as follows:

(price of underlying instrument – strike price) x exercise ratio

= (EUR 30.00 – EUR 30.00) x 0.1

= EUR 00.00

If the price of the ABC share increases by EUR 1, the intrinsic value becomes

= (EUR 31.00 – EUR 30.00) x 0.1

= EUR 00.10

The intrinsic value of a put warrant is calculated with this formula:

(strike price – price of underlying instrument) x exercise ratio

It’s important to note that the intrinsic value of a warrant can never be negative. By way of explanation:

if the price of the underlying instrument is at or below the exercise price, the intrinsic value of a call equals zero. In this instance, the price of the warrant consists only of “time value”. On the flipside, the intrinsic value of a put is equal to zero if the price of the underlying instrument is at or above the exercise price.

Time value

Once you’ve calculated the intrinsic value of a warrant, it’s also easy to figure out what the time value of that warrant is. You simply deduct the intrinsic value from the current market price of the warrant. In our example, the time value is equal to EUR 1.30 as you can see from the following calculation:

(warrant price – intrinsic value)

= (EUR 0.30 EUR – EUR 0.00)

= EUR 0.30

Time value gradually erodes during the term of a warrant and ultimately ends up at zero upon expiration. At that point, warrants with no intrinsic value expire worthless. Otherwise you can expect to receive payment of the intrinsic value. Take note, though: a warrant’s loss of time value accelerates during the final months of its term.

Premium

The premium indicates how much more expensive a purchase/sale of the underlying instrument would be via the purchase of a warrant and the immediate exercise of the option right as opposed to simply buying/selling the underlying instrument in the open market.

Hence the premium is a measure of how expensive a warrant actually is. It follows that, when given a choice between warrants with similar features, you should always buy the one with the lowest premium. By calculating the premium as an annualized percentage, warrants with different terms to expiry can be compared with each other.

The percentage premium for the call warrant in our example can be calculated as follows:

(strike price + warrant price / exercise ratio – share price) / share price * 100

= (EUR 30.00 + EUR 0.30 / 0.1 – EUR 30.00) / EUR 30.00 x 100

= 10 percent

Leverage

The amount of leverage is the price of the share * ratio divided by the price of the warrant. In our example 30.00*0.1/0.3 = 10. So when the price of ABC increases by 1% the value of the warrant increases by 10%.

The amount of leverage is not constant however; it varies as intrinsic and time value changes, and is particularly sensitive to changes in intrinsic value. As a rule of thumb, the higher the intrinsic value of the warrant, the lower the leverage. For example (assuming constant time value):

Knock-out (Turbo) Tutorial

Introduction

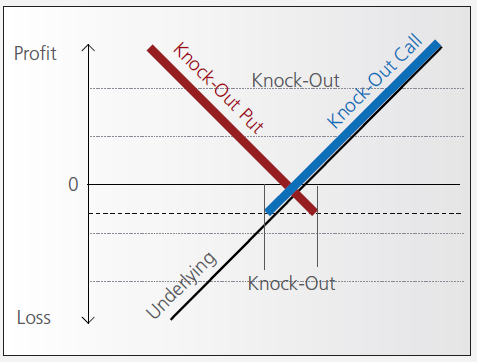

Knock-out warrants (turbos), like vanilla warrants, derive their value from the difference between the price of the underlying and the strike. They differ significantly however from vanilla warrants in many important respects:

- They can expire (knock-out) prematurely if the price of the underlying instrument touches or falls below (in the case of knock-out calls) or exceeds (in the case of knockout puts) a predetermined barrier-level. It expires worthless if the barrier equals the strike, or it may have a residual stop-loss value if the barrier is set higher than the strike (in the case of a call).

- Changes in implied volatility have little or no impact on knock-out products, therefore their pricing is easier for investors to comprehend than that of warrants.

- They have little or no time value (because of the presence of the knock-out barrier), and therefore have a higher degree of leverage than a warrant with the same strike. This is because the absence of time value makes the instrument “cheaper”.

Pay-out Profile

Leverage

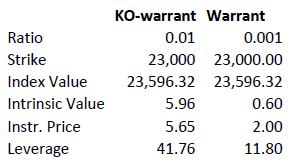

As discussed above, knock-out warrants exhibit high degrees of leverage, particularly as the price of the underlying nears the strike/barrier. Consider the following example of a long turbo on the Dow Jones Index, compared to a vanilla warrant:

Intrinsic value = (index value – strike) x ratio

Leverage = Index Value x Ratio / Instrument Price

A vanilla warrant retains significant time value even as the underlying price approaches the strike, sharply reducing its leverage compared to a knock-out warrant.

Product types

As discussed above, the barrier may either equal the strike, or be set above (calls) or below (puts). In the latter cases a small residual value remains after knock-out, corresponding to the difference between the barrier (the stop-loss level) and the strike.

Moreover, knock-out products may either have an expiration date or may be open-ended. This makes a difference in the way interest is accounted for. If the contract has an expiration date interest is included in the premium, the amount of which reduces over time and is zero on expiration. This is analogous to a standard vanilla warrant.

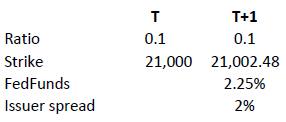

in relation to an expiration date. The price of the contract therefore corresponds exactly to its intrinsic value. Interest however must be accounted for. This is done by a daily adjustment of the barrier and strike. The following example shows the daily adjustment for a long open-end turbo on the Dow Jones Index:

The adjustment = Strike T x (1+ FedFunds/360 + Issuer Spread/360).

The intrinsic value of the instrument is correspondingly reduced as follows, assuming no change in the value of the DJ Index):

Intrinsic value = (index value – strike) x ratio

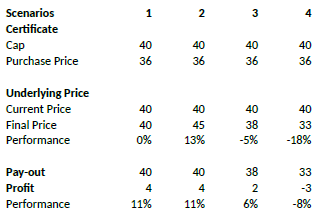

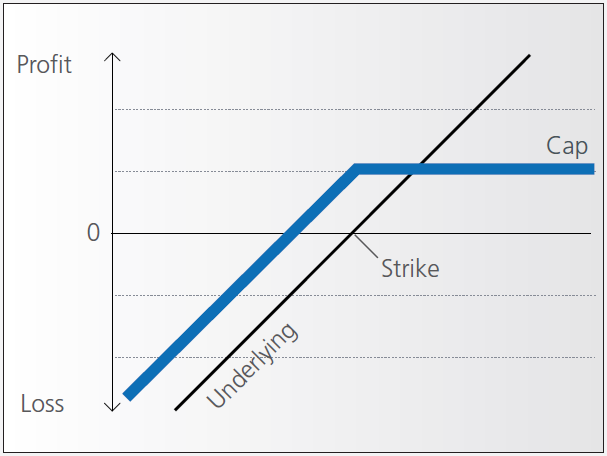

Discount Certificates Tutorial

Introduction

Discount certificates are designed to provide an enhanced return in sideways markets, compared to a direct investment in the underlying.

Discount certificates make it possible for you to buy an underlying instrument for less than its current market price. However, the maximum payback on a discount certificate is limited to a predetermined amount (cap).

Discount certificates normally have a term to maturity of one to three years. At maturity, a determination is made of where the price of the underlying instrument stands.

If it is at or above the cap, you’ll earn the maximum return and receive payment of the amount reflected by the cap.

If the price of the underlying instrument is below the cap on the maturity date, you’ll receive either the corresponding number of shares or a cash settlement reflecting the value of the underlying instrument on the maturity date.

Pay-out Profile

Example

Assume a discount certificate on ABC share. The certificate has a cap of EUR 40.00, and a purchase price of EUR 36.00. The table below shows scenarios depending on the final price of the underlying.