Automatic Forex Swap

OVERVIEW

In general, interest on account balances are credited/debited at benchmark rates plus/minus a spread as shown on our web pages. For qualified clients with substantial forex positions, however, IB has created a mechanism to carry large gross FX positions with higher efficiency with respect to carrying costs. We refer to it as the “auto swap program”. The design allows clients to benefit from IB’s participation in the interbank forex swaps market where implied interest rate spreads are usually much narrower than the spreads available in the retail deposit market.

a. Concept

Interest is charged on settled balances, so the intent of a Forex swap as used here is to defer the settlement of a currency position from one day to the next business day. This is done by a simultaneous sell and buy of the same amount of base (first) currency but for two different value dates e.g. on T you go long 10 mio. EUR.USD for value date T+2. By example, on T+1 the position is swapped T+2 to T+3, here a sell of 10 mio EUR.USD for T+2 and a purchase of 10 mio. EUR.USD for T+3. As a result you have deferred settlement from T+2 to T+3, with the difference in prices of the two trades representing the financing cost from T+2 to T+3.

b. Cost

This service is provided as a free service and no commission or markup is charged by Interactive Brokers. The interbank market bid/ask spread inherent in the swap prices may be regarded as a cost but is not determined by Interactive Brokers. Interactive Brokers provides the service on a best efforts basis to our large Forex clients.

c. Position Criteria

Swap activity is only applied to accounts with gross FX positions larger than 10 mio. USD or approximate equivalent of other currencies. Positions are swapped (rolled) in increments or multiples of USD 1 mio. (or equivalent). The residual settled balances are traded under IB‘s standard interest model1. Positions that are swapped (rolled) are real positions, i.e. the projected T+1 settled cash balances.

The so-called “Virtual Positions” are not considered; the virtual position is only a representation of the original trades expressed as currency pairs, for example EUR.CHF.

Settled cash balances are a single currency concept, e.g. EUR or CNH. IB executes all swaps against USD as it is the most efficient funding currency. Should you have a position in a cross, e.g. EUR against CHF, two swaps, one in EUR.USD and one in USD.CHF will be done. The threshold(s) and increment(s) may change at any time without notice.

d. Client Eligibility

As we offer this service for free, only clients with substantial currency positions are eligible for inclusion in the service. US legal residents need to be an Eligible Contract Participant (ECP) and be in the possession of an LEI number (legal entity identifier). Interactive Brokers cannot guarantee a client’s inclusion in the program and all inquiries require compliance approval prior to become active.2

e. Swap Price Recognition

Interactive Brokers may conduct a series of swaps in a currency during a day. Interactive Brokers will use average bid and ask prices at which it executed, respectively average bid and asks as quoted in the interbank market. Swap prices are not published but can be seen (or calculated) in the statement after execution. The swaps are applied in the account at the end of the day.

f. Recognition in the Statement

You will find the swap transaction(s) in the Trades section of the statement. The swap are represented as simultaneous purchase/sale or vice versa, do not have a time stamp and shows an M (manual entry) in the code column. The actual swap prices are the difference in between the two prices.

Here an example for cob 20150203 that shows a swap from 20150203 to 20150204.

![]()

.jpg)

g. Examples of Swap Prices

Here a couple of examples that use swap prices from a major interbank provider. Often bid/ask spreads are even tighter.

|

Currency Pair |

Spot Bid |

Spot Ask |

Tenor |

Days in Period (TN) |

Swap Points Bid |

Swap Points Ask |

Implied Currency |

Implied Rate Bid |

Implied Rate Ask |

|

EUR.USD |

1.04481 |

1.04483 |

TomNext(TN) |

1 |

0.00004220 |

0.00004280 |

EUR |

-0.77% |

-0.75% |

|

USD.HKD |

7.76810 |

7.76810 |

TomNext(TN) |

1 |

-0.00011500 |

-0.00011000 |

HKD |

0.17% |

0.19% |

|

USD.JPY |

117.050 |

117.052 |

TomNext(TN) |

1 |

-0.0038 |

-0.0032 |

JPY |

-0.47% |

-0.47% |

|

USD.CNH |

6.93101 |

6.93105 |

TomNext(TN) |

1 |

0.0021 |

0.0028 |

CNH |

11.77% |

15.46% |

In more detail, let’s assume you want to calculate the implied CNH rate resulting from a USD.CNH swap. We are looking for the implied rate of the quote currency CNH (Currency 2). Therefore the following formula is used:

| Description | Variable | Value |

| Currency Pair (Currency1.Currency2) | USD.CNH | |

| day count convention Currency 1 (base Currency), i.e. USD | dayCountCurr1 | 360 |

| day count convention Currency 2 (quote Currency), i.e. CNH | dayCountCurr2 | 365 |

| Tenor | TomNext | |

| number of days in the Tenor | noDays | 1 |

| interest rate of Currency 1 (in decimals, i.e. 1% = 0.01) | inRateCurr1 | 0.0070 |

| Currency rate (Spot) | currencyRate | 6.939500 |

| swap Points expressed in decimals | swapPoints | 0.0012 |

| near Currency Rate (Spot - swap points) | nearCurrencyRate | 6.938300 |

| far Currency Rate (in a Tomnext swap this is the spot rate) | farCurrencyRate | 6.939500 |

| implied interes rate of Currency2, i.e. CNH | impliedRateCurrncy2(quoteCurrency) | 0.0702 |

So using above figures, this results in a 7.02% implied interest rate for CNH.

Now if you wanted to calculate the implied rate for the base currency (Currency 1) the formula would change slightly. Here an example using EUR.USD:

| Description | Variable | Value |

| Currency Pair (Currency1.Currency2) | EUR.USD | |

| day count convention Currency 1 (base Currency), i.e. EUR | dayCountCurr1 | 360 |

| day count convention Currency 2 (quote Currency), i.e. USD | dayCountCurr2 | 360 |

| Tenor | TomNext | |

| number of days in the Tenor | noDays | 1 |

| interest rate of Currency 2 (in decimals, i.e. 1% = 0.01) | inRateCurr2 | 0.0070 |

| Currency rate (Spot) | currencyRate | 1.039900 |

| swap Points expressed in decimals | swapPoints | 0.000042 |

| near Currency Rate (Spot - swap points) | nearCurrencyRate | 1.039858 |

| far Currency Rate (in a Tomnext swap this is the spot rate) | farCurrencyRate | 1.039900 |

| implied interes rate of Currency1, i.e. EUR | impliedRateCurrncy1(baseCurrency) | -0.0075 |

Using above example, this results in a -0.75 % implied interest rate for EUR.

1. For example, in the case of a USD 20.3 mio. position only 20 mio. will be swapped. USD 0.3 remains in the account and interest using benchmark and spreads will be applied. A USD 300k position will not be considered for swapping at all. The position by currency is taken as the reference, regardless of the overall position.

2 US, Australian and Israeli domiciled residents are currently not eligible for inclusion in the Automated Forex Swap Program.

Summary of Risks relating to Forex CFDs issued by Interactive Brokers Securities Japan, Inc.

Übersicht:

This summary highlights the principal risks associated with trading Forex CFDs issued by IBSJ (“IB FXCFDs"). It is not a risk disclosure for regulatory purposes.

- Trading of IB FXCFDs is not suitable for all investors, and you should not trade them unless you are an experienced investor with a high risk tolerance and the capability to sustain losses if they occur

- The volatility of foreign exchange rates and interest rates may quickly cause significant losses. Forex CFDs employ leverage that further amplifies the volatility relative to your investment and you may lose more than you have invested. In addition, IB FXCFD roll over interest may turn from a credit to a debit due to changes in interest rates

- You are required to maintain sufficient equity in your account at all times to cover IBSJs maintenance margin requirement. There are no grace-periods and IBSJ does not issue margin calls. Your equity is calculated in real time and should it become insufficient, IBSJ will immediately and automatically liquidate positions to bring your account into margin compliance. Real time liquidations aim to minimize the risk that your account equity becomes negative, but they cannot eliminate that risk. Should your equity become negative you are required to deposit additional funds to cover the deficit

- The price IBSJ displays to you for IB FXCFDs is based on the prevailing foreign exchange market. However there is no guarantee for executions at that price. Slippage may occur for large trades or in fast moving markets and during heavily traded hours

- Moreover, your ability to establish or close positions on a timely basis is not guaranteed. It may become difficult to display quotes during major holidays or during hours when foreign exchange trading is not active. IBSJ may display prices that deviate from a fair market due to system-malfunctions or failures, or erroneous quotes that IBSJ may receive from market participants or for other reasons (off-market prices). IBSJ will adjust or cancel trades executed with off-market prices

- IB FXCFDs are over-the-counter trades between you and IBSJ. They are not traded on any exchange or cleared by any central counterparty. You are therefore exposed to counterparty risk and should IBSJ become insolvent you may not be able to fully recoup your investment, or at all

Please contact IBSJs Client Service Department should you have questions about the content of this summary and read the full risk disclosure carefully before commencing trading. The risk disclosure is available in Account Management when you request IB FXCFD trading permissions, and on IBSJs web site.

IBKR-Forex-CFDs - Fakten, Fragen und Antworten

Übersicht:

Der nachfolgende Artikel gewährt einen allgemeinen Überblick zu Differenzkontrakten (CFDs) auf Forexbasis, die von IB UK ausgegeben werden.

IB-Forex-CFDs sind für dieselben 85 Währungspaare verfügbar, die IB für Spot-FX anbietet. Die günstigen Provisionen und Marginsätze sind ebenfalls identisch. Allerdings zeichnen sich Forex-CFDs durch ein äußerst wettbewerbsfähiges Finanzierungsmodell im Kontraktstil aus, wie nachstehend erläutert.

Risikowarnhinweis

Bei CFDs handelt es sich um komplexe Instrumente, die mit einem hohen Risiko des Geldverlusts aufgrund von Hebeleffekten einhergehen.

67% an Privatanlegern verlieren beim CFD-Handel mit IBKR (UK) Geld.

Bitte überlegen Sie sich, ob Sie wissen, wie CFDs funktionieren und ob Sie das hohe Risikopotenzial, Ihre Anlage zu verlieren, tragen können.

ESMA-Regeln für CFDs (betreffen ausschließlich Privatkunden)

Zum 1. August 2018 hat die Europäische Wertpapier- und Marktaufsichtsbehörde (ESMA) neue CFD-Regeln eingeführt.

Die Regeln umfassen: 1) Leverage-Limits zur Eröffnung einer CFD-Position; 2) Margin-Glattstellungsregel auf einer Pro-Konto-Basis sowie 3) Negativkapitalschutz auf einer Pro-Konto-Basis. Die Entscheidung der ESMA betrifft ausschließlich Privatkunden.

Professionelle Kunden sind davon nicht betroffen.

Siehe Einführung der ESMA-CFD-Regeln bei IBKR für weitere Details.

Forex-CFD-Funktionen bei IBKR

Transparente DMA-Kursnotierungen: IB bietet enge Spreads und starke Liquidität an. Dies ist dank der Kombination von Kursnotierungsstreams 14 weltweit führender Forex-Dealer möglich, die zusammen einen Marktanteil von über 70% des weltweiten Interbankenmarkts halten.* Hierdurch werden Kursnotierungen mit einer Genauigkeit von mitunter nur 0.1 PIP angezeigt. IB erhöht die Kursnotierungen nicht durch Aufschläge, sondern gibt die Kurse so weiter, wie sie von den Forex-Anbietern eingehen, und erhebt separat eine geringe Provision.

*Quelle: Euromoney FX Survey FX Poll 2016.

Haltezinsen: Die Verlängerung von Forex-CFDs erfolgt auf Basis der Differenz zwischen den Referenzzinssätzen der beiden Währungen des jeweiligen Währungspaares. Dies ähnelt prinzipiell der TOM-Next-Rollover-Methode, die von anderen Brokern verwendet wird, bietet aber ein höheres Maß an Stabilität, da die Referenzzinssätze in der Regel weniger schwankungsanfällig sind als Swap-Sätze. Zusätzlich erhebt IB einen geringen Finanzierungsspread, der bei den gängigsten Währungspaaren schon bei 1.0% ansetzt und bei großen Salden bis auf 0.5% sinken kann. Für volatilere Währungspaare gelten höhere Finanzierungsspreads.

Die Haltezinsen für IB-Forex-CFDs basieren auf einen Währungspaar-spezifischen Benchmarkwert und einem Spread. Der Benchmarkwert entspricht der Differenz zwischen den IB-Benchmarkzinssätzen für die beiden Währungen. Dieser Wert wird anhand der Formel + BM der Basiswährung - BM der Zielwährung berechnet.

Beispiel: Am 21. April 2016 lag der GBP-Referenzzins bei 0.483% und der USD-Referenzzins bei 0.37%. Der anwendbare Benchmarksatz ist:

GBP.USD BM + 0.48% - 0.37% = +0.113%

Der anzuwendende Zinssatz für den Kunden entspricht dem BM-Satz für das Währungspaar - dem IB-Spread für Long-Positionen oder + dem Spread für Short-Positionen:

GBP.USD Long-Satz +0.113% - 1.00% = -0.887%

GBP.USD Short-Satz +0.113% + 1.00% = +1.113%

Bitte beachten Sie, dass der Long-Zinssatz als Habenzins und der Short-Zinssatz als Sollzins angewendet wird. Folglich entspricht ein positiver Zinssatzwert auf eine Long-Position einer Zinsgutschrift, während ein negativer Zinssatz eine Zinsbelastung bedeutet. Bei Short-Positionen bedeutet ein positiver Zinssatz eine Zinsbelastung, während ein negativer Satz einer Zinsgutschrift entspricht.

Die Zinsen werden auf den Kontraktwert in der Zielwährung berechnet und in dieser Währung gutgeschrieben bzw. in Rechnung gestellt. Beispiele:

Beispiele:

| Tägliche Zinsen | |||||

|---|---|---|---|---|---|

| Position | Schlusskurs GBP.USD | USD-Wert | Gebühr | USD | |

| GBP.USD | -20,000 | 1.43232 | -28,646.40 | 1.113% | -0.89 |

Zinsen auf Forex-CFD-Salden werden auf Einzelkontraktbasis berechnet und nicht mit anderen Währungspositionen, inkl. Spot-FX, kombiniert oder verrechnet. IB verwendet zwar keine direkte Referenz für Swap-Sätze, behält sich aber das Recht vor, bei außerordentlichen Marktbedingungen höhere Spreads anzuwenden, z. B. während Spitzenphasen der Swap-Sätze, die zum Ende des Finanzjahres eintreten können.

Ausführliche Zinstabellen finden Sie hier.

Trading: IB-Forex-CFDs werden genau wie Spot-FX gehandelt und es steht dieselbe Auswahl aus mehr als 20 Ordertypen und Algorithmen zur Auswahl. IB-Forex-CFDs können entweder über die klassische TWS oder über den IB FX Trader gehandelt werden. Um Ihren gewünschten Kontrakt in der klassischen TWS oder dem FX Trader zu finden, können Sie einfach das Währungspaar (z. B. EUR.USD) eingeben und dann im Kontraktauswahl-Pop-Up den CFD auswählen.

Margin: Die Margin-Anforderungen für IB-Forex-CFDs werden für jedes Währungspaar pro Kontrakt ermittelt, ohne

Berücksichtigung anderer im Konto gehaltener Forex-Salden, inkl. Spot-FX. Bei den gängigsten Währungspaaren beginnen die Marginsätze bereits bei günstigen 2.5% des Kontraktwerts. Details zu allen Währungspaaren finden Sie hier. In Abhängigkeit des Währungspaares unterliegen Privatkunden einem regulatorischen Ersteinschuss von mindestens 3.33% oder 5%. Siehe Einführung der ESMA-CFD-Regeln bei IBKR für weitere Details.

Provisionen: IB zeigt die Kurse so an, wie sie von den Forex-Anbietern eingehen, und erhebt separat eine geringe Provision.

Diese Methode haben wir gewählt, um eine möglichst transparente Gebührenstruktur anzubieten, anstatt unsere Kursnotierungen mit Aufschlägen zu versehen und dafür keine Provisionen zu berechnen, wie es bei vielen anderen Forex-Brokern üblich ist. Die Provisionen werden in Abhängigkeit von dem monatlich gehandelten Wert gestaffelt und liegen zwischen 0.20 Basispunkten und 0.08 Basispunkten. Bei der Ermittlung der Staffelungsstufe werden sowohl Forex-CFD-Volumina als auch Spot-FX-Volumina berücksichtigt.

Weitere Einzelheiten finden Sie hier.

Handelsberechtigungen: Für den Handel mit Forex-CFDs müssen Sie die entsprechenden Forex-CFD-Berechtigungen in der Kontoverwaltung einrichten. Es gelten dieselben Eignungskriterien wie für den gehebelten FX-Handel. Bitte beachten Sie, dass Forex-CFDs - ebenso wie andere CFDs - durch IB UK gehalten werden. Falls Sie über ein Konto bei IB LLC verfügen, werden sie in diesem Zusammenhang daher aufgefordert, ein Kontosegment bei IB UK zu eröffnen. Das IB-UK-Kontosegment wird durch Ihre Kontonummer plus dem Anhängsel „F“ gekennzeichnet.

Beispiel einer Transaktion (Professionelle Kunden)

Eröffnung der Position

Sie kaufen 10 Lots (200000) EUR.CHF CFDs zu $1.16195 für 232,390 CHF und halten die Position für 5 Tage.

| EUR.CHF-Forex-CFDs – Neue Position | |

|---|---|

| Referenzkurs des Basiswerts | 1.16188 - 1.16195 |

| CFD-Referenzkurs | 1.16188 - 1.16195 |

| Aktion | Kauf |

| Menge | 200,000 |

| Handelswert | 232,390.00 CHF |

| Margin (3% x 232,390) | 9,100 AUD |

| Soll-Zinsen (auf 232,390 CHF über 5 Tage) | |||

|---|---|---|---|

| Stufe I (Paar BM 0.42% - IB-Spread 1%) | 232,390.00 CHF | -0.58% | (18.72 CHF) |

Schließung der Position

| Verlassen der CFD-Position | ||

|---|---|---|

| Gewinn-Szenario | Verlust-Szenario | |

| Referenzkurs des Basiswerts | 1.16840 - 1.16848 | 1.15539 - 1.15546 |

| CFD-Referenzkurs | 1.16840 - 1.16848 | 1.15539 - 1.15546 |

| Aktion | Verkauf | Verkauf |

| Menge | 200,000 | 200,000 |

| Handelswert | 233,680.00 CHF | 231,078.00 CHF |

| Handels-G&V | 1,290.00 CHF | (1,312.00 CHF) |

| Finanzierung | (18.72 CHF) | (18.72 CHF) |

| Einstiegsprovision 0.002% | (4.65 CHF) | (4.65 CHF) |

| Einstiegsprovision 0.002% | (4.67 CHF) | (4.62 CHF) |

| Gesamt-G&V | 1,261.96 CHF | (1,339.99 CHF) |

Informationsquellen zu CFDs

Nachstehend sind einige hilfreiche Links aufgeführt, über die Sie sich weitere Informationen zum CFD-Angebot von IB ansehen können:

Häufig gestellte Fragen

Ist der Handel mit IB-Forex-CFDs für jeden Kunden möglich?

Alle Kunden, außer solchen mit Sitz in den USA, Kanada und Hongkong, können mit IB-CFDs handeln. Es gibt keine Anlegertyp-basierten Ausnahmen für die Ausschlüsse auf Basis der Ansässigkeit.

Was ist der Unterschied zwischen IB-Forex-CFDs und IB Cash-Forex?

IB Cash-Forex bezeichnet eine gehebelte Forex-Transaktion, bei der Sie beide Währungen des Währungspaares aufnehmen. Ihre Salden aus dem Forex-Handel werden mit Ihren Salden aus anderen Handelsaktivitäten kombiniert und Sie zahlen oder erhalten Zinsen auf diese konsolidierten Salden auf Basis des Benchmark-Zinssatzes für jede der Währungen.

Im Gegensatz dazu ist ein IB-Forex-CFD ein Kontrakt, der es Ihnen ermöglicht, eine Position zu eröffnen, ohne dass Ihnen die zugrunde liegenden Währungen geliefert werden. Somit erhalten und zahlen Sie keine Zinsen auf den Nennbetrag des Kontrakts. Der Benchmark-Satz für den Kontrakt entspricht der Differenz zwischen den Referenzzinssätzen der zwei zugrunde liegenden Währungen. Dies ähnelt prinzipiell der TOM-Next-Rollover-Methode, die von anderen Brokern verwendet wird, bietet aber ein höheres Maß an Stabilität, da die Referenzzinssätze in der Regel weniger schwankungsanfällig sind als Swap-Sätze.

Ein ausführliches Beispiel finden Sie vorstehend im Abschnitt Haltezinsen.

Sind bestimmte Marktdaten erforderlich?

Die Marktdaten für IB-Forex-CFDs sind mit denen für den gehebelten FX-Handel identisch. Es handelt sich um eine globale Berechtigung, die kostenlos bereitgestellt wird.

Wie werden CFD-Transaktionen und -Positionen auf meinen Kontoauszügen dargestellt?

Falls Sie ein Konto besitzen, das bei IBLLC geführt wird, werden Ihre CFD-Positionen in einem separaten Kontosegment gehalten, das durch Ihre Hauptkontonummer mit dem angehängten Kürzel „F“ gekennzeichnet wird. Sie können sich Umsatzübersichten entweder separat für das F-Segment oder konsolidiert zusammen mit Ihrem Hauptkonto anzeigen lassen. Diese Auswahl können Sie in der Kontoverwaltung im Kontoauszugsfenster treffen.

Können beim Handel mit Forex-CFDs dieselben Ordertypen und Algorithmen genutzt werden wie für Spot-FX-Geschäfte, und können solche Geschäfte über den FX Trader durchgeführt werden?

Ja, das Trading-Erlebnis ist identisch.

Allocation of Partial Fills

How are executions allocated when an order receives a partial fill because an insufficient quantity is available to complete the allocation of shares/contracts to sub-accounts?

Overview:

From time-to-time, one may experience an allocation order which is partially executed and is canceled prior to being completed (i.e. market closes, contract expires, halts due to news, prices move in an unfavorable direction, etc.). In such cases, IB determines which customers (who were originally included in the order group and/or profile) will receive the executed shares/contracts. The methodology used by IB to impartially determine who receives the shares/contacts in the event of a partial fill is described in this article.

Background:

Before placing an order CTAs and FAs are given the ability to predetermine the method by which an execution is to be allocated amongst client accounts. They can do so by first creating a group (i.e. ratio/percentage) or profile (i.e. specific amount) wherein a distinct number of shares/contracts are specified per client account (i.e. pre-trade allocation). These amounts can be prearranged based on certain account values including the clients’ Net Liquidation Total, Available Equity, etc., or indicated prior to the order execution using Ratios, Percentages, etc. Each group and/or profile is generally created with the assumption that the order will be executed in full. However, as we will see, this is not always the case. Therefore, we are providing examples that describe and demonstrate the process used to allocate partial executions with pre-defined groups and/or profiles and how the allocations are determined.

Here is the list of allocation methods with brief descriptions about how they work.

· AvailableEquity

Use sub account’ available equality value as ratio.

· NetLiq

Use subaccount’ net liquidation value as ratio

· EqualQuantity

Same ratio for each account

· PctChange1:Portion of the allocation logic is in Trader Workstation (the initial calculation of the desired quantities per account).

· Profile

The ratio is prescribed by the user

· Inline Profile

The ratio is prescribed by the user.

· Model1:

Roughly speaking, we use each account NLV in the model as the desired ratio. It is possible to dynamically add (invest) or remove (divest) accounts to/from a model, which can change allocation of the existing orders.

Basic Examples:

Details:

CTA/FA has 3-clients with a predefined profile titled “XYZ commodities” for orders of 50 contracts which (upon execution) are allocated as follows:

Account (A) = 25 contracts

Account (B) = 15 contracts

Account (C) = 10 contracts

Example #1:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 10 am (ET) the order begins to execute2but in very small portions and over a very long period of time. At 2 pm (ET) the order is canceled prior to being executed in full. As a result, only a portion of the order is filled (i.e., 7 of the 50 contracts are filled or 14%). For each account the system initially allocates by rounding fractional amounts down to whole numbers:

Account (A) = 14% of 25 = 3.5 rounded down to 3

Account (B) = 14% of 15 = 2.1 rounded down to 2

Account (C) = 14% of 10 = 1.4 rounded down to 1

To Summarize:

A: initially receives 3 contracts, which is 3/25 of desired (fill ratio = 0.12)

B: initially receives 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: initially receives 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The system then allocates the next (and final) contract to an account with the smallest ratio (i.e. Account C which currently has a ratio of 0.10).

A: final allocation of 3 contracts, which is 3/25 of desired (fill ratio = 0.12)

B: final allocation of 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: final allocation of 2 contract, which is 2/10 of desired (fill ratio = 0.20)

The execution(s) received have now been allocated in full.

Example #2:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 11 am (ET) the order begins to be filled3 but in very small portions and over a very long period of time. At 1 pm (ET) the order is canceled prior being executed in full. As a result, only a portion of the order is executed (i.e., 5 of the 50 contracts are filled or 10%).For each account, the system initially allocates by rounding fractional amounts down to whole numbers:

Account (A) = 10% of 25 = 2.5 rounded down to 2

Account (B) = 10% of 15 = 1.5 rounded down to 1

Account (C) = 10% of 10 = 1 (no rounding necessary)

To Summarize:

A: initially receives 2 contracts, which is 2/25 of desired (fill ratio = 0.08)

B: initially receives 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: initially receives 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The system then allocates the next (and final) contract to an account with the smallest ratio (i.e. to Account B which currently has a ratio of 0.067).

A: final allocation of 2 contracts, which is 2/25 of desired (fill ratio = 0.08)

B: final allocation of 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: final allocation of 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The execution(s) received have now been allocated in full.

Example #3:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 11 am (ET) the order begins to be executed2 but in very small portions and over a very long period of time. At 12 pm (ET) the order is canceled prior to being executed in full. As a result, only a portion of the order is filled (i.e., 3 of the 50 contracts are filled or 6%). Normally the system initially allocates by rounding fractional amounts down to whole numbers, however for a fill size of less than 4 shares/contracts, IB first allocates based on the following random allocation methodology.

In this case, since the fill size is 3, we skip the rounding fractional amounts down.

For the first share/contract, all A, B and C have the same initial fill ratio and fill quantity, so we randomly pick an account and allocate this share/contract. The system randomly chose account A for allocation of the first share/contract.

To Summarize3:

A: initially receives 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: initially receives 0 contracts, which is 0/15 of desired (fill ratio = 0.00)

C: initially receives 0 contracts, which is 0/10 of desired (fill ratio = 0.00)

Next, the system will perform a random allocation amongst the remaining accounts (in this case accounts B & C, each with an equal probability) to determine who will receive the next share/contract.

The system randomly chose account B for allocation of the second share/contract.

A: 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: 0 contracts, which is 0/10 of desired (fill ratio = 0.00)

The system then allocates the final [3] share/contract to an account(s) with the smallest ratio (i.e. Account C which currently has a ratio of 0.00).

A: final allocation of 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: final allocation of 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: final allocation of 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The execution(s) received have now been allocated in full.

Available allocation Flags

Besides the allocation methods above, user can choose the following flags, which also influence the allocation:

· Strict per-account allocation.

For the initially submitted order if one or more subaccounts are rejected by the credit checking, we reject the whole order.

· “Close positions first”1.This is the default handling mode for all orders which close a position (whether or not they are also opening position on the other side or not). The calculation are slightly different and ensure that we do not start opening position for one account if another account still has a position to close, except in few more complex cases.

Other factor affects allocations:

1) Mutual Fund: the allocation has two steps. The first execution report is received before market open. We allocate based onMonetaryValue for buy order and MonetaryValueShares for sell order. Later, when second execution report which has the NetAssetValue comes, we do the final allocation based on first allocation report.

2) Allocate in Lot Size: if a user chooses (thru account config) to prefer whole-lot allocations for stocks, the calculations are more complex and will be described in the next version of this document.

3) Combo allocation1: we allocate combo trades as a unit, resulting in slightly different calculations.

4) Long/short split1: applied to orders for stocks, warrants or structured products. When allocating long sell orders, we only allocate to accounts which have long position: resulting in calculations being more complex.

5) For non-guaranteed smart combo: we do allocation by each leg instead of combo.

6) In case of trade bust or correction1: the allocations are adjusted using more complex logic.

7) Account exclusion1: Some subaccounts could be excluded from allocation for the following reasons, no trading permission, employee restriction, broker restriction, RejectIfOpening, prop account restrictions, dynamic size violation, MoneyMarketRules restriction for mutual fund. We do not allocate to excluded accountsand we cancel the order after other accounts are filled. In case of partial restriction (e.g. account is permitted to close but not to open, or account has enough excess liquidity only for a portion of the desired position).

Footnotes:

Additional Information Regarding the Use of Stop Orders

U.S. equity markets occasionally experience periods of extraordinary volatility and price dislocation. Sometimes these occurrences are prolonged and at other times they are of very short duration. Stop orders may play a role in contributing to downward price pressure and market volatility and may result in executions at prices very far from the trigger price.

Investors may use stop sell orders to help protect a profit position in the event the price of a stock declines or to limit a loss. In addition, investors with a short position may use stop buy orders to help limit losses in the event of price increases. However, because stop orders, once triggered, become market orders, investors immediately face the same risks inherent with market orders – particularly during volatile market conditions when orders may be executed at prices materially above or below expected prices.

While stop orders may be a useful tool for investors to help monitor the price of their positions, stop orders are not without potential risks. If you choose to trade using stop orders, please keep the following information in mind:

· Stop prices are not guaranteed execution prices. A “stop order” becomes a “market order” when the “stop price” is reached and the resulting order is required to be executed fully and promptly at the current market price. Therefore, the price at which a stop order ultimately is executed may be very different from the investor’s “stop price.” Accordingly, while a customer may receive a prompt execution of a stop order that becomes a market order, during volatile market conditions, the execution price may be significantly different from the stop price, if the market is moving rapidly.

· Stop orders may be triggered by a short-lived, dramatic price change. During periods of volatile market conditions, the price of a stock can move significantly in a short period of time and trigger an execution of a stop order (and the stock may later resume trading at its prior price level). Investors should understand that if their stop order is triggered under these circumstances, their order may be filled at an undesirable price, and the price may subsequently stabilize during the same trading day.

· Sell stop orders may exacerbate price declines during times of extreme volatility. The activation of sell stop orders may add downward price pressure on a security. If triggered during a precipitous price decline, a sell stop order also is more likely to result in an execution well below the stop price.

· Placing a “limit price” on a stop order may help manage some of these risks. A stop order with a “limit price” (a “stop limit” order) becomes a “limit order” when the stock reaches or exceeds the “stop price.” A “limit order” is an order to buy or sell a security for an amount no worse than a specific price (i.e., the “limit price”). By using a stop limit order instead of a regular stop order, a customer will receive additional certainty with respect to the price the customer receives for the stock. However, investors also should be aware that, because a sell order cannot be filled at a price that is lower (or a buy order for a price that is higher) than the limit price selected, there is the possibility that the order will not be filled at all. Customers should consider using limit orders in cases where they prioritize achieving a desired target price more than receiving an immediate execution irrespective of price.

· The risks inherent in stop orders may be higher during illiquid market hours or around the open and close when markets may be more volatile. This may be of heightened importance for illiquid stocks, which may become even harder to sell at the then current price level and may experience added price dislocation during times of extraordinary market volatility. Customers should consider restricting the time of day during which a stop order may be triggered to prevent stop orders from activating during illiquid market hours or around the open and close when markets may be more volatile, and consider using other order types during these periods.

· In light of the risks inherent in using stop orders, customers should carefully consider using other order types that may also be consistent with their trading needs.

IB Forex CFDs - Facts and Q&A

Übersicht:

The following article is intended to provide a general introduction to forex-based Contracts for Differences (CFDs) issued by IBKR.

IBKR Forex CFDs are available for the same 85 tradable currency pairs IBKR offers as Spot FX, with identical low commissions and margin rates. By contrast, Forex CFDs feature a contract-style highly competitive financing model detailed below.

Risk Warning

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage.

61% of retail investor accounts lose money when trading CFDs with IBKR.

You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

ESMA Rules for CFDs (Retail Clients only)

The European Securities and Markets Authority (ESMA) has enacted new CFD rules effective 1st August 2018.

The rules include: 1) leverage limits on the opening of a CFD position; 2) a margin close out rule on a per account basis; and 3) negative balance protection on a per account basis. The ESMA Decision is only applicable to retail clients.

Professional clients are unaffected.

Please refer to the following articles for more detail:

ESMA CFD Rules Implementation at IBKR (UK) and IBKR LLC

ESMA CFD Rules Implementation at IBIE and IBCE

IBKR Forex CFD Features

Transparent DMA Quotes: IBKR ensures tight spreads and substantial liquidity as a result of combining quotation streams from 14 of the world's largest foreign exchange dealers which constitute more than 70% of market share in the global interbank market*. This results in displayed quotes as small as 0.1 PIP. IBKR does not mark up the quotes, rather passes through the prices that it receives and charges a separate low commission.

*Source: Euromoney FX survey FX Poll 2016.

Carry Interest: Forex CFDs are rolled over reflecting the benchmark interest rate differential of the relevant currency pair. This is in principle similar to the TOM Next rolls used by other brokers, but offers greater stability as benchmark rates generally are less volatile than swap rates. In addition IBKR applies a low financing spread that for major pairs starts at just 1.0% and can be as low as 0.5% for large balances. More volatile pairs have higher financing spreads.

The carry interest for IBKR Forex CFDs is based on a currency-pair specific benchmark and a spread. The benchmark is the difference between the IBKR benchmark rates for the two currencies. It is calculated as + BM Base currency – BM Quote currency.

For example, April 21, 2016 the GBP benchmark rate was 0.483%, the USD rate was 0.37%. The applicable benchmark rate is:

GBP.USD BM +0.48% - 0.37% = +0.113%

The applicable customer rate is Pair BM – IBKR spread for long positions, BM + spread for short positions:

GBP.USD Long Rate +0.113% - 1.00% = -0.887%

GBP.USD Short Rate +0.113% + 1.00% = +1.113%

It is important to note that the long rate is applied as a credit, the short rate as a debit. Consequently for a long position a positive rate means a credit, a negative rate a charge. However for short positions a positive rate means a charge, a negative rate a credit.

Interest is calculated on the contract value expressed in the quote currency, and credited or debited in that currency. For example:

For example:

| Daily Interest | |||||

|---|---|---|---|---|---|

| Position | GBP.USD Close | USD Value | Rate | USD | |

| GBP.USD | -20,000 | 1.43232 | -28,646.40 | 1.113% | -0.89 |

Interest on Forex CFD balances is calculated on a stand-alone contract basis, and not combined or netted with other currency exposures, including Spot FX. Although IBKR does not directly reference swap rates, IBKR reserves the right to apply higher spreads in exceptional market conditions, such as during spikes in swap rates that can occur around fiscal year-ends.

Detailed interest schedules can be viewed here.

Trading: IBKR Forex CFDs are traded exactly like Spot FX, with the same over 20 available order types and algos. IBKR Forex CFDs can be traded either in classical TWS or in the IBKR FX Trader. To find the contract you want to trade in classical TWS or FX Trader, enter the currency pair (i.e. EUR.USD) and choose Sec Tyoe CFD in the Contract Selection pop-up.

Margin: IBKR Forex CFD margins are determined for each currency pair on a per contract basis without

regard to other Forex balances held in the account, including Spot FX. Margins start as low as 2.5% of contract value for major currency pairs. Details for all currency pairs can be found here. Retail clients are subject to minimum regulatory initial margins of 3.33% or 5% depending on the currency pair.

Commissions: IBKR passes through the prices that it receives and charges a separate low commission.

We do this in the interest of providing a transparent pricing structure instead of marking up our quotes and charging nothing in commissions as is the practice with many forex brokers. Commissions are tiered based on monthly traded value, and range from 0.20 basis points to 0.08 basis points. Both Forex CFD and spot FX volumes count toward the tiers.

Details are found here.

Trading Permissions: In order to trade Forex CFDs, you must set up the trading permission for Forex CFDs in Client Portal.

If your account is with IBKR (UK) or with IBKR LLC, IBKR will then set up a new account segment (identified with your existing account number plus the suffix “F”). Once the set-up is confirmed you can begin to trade. You do not need to fund the F-account separately, funds will be automatically transferred to meet CFD margin requirements from your main account.

If your account is with another IBKR entity, only the permission is required; an additional account segment is not necessary.

Trading Example (Professional Clients)

Opening the position

You purchase 10 lots (200000) EUR.CHF CFDs at $1.16195 for CHF 232,390, which you then hold for 5 days.

| EUR.CHF Forex CFDs – New Position | |

|---|---|

| Reference Underlying Price | 1.16188 - 1.16195 |

| CFDs Reference Price | 1.16188 - 1.16195 |

| Action | Buy |

| Quantity | 200,000 |

| Trade Value | CHF 232,390.00 |

| Margin (3% x 232,390) | AUD 9,100 |

| Interest Charged (on CHF 232,390 over 5 days) | |||

|---|---|---|---|

| Tier I (Pair BM 0.42% - IB Spread 1%) | CHF 232,390.00 | -0.58% | (CHF 18.72) |

Closing the position

| Exit CFD Position | ||

|---|---|---|

| Profit Scenario | Loss Scenario | |

| Reference Underlying Price | 1.16840 - 1.16848 | 1.15539 - 1.15546 |

| CFDs Reference Price | 1.16840 - 1.16848 | 1.15539 - 1.15546 |

| Action | Sell | Sell |

| Quantity | 200,000 | 200,000 |

| Trade Value | CHF 233,680.00 | CHF 231,078.00 |

| Trade P&L | CHF 1,290.00 | (CHF 1,312.00) |

| Financing | (CHF 18.72) | (CHF 18.72) |

| Entry Commission 0.002% | (CHF 4.65) | (CHF 4.65) |

| Entry Commission 0.002% | (CHF 4.67) | (CHF 4.62) |

| Total P&L | CHF 1,261.96 | (CHF 1,339.99) |

CFD Resources

Below are some useful links with more detailed information on IBKR’s CFD offering:

Frequently Asked Questions

Can anyone trade IBKR Forex CFDs?

All clients can trade IBKR CFDs, except residents of the USA, Canada, and Hong Kong. There are no exemptions based on investor type to the residency-based exclusions.

What is the difference between IBKR Forex CFDs and IBKR Cash Forex?

IBKR Cash Forex is a leveraged cash trade where you take delivery of the two currencies making up the pair. Your Forex-trading related balances are combined with your other balances arising out of your other trading activity, and you pay or receive interest on these consolidated balances based on the benchmark rate for each currency.

By contrast IBKR Forex CFDs are a contract which provides exposure but does not deliver the underlying currencies, and you pay or receive interest on the notional value of the contract. The benchmark rate for the contract is the difference between the benchmark rates for the two underlying currencies. This is in principle similar to the TOM Next rolls used by other brokers, but offers greater stability as benchmark rates generally are less volatile than swap rates.

Please see the Carry Interest section above for a detailed example.

Are there any market data requirements?

The market data for IBKR Forex CFDs is the same as for Leverage FX. It is a global permission and free of charge.

How are my CFD trades and positions reflected in my statements?

If you are a client of IBKR (U.K.) or IBKR LLC, your CFD positions are held in a separate account segment identified by your primary account number with the suffix “F”. You can choose to view Activity Statements for the F-segment either separately or consolidated with your main account. You can make the choice in the statement window in Client Portal.

If you are a client of other IBKR entities, there is no separate segment. You can view your positions normally alongside your non-CFD positions.

Can I trade Forex CFDs with the same order types and algos as Spot FX, and can I trade them in the FX Trader?

Yes, the trading experience is identical.

Willkommen bei Interactive Brokers

Übersicht:

Ihr Konto ist nun mit Einlagen ausgestattet und bestätigt - das heißt, Sie können beginnen zu handeln. Die nachfolgenden Informationen werden Ihnen den Start als Neukunde bei Interactive Brokers erleichtern.

- Ihr Vermögen

- Konfigurieren Sie Ihr Konto für den Handel

- So funktioniert der Handel

- Handel in aller Welt

- Fünf Punkte zur Optimierung Ihres IB-Kundenerlebnisses

1. Ihr Vermögen

Allgemeine Informationen zu Einzahlungen und Auszahlungen/Abhebungen. Alle Transaktionen werden über Ihr sicheres Kontoverwaltungssystem abgewickelt.

Einzahlungen

Zunächst müssen Sie eine Einzahlungsbenachrichtigung erstellen. Nutzen Sie hierzu folgenden Navigationspfad: Kontoverwaltung > Guthabenverwaltung > Guthabentransfers > Transaktionstyp: „Einzahlung“. Hier erfahren Sie, wie Sie eine Einzahlungsbenachrichtigung erstellen. Der zweite Schritt besteht darin, dass Sie Ihre Bank beauftragen, die Banküberweisung unter Verwendung der Bankverbindung, die Ihnen im Zuge der Erstellung der Einzahlungsbenachrichtigung mitgeteilt wird, auszuführen.

Auszahlungen/Abhebungen

Erstellen Sie eine Auszahlungsanweisung. Nutzen Sie hierzu folgenden Navigationspfad: Kontoverwaltung > Guthabenverwaltung > Guthabentransfers > Transaktionstyp: „Auszahlung“. Hier erfahren Sie, wie Sie eine Auszahlungsanweisung erstellen.

Wenn Sie eine Auszahlung beantragen, die die geltenden Auszahlungslimits überschreitet, wird diese als außerordentliche Auszahlung behandelt. Dies bedeutet, dass wir den Bankkontoinhaber und das IB-Konto abgleichen müssen. Falls das Zielbankkonto bereits für eine Einzahlung verwendet wurde, wird die Auszahlung bearbeitet. Andernfalls müssen Sie den Kundenservice kontaktieren und die erforderlichen Dokumente bereitstellen.

Problembehebung

Einzahlungen: Meine Bank hat das Guthaben übersendet, aber es wurde meinem IB-Konto noch nicht gutgeschrieben. Mögliche Gründe:

a) Ein Guthabentransfer dauert 1-4 Geschäftstage

b) Es fehlt eine Einzahlungsbenachrichtigung. Sie müssen diese in der Kontoverwaltung erstellen und ein Ticket an den Kundenservice schicken.

c) Korrekturdaten fehlen. Ihr Name oder Ihre IB-Kontonummer fehlt in den Transferdetails. Bitte kontaktieren Sie Ihre Bank und bitten Sie um die vollständigen Korrekturdaten.

d) Ein bei IB eingeleiteter ACH-Transfer ist auf 100,000 USD je Zeitraum von 7 Geschäftstagen beschränkt. Wenn Sie ein Portfolio-Margin-Konto eröffnet haben, bei dem eine Ersteinlage von 110,000 USD erforderlich ist, ist eine Einzahlung per Banküberweisung ggf. eine bessere Lösung, um die Wartezeit zu verringern, bis Sie beginnen können zu handeln. Wenn Sie ACH als Methode auswählen, können Sie entweder eine Wartezeit von knapp 2 Wochen in Kauf nehmen oder ein temporäres Downgrade auf ein Reg-T-Konto als mögliche Lösung erwägen.

Auszahlungen: Ich habe eine Auszahlung beantragt, aber das Guthaben wurde noch nicht meinem Bankkonto gutgeschrieben. Mögliche Gründe:

a) Ein Guthabentransfer dauert 1-4 Geschäftstage

b) Abgelehnt. Überschreitung des maximal möglichen Auszahlungsbetrags. Bitte prüfen Sie den Barsaldo Ihres Kontos. Beachten Sie, dass aus regulatorischen Gründen ab Einzahlung des Guthabens eine Haltefrist von 3 Tagen gilt, ehe das Guthaben ausgezahlt/abgehoben werden kann.

c) Ihre Bank hat das Guthaben zurückgesendet. Vermutlich stimmen die Namen des empfangenden Kontos und des sendenden Kontos nicht überein.

2. Konfigurieren Sie Ihr Konto für den Handel

Unterschied zwischen Cash- und Marginkonten: Falls Sie sich für unsere FastTrack-Kontoeröffnung entschieden haben, ist Ihr Konto automatisch ein Cash-Konto mit Handelsberechtigungen für US-Aktien. Wenn Sie Leverage nutzen und auf Marginbasis handeln möchten, erfahren Sie hier, wie Sie ein Upgrade Ihres Kontos auf ein Reg-T-Margin-Konto durchführen können.

Handelsberechtigungen

Um mit einem bestimmten Instrument in einem bestimmten Land handeln zu können, müssen Sie über die Kontoverwaltung die entsprechenden Handelsberechtigungen beantragen. Bitte beachten Sie, dass Handelsberechtigungen kostenlos sind. Möglicherweise werden Sie jedoch gebeten, Risikoinformationsdokumente zu unterzeichnen, die von örtlichen Aufsichtsbehörden benötigt werden. Hier erfahren Sie, wie Sie Handelsberechtigungen beantragen können.

Marktdaten

Wenn Sie für ein bestimmtes Produkt oder eine bestimmte Börse Echtzeit-Marktdaten beziehen möchten, müssen Sie ein Marktdatenpaket abonnieren und Abonnementgebühren an die entsprechende Börse entrichten. Hier erfahren Sie, wie Sie Marktdaten abonnieren können.

Der Marktdatenassistent hilft Ihnen bei der Auswahl des richtigen Datenpakets. Bitte sehen Sie sich dieses Video an, indem die Funktionsweise erläutert wird.

Kunden können für Ticker, zu denen sie kein Abonnement abgeschlossen haben, kostenlose verzögerte Marktdaten beziehen. Klicken Sie dazu auf die Schaltfläche „Kostenlose verzögerte Marktdaten“ in der entsprechenden Tickerzeile.

Beraterkonten

Werfen Sie einen Blick in unseren „Getting Started Guide“ für Berater. Hier erfahren Sie, wie Sie für Ihr Beraterkonto weitere Benutzer anlegen können, diesen Zugriffsrechte erteilen und vieles mehr.

3. So funktioniert der Handel

Wenn Sie den Umgang mit unserer Handelsplattformen erlernen möchten, ist die Trader-Akademie die beste Anlaufstelle für Sie. Dort finden Sie unsere Live-Webinare und Webinaraufzeichnungen in 10 Sprachen, sowie Touren und Dokumente zu unseren verschiedenen Handelsplattformen.

Trader Workstation (TWS)

Traders, die ausgefeilte Trading-Tools verwenden möchten, können unsere Market-Maker-entwickelte Trader Workstation (TWS) verwenden. Mit dieser Plattform können Sie dank einer benutzerfreundlichen tabellarischen Oberfläche Ihre Handelsgeschwindigkeit und Effizienz optimieren. Es werden über 60 Ordertypen und aufgabenspezifische Tools für sämtliche Trading-Stile angeboten und Kontosalden und Kontoaktivitäten können in Echtzeit geprüft und überwacht werden. Testen Sie die zwei verfügbaren Varianten:

TWS Mosaic: intuitiv und benutzerfreundlich, einfacher Handelszugang, Ordermanagement, Watchlisten und Charts, zusammengestellt in einer Ansicht, oder

Klassische TWS: Erweitertes Ordermanagement für Trader, die komplexere Tools und Algorithmen.

Allgemeine Beschreibung und Informationen / Kurzanleitung / Benutzerhandbuch

Interaktive Touren: TWS Grundlagen / TWS Konfiguration / TWS Mosaic

Platzierung einer Transaktion: Video zur klassischen TWS / Video zu Mosaic

Trading-Tools: Allgemeine Beschreibung und Informationen / Benutzerhandbuch

Anforderungen: Installation von Java für Windows / Installation von Java für MAC / Port 4000 und 4001 müssen offen sein

Login in die TWS / Download der TWS

WebTrader

Trader, die eine einfache und besonders übersichtliche Oberfläche bevorzugen, können unseren HTML-basierten WebTrader verwenden. Mit dieser Anwendung können Sie sich völlig unkompliziert Marktdaten anzeigen lassen, Orders übermitteln und Ihr Konto und Ihre Ausführungen kontrollieren. Nutzen Sie die aktuellste WebTrader-Version für Ihren jeweiligen Browser.

Kurzanleitung / WebTrader-Benutzerhandbuch

Einführung: Video zum WebTrader

Platzierung einer Transaktion: Video zum WebTrader

Login in den WebTrader

MobileTrader

Mit unseren Softwarelösungen für Mobilgeräte können Sie unterwegs Handel mit Ihrem IB-Konto betreiben. Die mobileTWS für iOS und die mobileTWS für BlackBerry sind speziell für diese Beliebten Modelle entwickelte Anwendungen, während die allgemeine MobileTrader-App auf den meisten anderen Smartphone-Typen unterstützt wird.

Allgemeine Beschreibung und Informationen

Ordertypen: Verfügbare Ordertypen und Beschreibungen / Videos / Tour / Benutzerhandbuch

Paper-Trading: Allgemeine Beschreibung und Informationen / So erhalten Sie ein simuliertes Paper-Trading-Konto

Sobald Ihr simuliertes Konto angelegt wurde, können Sie die Marktdaten aus Ihrem realen Konto mit dem Paper-Trading-Konto teilen: Kontoverwaltung > Konto verwalten > Einstellungen > Paper-Trading

4. Handel in aller Welt

IB-Konten sind Multiwährungskonten. In Ihrem Konto können Sie gleichzeitig mehrere verschiedene Währungen halten, was Ihnen den Handel mit verschiedenen Produkten in aller Welt in einem einzigen Konto ermöglicht.

Basiswährung

Ihre Basiswährung ist die Umrechnungswährung für Ihre Kontoauszüge und die Währung, die zur Berechnung Ihrer Margin-Anforderungen verwendet wird. Sie legen die Basiswährung für Ihr Konto im Rahmen des Kontoeröffnungsprozesses fest. Kunden können ihre Basiswährung jederzeit in der Kontoverwaltung ändern.

Wir wandeln Devisenpositionen automatisch in Ihre Basiswährung um.

Währungsumwandlungen müssen manuell vom Kunden vorgenommen werden. In diesem Video erfahren Sie, wie Sie eine Währungsumwandlung ausführen.

Wenn Sie eine Position in einer Währung eröffnen möchten, die Sie nicht in Ihrem Konto haben, haben Sie zwei Möglichkeiten:

A) Währungsumwandlung

B) IB-Margindarlehen (nicht für Cash-Konten verfügbar)

In diesem Kurs finden Sie eine Erläuterung der Funktionsweisen von Forex-Transaktionen

5. Fünf Punkte zur Optimierung Ihres Kundenerlebnisses

1. Kontraktsuche

Hier finden Sie unsere sämtlichen Produkte, Symbole und Spezifikationen.

2. IB Wissensdatenbank

Die Wissensdatenbank ist eine Sammlung aus Glossarbegriffen, Hilfe-Artikeln, Problemlösungstipps und Leitfäden, die Sie bei der Verwaltung Ihres IB-Kontos unterstützen können. Geben einfach in das Suchfeld ein, was Sie wissen möchten, und finden Sie Ihre Antwort.

3. Kontoverwaltung

Während unsere Trading-Plattformen Ihnen Zugang zu den Märkten gewähren, bietet die Kontoverwaltung Ihnen Zugang zu Ihrem IB-Konto. In der Kontoverwaltung können Sie Aufgaben rund um Ihr Konto ausführen, wie zum Beispiel Guthaben ein- und auszahlen, Kontoauszüge ansehen, Marktdaten- und Nachrichtenabonnements anpassen, Handelsberechtigungen ändern und Ihre persönlichen Informationen verifizieren oder ändern.

Login in die Kontoverwaltung / AM-Kurzanleitung / AM-Benutzerhandbuch

4. Das Secure-Login-System

Um Ihnen online das größtmögliche Maß an Sicherheit zu gewähren, hat Interactive Brokers das Secure-Login-System (SLS) eingeführt. Bei diesem System erfolgt der Zugriff auf Ihr Konto mittels einer Zwei-Faktoren-Authentifizierung - d. h. Ihre Identität wird bei der Anmeldung unter Verwendung von zwei Sicherheitsfaktoren überprüft: 1) ein Faktor, der auf Ihrem Wissen basiert (Eingabe Ihres Benutzernamens und Passworts), und 2) ein Faktor, der auf etwas in Ihrem physischen Besitz basiert (ein von IB bereitgestelltes Sicherheitsgerät, das zufällige, einmalig verwendbare Sicherheitscodes generiert). Da sowohl Kenntnis über Ihren Benutzernamen und Ihr Passwort als auch der physische Besitz des Sicherheitsgerätes für eine erfolgreiche Anmeldung im Konto erforderlich sind, wird die Gefahr eines Zugriffs auf Ihr Konto durch eine andere Person als Sie durch die Teilnahme am Secure-Login-System praktisch ausgeschlossen.

Aktivierung Ihres Sicherheitsgerätes / Erhalt einer Sicherheitscodekarte / Rücksendung Ihres Sicherheitsgerätes an IB

Sollten Sie Ihr Passwort vergessen oder Ihre Sicherheitscodekarte verloren haben, kontaktieren Sie uns bitte telefonisch für sofortigen Support.

5. Kontoauszüge und Berichte

Unsere Kontoauszüge und Berichte lassen sich ganz einfach erstellen und anpassen und decken alle Aspekte Ihres Kontos bei Interactive Brokers ab. Hier erfahren Sie, wie Sie Ihre Umsatzübersichten öffnen können.

Welcome to Interactive Brokers

Übersicht:

Now that your account is funded and approved you can start trading. The information below will help you getting

started as a new customer of Interactive Brokers.

- Your Money

- Configure your account to trade

- How to trade

- Trade all over the World

- Five points to enrich your IB experience

1. Your Money

Deposits & Withdrawals General Info. All transactions are administered through your secure Account Management

Deposits

First, you create a deposit notification through your Account Management > Funding > Fund Transfers > Transaction Type: “Deposit” How to create a deposit notification. The second step is to instruct your Bank to do the wire transfer with the bank details provided in your Deposit Notification.

Withdrawals

Create a withdrawal instruction via your secure Account Management > Funding > Fund Transfers > Transaction Type: "Withdrawals" How to create a withdrawal instruction

If you instruct a withdrawal over the Withdrawal limits, it will be considered an exceptional withdrawal and we will therefore need to match bank account holder and IB account. If destination bank account has been used for a deposit, withdrawal will be processed; otherwise, you must contact customer service and provide the documents needed.

Troubleshooting

Deposits: My bank sent the money but I do not see it credited into my IB account. Possible reasons:

a) A fund transfer takes 1-4 business days

b) A Deposit Notification is missing. You have to create it via your Account Management and send a ticket to Customer Service

c) Amending details are missing. Your name or IB account number is missing in the transfer details. You have to contact your bank and ask for the full amending details.

d) ACH initiated by IB is limited to 100k USD in a 7 business period. If you opened a Portfolio Margin account where the initial requirement is 110k, a wire deposit might be the better deposit option to reduce wait time for your first trade. If selecting ACH a wait time of almost 2 weeks or a temporary downgrade to RegT can be possible solutions.

Withdrawals: I have requested a withdrawal but I do not see the money credited to my bank account. Possible reasons:

a) A fund transfer takes 1-4 business days

b) Rejected. Over the max it can be withdrawn. Please check your account cash balance. Note that for regulatory requirements, when the funds are deposited, there is a 3 day holding period before they can be withdrawn.

c) Your bank returned the funds. Probably because receiving bank account and remitting bank account names do not match.

2. Configure your account to trade

Difference between Cash and Margin accounts: If you have chosen the FastTrack application, by default your account type is a cash account with US stock permission. If you would like to get leverage and trade on margin, here how to upgrade to a RegT Margin account

Trading Permissions

In order to be able to trade a particular asset class in a particular country, you need to get the trading permission for it via your Account Management. Please note that trading permissions are free. You might however be asked to sign risk

disclosures required by local regulatory authorities. How to Request Trading Permissions

Market Data

If you want to have market data in real-time for a particular product/exchange, you need to subscribe to a market data package charged by the exchange. How to subscribe to Market data

The Market data assistant will help you choose the right package. Please watch this Video explaining how it works.

Customers have the option to receive delayed market data for free by clicking the Free Delayed Data button from a non-subscribed ticker row.

Advisor Accounts

Have a look at the user guide getting started as advisors. Here you see how to create additional users to your advisor account and grant them access and much more.

3. How to trade

The Trader's University is the place to go when you want to learn how to use our Platforms. Here you will find our webinars, live and recorded in 10 languages and tours and documentation about our various Trading Platforms.

Trader Workstation (TWS)

Traders who require more sophisticated trading tools can use our market maker-designed Trader Workstation (TWS), which optimizes your trading speed and efficiency with an easy-to-use spreadsheet interface, support for more than 60 order types, task-specific trading tools for all trading styles, and real-time account balance and activity monitoring. Try the two models

TWS Mosaic: for intuitive usability, easy trading access, order management, watchlist, charts all in one window or

TWS Classic: the Advanced Order Management for traders who need more advanced tools and algos.

General Description and Information / Quick start guide / Usersguide

Interactive Tours: TWS Basics / TWS configuration / TWS Mosaic

How to place a trade: Video Classic TWS / Video Mosaic

Trading tools: General Description and Information / Users guide

Requirements: How to install Java for Windows / How to install Java for MAC / Port 4000 and 4001 needs to be open

Login TWS / Download TWS

WebTrader

Traders who prefer a clean and simple interface can use our HTML-based WebTrader, which makes it easy to view market data, submit orders, and monitor your account and executions. Use the latest WebTrader from every browser

Quick Start Guide / WebTrader User's Guide

Introduction: Video WebTrader

How to place a Trade: Video WebTrader

Login WebTrader

MobileTrader

Our mobile solutions allow you to trade your IB account on the go. The mobileTWS for iOS and the mobileTWS for BlackBerry are custom-designed for these popular models, while the generic MobileTrader supports most other Smart phones.

General Description and Information

Order Types Order Types available and Description / Videos / Tour / Users guide

Paper Trading General Description and Information / How to get a Paper Trading Account

Once your paper account is created, you can share the market data of your real account with your paper trading account: Account Management > Manage Account > Settings > Paper trading

4. Trade all over the World

IB accounts are multi-currency accounts. Your account can hold different currencies at the same time, this allows you to trade multiple products around the world from a single account.

Base Currency

Your base currency determines the currency of translation for your statements and the currency used for determining margin requirements. Base currency is determined when you open an account. Customers may change their base currency at any time through Account Management.

We do not automatically convert currencies into your Base currency

Currency conversions must be done manually by the customer. In this video you can learn how to do a currency conversion.

In order to open a position denominated in a currency that you do not have in your account, you have two possibilities:

A) Currency conversion.

B) IB Margin Loan. (Not available for Cash Accounts)

Please see this course explaining the mechanics of a foreign transaction.

5. Five points to enrich your IB experience

1. Contract Search

Here you will find all our products, symbols and specifications.

2. IB Knowledge Base

The Knowledge Base is a repository of glossary terms, how-to articles, troubleshooting tips and guidelines designed to assist IB customers with the management of their IB accounts. Just enter in the search button what you are looking for and you will get the answer.

3. Account Management

As our trading platforms give you access to the markets, the Account Management grants you access to your IB account. Use Account Management to manage account-related tasks such as depositing or withdrawing funds, viewing your statements, modifying market data and news subscriptions, changing your trading permissions, and verifying or changing your personal information.

Log In Account Management / AM Quick Start Guide / AM Users Guide

4. Secure Login System

To provide you with the highest level of online security, Interactive Brokers has implemented a Secure Login System (SLS) through which access to your account is subject to two-factor authentication. Two-factor authentication serves to confirm your identity at the point of login using two security factors: 1) Something you know (your username and password combination); and 2) Something you have (an IB issued security device which generates a random, single-use security code). As both knowledge of your username/password and physical possession of the security device are required to login to your account, participation in the Secure Login System virtually eliminates the possibility of anyone other than you accessing your account.

How to Activate your Security Device / How to Obtain a Security Code Card / How to return Security device

In case you forgot your password or lost your security code card, please call us for immediate assistance.

5. Statements and Reports

Easy to view and customize, our statements and reports cover all aspects of your Interactive Brokers account. How to view an Activity Statement

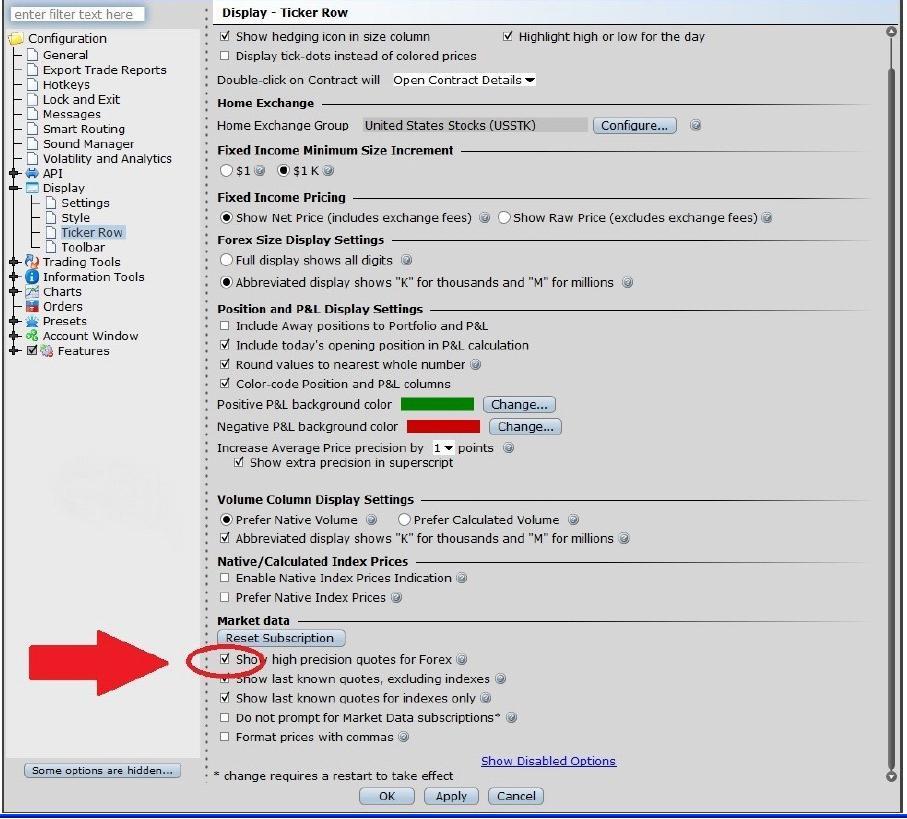

Information regarding high precision forex quotes

Übersicht:

Clients wishing to see forex (IDEALPRO) market data in a more detailed way can now control the order book display mode via the Global Configuration. In order to access this feature you must use TWS release 944.2b or higher. The display mode selection allows the order book to be viewed either as:

- Rounded prices (default): market data is rounded out to the next 0.5 pip. This is identical to the current display functionality for the IB trading platforms. This setting provides a more stable visible quote and a larger ‘top-of-book’ size since it includes the available size at multiple price levels up to the rounded price.

- Unrounded prices: market data is visible in 0.1 pip increments. This allows you to see prices in a more granular fashion, but the displayed values will change more rapidly and the sizes for the top-of-book may appear to be smaller.

It is important to understand that either display mode accesses the same IDEALPRO order book. Order submission will still be in 0.5 pip increments and orders submitted in either display mode will execute in exactly the same way. As in the past (and currently), in cases where the order book has prices at better than your order’s limit price, you will receive the full price improvement.

Instructions on how to display high precision forex quotes

In Global Configuration go to Display, choose Ticker Row and then at the bottom of the window in the Market Data section tick Show high precision quotes for Forex. Then press apply or ok to enable the new setting.

"EMIR": Reporting to Trade Repository Obligations and Interactive Brokers Delegated Service to help meet your obligations

1. Background: In 2009 the G20 pledged to undertake reforms aimed at increasing transparency and reducing counterparty risk in the OTC derivatives market post the financial crisis of 2008. The European market infrastructure regulation (“EMIR”) implements most of these pledges in the EU. EMIR is a EU regulation and entered into force on 16 August 2012.

2. Financial instruments and asset classes reportable under EMIR: OTC and Exchange Traded derivatives for the following asset classes: credit, interest, equity, commodity and foreign exchange derivatives Reporting obligation does not apply to exchange traded warrants.

3. Who do EMIR reporting obligations apply to: Reporting obligations normally apply to all counterparties established in the EU with the exception of natural persons. They apply to:

* Financial Counterparties (“FC”)

* Non-financial counterparties above the clearing threshold (“NFC+”)

* Non-financial counterparties below the clearing threshold (“NFC-“)

* Third country Entities outside the EU (“TCE”) in some limited circumstances

The reporting obligations essentially apply to any entity established in the EU that has entered into a derivatives contract.

4. Financial counterparties (“FC”): include banks, investment firms, credit institutions, insurers, UCITS and pension schemes and Alternative Investment Fund managed by an AIFM. The Alternative Investment Fund (“AIF”) will only become an FC if the manager of that AIF is authorised under the Alternative Investment Fund Managers Directive (“AIFMD”), so a fund outside the EU may be subject to EMIR reporting requirements.

5. Non-Financial Counterparty (“NFC”): A NFC is defined as an undertaking established in the EU other than those defined as a FC or a Central Counterparty (“CCP”), like the Clearing Houses. NFCs have lesser obligations than FCs. But when an NFC breaches a “clearing threshold” it becomes an NFC+, when it is subject to almost the same obligations as FCs (including collateral and valuation reporting). NFCs below the clearing threshold are known as NFC-s. In practice anyone other than a natural individual person (i.e. an individual or individuals operating a joint

account) is defined as an NFC- and subject to reporting obligations.

INTERACTIVE BROKERS DELEGATED REPORTING SERVICE TO HELP MEET YOUR REPORTING OBLIGATIONS

6. What service will Interactive Brokers offer to its customers to facilitate them fulfill their reporting obligations i.e. will it offer a delegated service for trade reporting as well as facilitating issuance of LEI: As noted above, both FCs and NFCs must report details of their transactions (both OTC and ETD) to authorized Trade Repositories. This obligation can be discharged directly through a Trade Repository, or by delegating the operational aspects of reporting to the counterparty or a third party (who submits reports on their behalf).

Interactive Brokers intends to facilitate the issuance of LEIs and offer delegated reporting to customers for whom it executes and clear trades, subject to customer consent, to the extent it is possible to do so from an operational, legal and regulatory perspective.

If you are subject to EMIR Reporting you will shortly be able to log into the IB Account Management system and apply for an LEI and delegate your reporting to Interactive Brokers.

We intend to include valuation reporting but only if and to the extent and for so long as it is permissible for Interactive brokers to do so from a legal and regulatory perspective and where the counterparty is required to do so (i.e. in cases where it is a FC or NFC+).

However, this would be subject to condition that Interactive Brokers uses its own trade valuation for reporting purposes.

7. Can EMIR reporting be delegated: EMIR allows either counterparty to delegate reporting to a third-party. If a counterparty or CCP delegates reporting to a third party, it remains ultimately responsible for complying with the reporting obligation. Likewise, the counterparty or CCP must ensure that the third party to whom it has delegated reports correctly. Brokers and dealers do not have a reporting obligation when acting purely in an agency capacity. If a block trade gives rise to multiple transactions, each transaction would have to be reported.

FUNDS AND SUB-FUNDS - The obligations under EMIR are on the counterparty which may be the fund or sub-fund. The fund or sub-fund that is the principal to transactions will have to provide details of their classification (FC, NFC+ or NFC-), authorization for delegated reporting and Legal Entity Identifier (“LEI”) application.

8. Exemptions under Article 1(4) and 1(5) of EMIR: Articles 1(4) and 1(5) of EMIR exempt certain entities from some or all of the obligations set out in EMIR, depending on their classification. Specifically, exempt entities under Article 1(4) are exempt from all obligations set out in EMIR, while exempt entities under Article 1(5) are exempt from all obligations except the reporting obligation, which continues to apply.

9. Entities qualifying under Article 1(4) and 1(5) of EMIR: Article 1(4) initially applied only to EU central banks, Union public bodies involved in the management of public debt and the Bank for International Settlements. Subsequently the

application of the Article 1(4) exemption was extended to include the central banks and debt management offices of the United States and Japan. The Commission has indicated that further foreign central banks and debt management offices may be added in the future if they are satisfied that equivalent regulation is put in place in those jurisdictions. Article 1(5) broadly exempts the following categories of entities:

- Multilateral development banks;

- Non-commercial public sector entities owned and guaranteed by central government; and

- The European Financial Stability Facility and the European Stability Mechanism.

10. OTC and Exchange Traded Derivatives: There is no distinction between reporting of exchange traded derivatives (“ETDs”) and OTC contracts within the level 1 regulations, implementing technical standards, or regulatory technical standards of ESMA.

The contract is to be identified by using a unique product identifier. In addition, a unique trade identifier will be required for transactions. In the event that a globally agreed system of product identifiers does not materialise, it has been suggested that International Securities Identification numbers (“ISIN”), Alternative Instruments Identifiers (“AII”), or Classification of Financial Instruments Codes (“CFI”) may serve as alternatives.

11. Trade repository Interactive Brokers use: Interactive Brokers (U.K.) Limited will use the services of CME ETR, which is part of the CME Group.

12. Issuance of Legal Entity Identifiers (“LEI”)

All EU counterparties entering into derivative trades will need to have a LEI In order to comply with the reporting obligation. The LEI will be used for the purpose of reporting counterparty data.

A LEI is a unique identifier or code attached to a legal person or structure, that will allow for the unambiguous identification of parties to financial transactions.

“EMIR”: Further Information on Reporting to Trade Repository Obligations

13. Thresholds which determine whether an NFC is an NFC+ or NFC-: Breaching any of the following clearing threshold values will mean classification as an NFC+. Positions must be calculated on a notional, 30-day rolling average basis:

• EUR 1 billion in gross notional value for OTC credit derivative contracts;

• EUR 1 billion in gross notional value for OTC equity derivative contracts;

• EUR 3 billion in gross notional value for OTC interest rate derivative contracts;

• EUR 3 billion in gross notional value for OTC FX derivative contracts; and

• EUR 3 billion in gross notional value for OTC commodity derivative contracts and other OTC derivative contracts not covered above.

For the purpose of calculating whether a clearing threshold has been breached, an NFC must aggregate the transactions of all non-financial entities in its group (and determine whether or not those entities are inside or outside the EU) but discount transactions entered into for hedging or treasury purposes. The term “hedging transactions” in this context means transactions objectively measureable as reducing risks directly relating to the commercial activity or treasuring financing activity of the NFC or its group.

14. Reporting Of Exposures: FCs and NFC+s must report on:

* Mark-to-market or mark-to-model valuations of each contract

* Details of all collateral posted, either on a transaction or portfolio basis (i.e. where collateral is calculated on the basis of net positions resulting from a set of contracts rather than being posted on a transaction by transaction basis)

15. Timetable to report to Trade repositories: The reporting start date is 12 February 2014:

* New contracts they enter into on or after February 12th, on a trade date +1;

* Positions open from contracts entered into on or after 16 August 2012 and still open on February 12th, 2014 must be reported to a trade repository by February 12th 2014;

* Positions open from contracts entered into before 16th August and still open on February 12th, 2014 must be reported to a trade repository by 13th May 2014;

* Reporting of valuation and collateral must be reported to a trade repository by 12th August 2014;

* Contracts that were either entered before, on or after 16 August 2012 but not open on 12th February 2014 must be reported to a trade repository by February 12th, 2017.

16. What must be reported and when: Information must be reported on the counterparties to each trade (counterparty data) and the contracts themselves (common data).

There are 26 items that must be reported with regard to counterparty data, and 59 items that must be reported with regard to common data. These items are set out within tables 1 and 2 of the Annex to the ESMA’s Regulatory technical standards on minimum details to be reported to trade repositories.

Counterparties and CCPs have to make a report:

* when a contract is entered into

* when a contract is modified

* when a contract is terminated

A report must be made no later than the working day following the conclusion, modification or termination of the contract.

17. What has to be reported and who is responsible for reporting: Reporting applies to both OTC derivatives and exchange traded derivatives. The reporting obligation applies to counterparties to a trade, irrespective of their classification. Please note:

* Reporting of valuation and collateral is only required for FCs and NFC+s

* Every trade must be normally be reported by both counterparties.

THIS INFORMATION IS GUIDANCE FOR INTERACTIVE BROKERS CLEARED CUSTOMERS ONLY