Short részvényhozamok után járó kamatjóváírás

Overview:

Hogyan lehet meghatározni a kölcsönzött részvénypozíciókkal kapcsolatos kamatjóváírást vagy díjat?

Background:

Amikor egy számlatulajdonos részvényeket shortol, az IBKR azonos mennyiségű részvényt kölcsönvesz a számlatulajdonos nevében, hogy teljesíteni tudja a vevő felé fennálló kötelezettségét. A részvénykölcsönzési megállapodás előírja, hogy az IBKR a kölcsön biztosítékaként nyújtson készpénzfedezetet a részvények kölcsönbeadójának. A készpénzfedezet összege a részvények értékének iparági szabvány (Collateral Mark) szerinti számításán alapul .

A részvények kölcsönbeadója kamatot fizet az IBKR-nek a készpénzfedezet után, továbbá díjat is felszámít a szolgáltatás nyújtásáért oly módon, hogy a fizetendő kamatot kiigaztíja egy olyan összeggel, ami nem éri el a készpénzbetétekre aktuálisan fizetett piaci kamatot (USD készpénzegyenlegek után a kamat alapja a tényleges Fed alapkamat). Nehezen kölcsönözhető részvények esetén a kölcsönbeadót megillető díj nettó negatív kamatlábat eredményezhet az IBKR-nél.

Bár a legtöbb bróker kizárólag az intézményi ügyfeleinek adja tovább ezen vissszatérítés egy részét, az IBKR minden ügyfele kamatjóváírást kap a 100 000 USD-t vagy annak megfelelő, más devizában kifejezett összeget meghaladó short részvényeladások hozamából. Amikor egy kölcsönözhető értékpapírból rendelkezésre álló kínálat a kölcsönzési kereslethez képest magas, a számlatulajdonosok a referencia-kamatlábnak (pl. USD egyenlegeknél a tényleges egynapos Fed alapkamat) megfelelő kamatjóváírásra számíthatnak a short részvényegyenlegük után, csökkentve a vonatkozó spreaddel, ami jelenleg 1,25% (100 000 USD egyenleg) és 0,25% (3 000 000 USD egyenleg) között mozog. A kamatok előzetes értesítés nélkül változhatnak.

Ha egy adott értékpapír kínálati és keresleti tulajdonságai miatt nehézzé válik a kölcsönzés, a kölcsönbeadó által kínált visszatérítés csökken, és akár terhelést is eredményezhet a számlán. A visszatérítés vagy terhelés magasabb kölcsönzési díj formájában kerül áthárításra a számlatulajdonosra, ami meghaladhatja a short eladás hozamából eredő kamatjóváírást, és nettó terhelést eredményezhet a számlán. Mivel a kamatok értékpapíronként és dátumonként is változhatnak, az IBKR azt javasolja, hogy az ügyfelek használják az Ügyfélportál Támogatás menüpontjában elérhető Shortolható Részvények Elérhetősége eszközt a short eladások tájékoztató kamatlábainak megtekintéséhez. Felhívjuk a figyelmet, hogy a fenti eszközben megjelenített tájékoztató kamatlábak célja, hogy megfeleljenek az IBKR által a Tier III egyenlegekre (azaz a 3 millió USD vagy nagyobb short eladások többlethozamaira) fizetett, a short eladások hozamából eredő kamatoknak. Alacsonyabb egyenlegek esetén a kamat az adott Tier, illetve a kereskedési devizához kapcsolódó referencia-kamatláb alapján kerül kiigazításra. A pontos kamatlábat a Short eladások készpénz hozamegyenlege után Önnek fizetett kamat kalkulátor segítségével tudja kiszámítani.

A további példákat és a kalkulátort ld. az Értékpapír-finanszírozás oldalon.

FONTOS MEGJEGYZÉS

A Short Részvények Elérhetősége Eszközben és a TWS-ben a kölcsönözhető részvényekkel és a tájékoztató kamatlábakkal kapcsolatos információkat a legjobb tudásunk szerint közöljük, ugyanakkor nem vállalunk garanciát azok pontosságára vagy érvényességére. A részvények elérhetősége harmadik felektől származó, nem valós időben frissített információkat is tartalmaz. A kamatlábakra vonatkozó információk csak tájékoztató jellegűek. Egy kereskedési munkamenet során végrehajtott ügyletek általában 2 munkanapon belül kerülnek elszámolásra, és a tényleges elérhetőséget és kölcsönzési költséget az elszámolás napján határozzuk meg. A kereskedőknek tisztában kell lenniük azzal, hogy a kamatok és elérhetőségek jelentős mértékben megváltozhatnak a kötés és az elszámolás napja között, különösen a kis forgalmú és alacsony kapitalizációjú részvények, illetve azon részvényosztályok esetén, ahol küszöbön áll valamilyen vállalati esemény (pl. osztalékfizetés). További részletekért kérjük, tekintse meg a Short eladás operatív kockázatai oldalt.

Részvényhozam-növelő program GYIK

Mi a célja a Részvényhozam-növelő programnak?

A Részvényhozam-növelő program segítségével ügyfeleink többletjövedelemre tehetnek szert a meglévő (azaz teljes mértékben befizetett és fedezeten túli) értékpapír-pozícióik után (amelyeket egyébként el kellene különíteni) oly módon, hogy engedélyezik az IBKR számára ezen értékpapírok harmadik feleknek történő kölcsönadását. A programban részt vevő ügyfelek biztosítékot (vagy amerikai államkötvényt vagy készpénzt) kapnak a kölcsönadott részvényeik lejáratkori visszaszármaztatására.

Mik a teljes mértékben befizetett és fedezeten túli értékpapírok?

A teljes mértékben befizetett értékpapírok egy ügyfél számláján lévő olyan értékpapírok, amelyek vételárát az ügyfél már maradéktalanul befizette. A fedezeten túli értékpapírok olyan értékpapírok, amelyek vételárát az ügyfél még nem fizette be maradéktalanul, de amelyek piaci értéke meghaladja az ügyfél fedezeti tartozik egyenlegének 140%-át.

Hogyan kell meghatározni az ügyfelet egy Részvényhozam-növelő program szerinti hitelügylet után megillető jövedelmet?

Az ügyfelet a kölcsönadott részvényei után megillető jövedelmet a tőzsdén kívüli értékpapír-kölcsönzési piacon alkalmazott kamatlábak alapján kell meghatározni. Ezek a kamatlábak jelentős eltéréseket mutathatnak nem csak a kölcsönadott értékpapír, hanem a kölcsön időpontja függvényében is. Az IBKR általában a részvények kölcsönadásából általa realizált bevétel hozzávetőleg 50%-ának megfelelő kamatot fizet a programban részt vevő ügyfelek biztosítéka után.

Hogyan kell meghatározni egy adott hitel biztosítékának az összegét?

Az értékpapír-kölcsön biztosítékának (ami lehet amerikai államkötvény vagy készpénz) a kamatjövedelem meghatározására is használt összegét az iparági konvencióknak megfelelően kell meghatározni, azaz a részvény záróárát meg kell szorozni egy bizonyos százalékos értékkel (általában 102-105%), majd a kapott számot felfelé kell kerekíteni a legközelebbi dollárra/centre/pennyre stb. Devizánként eltérőek lehetnek az iparági konvenciók. Például egy 100 darabból álló, 59,24 USD záróárú amerikai részvénycsomag kölcsönzése esetén a biztosíték 6 100 USD lenne (59,24 USD x 1,02 = 60,4248; kerekítve: 61 USD, szorozva 100-zal). Az alábbi táblázat tartalmazza a különböző iparági konvenciókat devizánként:

| USD | 102%; a legközelebbi dollárra felkerekítve |

| CAD | 102%; a legközelebbi dollárra felkerekítve |

| EUR | 105%; a legközelebbi centre felkerekítve |

| CHF | 105%; a legközelebbi rappenre felkerekítve |

| GBP | 105%; a legközelbbi penny-re felkerekítve |

| HKD | 105%; a legközelebbi centre felkerekítve |

További információkért lásd KB1146.

Hol és hogyan tartjuk a Részvényhozam-növelő program alapján nyújtott kölcsönök biztosítékát?

Az IBLLC ügyfelei esetén a biztosítékot vagy készpénzben vagy amerikai államkötvényben tartjuk, és az IBLLC egyik leányvállalatának, az IBKR Securities Services LLC-nek („IBKRSS”) adjuk át megőrzésre. A Program alapján nyújtott kölcsönök biztosítékát az IBKRSS egy az Ön javára fenntartott számlán tartja, melynek vonatkozásában Önt perfektuált elsőbbségi biztosítéki jog illeti meg. Az IBLLC nem-teljesítése esetén Ön az IBLLC-t kiiktatva, közvetlenül az IBKRSS-en keresztül férhet hozzá a biztosítékhoz. További információkért kérjük, olvassa el az Értékpapírszámla-felügyeleti megállapodást itt. Nem-IBLLC ügyfelek esetén a biztosítékot a számlavezető fogja tartani és megvédeni. IBIE számlák esetén például a biztosítékot az IBIE fogja tartani és megvédeni.

Hogyan befolyásolják a kamatokat a long ügyletek, az IBKR Részvényhozam-növelő programja keretében kölcsönadott értékpapírok átruházása, illetve a programból való kivonása?

A kamat felhalmozódása a kötés napját követő munkanapon (T+1) szűnik meg. A kamat felhalmozódása szintén megszűnik az átruházási megbízás benyújtását illetve a programból történő kivonást követő munkanapon.

Melyek az IBKR Részvényhozam-növelő programban való részvétel jogosultsági feltételei?

| JOGOSULT SZERVEZETEK* |

| IB LLC |

| IB UK (SIPP számlák kivételével) |

| IB IE |

| IB CE |

| IB HK |

| IB Canada (RRSP/TFSA számlák kivételével) |

| IB Singapore |

| JOGOSULT SZÁMLATÍPUSOK |

| Készpénz (50 000 USD-t meghaladó minimális tőke a csatlakozás napján) |

| Fedezet |

| Pénzügyi tanácsadói ügyfélszámlák* |

| Közvetítő bróker ügyfélszámlák: nyilvános és nem-nyilvános* |

| Közvetítő bróker omnibus számlák |

| Külön kereskedési limit (STL) |

*A csatlakozott számláknak teljesíteniük kell a fedezeti számlákra vagy készpénzes számlákra vonatkozó minimális tőkekövetelményt.

Az IB Japan, IB Europe SARL, IBKR Australia és IB India ügyfelei nem jogosultak részt venni a programban. A számlájukat az IB LLC-nél vezető japán és indiai ügyfelek jogosultak részt venni a programban.

Emellett részt vehetnek a programban a fenti követelményeket teljesítő Pénzügyi tanácsadói ügyfélszámlák, a teljesen nyilvános IBroker ügyfelek és az Omnibus brókerek. Pénzügyi tanácsadók és teljesen nyilvános IBrokerek esetén maguknak az ügyfeleknek kell aláírniuk a szerződést. Omnibus brókerek esetén a bróker írja alá a szerződést.

Az IRA számlák jogosultak részt venni a Részvényhozam-növelő programban?

Igen.

Az IRA számlák Interactive Brokers Asset Management által kezelt részszámlái jogosultak részt venni a Részvényhozam-növelő programban?

Nem.

A UK SIPP számlák jogosultak részt venni a Részvényhozam-növelő programban?

Nem.

Mi történik olyankor, ha egy programban részt vevő készpénzes számla tőkéje az 50 000 USD jogosultsági küszöbérték alá csökken?

A készpénzes számlának kizárólag a programhoz történő csatlakozás időpontjában kell teljesítenie a minimális tőkekövetelményt. Ha a tőke ezt követően csökken ezen szint alá, az nem befolyásolja a meglévő vagy jövőbeli értékpapír-kölcsönzési tevékenységet.

Hogyan lehet csatlakozni az IBKR Részvényhozam-növelő programjához?

A csatlakozáshoz kérjük, jelentkezzen be az Ügyfélportálra. A bejelentkezést követően kattintson a Felhasználó menüre (a jobb felső sarokban található fej és váll ikon), majd a Beállítások opcióra. Ezután a Számlabeállítások menüpontban keresse meg a Kereskedés pontot és a csatlakozáshoz kattintson a Részvényhozam-növelő programra. Ezután megkapja a programhoz történő csatlakozáshoz szükséges űrlapokat és tájékoztatókat. Miután átnézte és aláírta az űrlapokat, a kérelme feldolgozásra kerül. A programhoz történő csatlakozás aktiválási ideje 24-48 óra.

Hogyan lehet megszüntetni a Részvényhozam-növelő programban való részvételt?

A kilépéshez kérjük, jelentkezzen be az Ügyfélportálra. A bejelentkezést követően kattintson a Felhasználó menüre (a jobb felső sarokban található fej és váll ikon), majd a Beállítások opcióra. A Számlabeállítások menüpontban keresse meg a Kereskedés pontot, majd kattintson a Részvényhozam-növelő programra, és kövesse a megjelenő utasításokat. Ezután nyújtsa be a kérelmét feldolgozásra. A kilépési kérelmek általában a nap végéig feldolgozásra kerülnek.

Ha egy számla csatlakozik a programhoz, majd később kilép a programból, akkor mikor csatlakozhat újra?

A kilépést követően a számla 90 naptári napig nem csatlakozhat újra a programhoz.

Milyen típusú értékpapír-pozíciókat lehet kölcsönadni?

| US piaci | EU piaci | HK piaci | CAD piaci |

| Törzsrészvény (tőzsdén jegyzett, PINK és OTCBB) | Törzsrészvény (tőzsdén jegyzett) | Törzsrészvény (tőzsdén jegyzett) | Törzsrészvény (tőzsdén jegyzett) |

| ETF | ETF | ETF | ETF |

| Elsőbbségi részvény | Elsőbbségi részvény | Elsőbbségi részvény | Elsőbbségi részvény |

| Vállalati kötvények* |

* Az önkormányzati kötvények kivételével.

Vonatkozik-e bármilyen korlátozás azon részvények kölcsönzésére, amelyekkel az IPO-t követően a másodlagos piacon kereskednek?

Nem, feltéve, hogy a számlán tartott kölcsönözhető értékpapírok nem esnek semmilyen korlátozás alá.

Hogyan határozza meg az IBKR a kölcsönözhető részvények számát?

Az első lépés az esetleges olyan értékpapírok értékének a meghatározása, amelyeken az IBKR fedezeti zálogjogot tart fenn, és amelyeket az ügyfél Részvényhozam-növelő programban való részvétele nélkül is kölcsönbe adhat. A szabályok értelmében az a bróker, aki az ügyfelei értékpapír-vásárlásait fedezeti hitelből finanszírozza, az ilyen ügyfelek értékpapírjait kölcsönadhatja vagy biztosítékként felajánlhatja a készpénz tartozik egyenleg 140%-ának megfelelő összegig. Ha például egy 50 000 USD készpénz egyenleggel rendelkező ügyfél 100 000 USD piaci értékű értékpapírokat vásárol, akkor a tartozik vagy hitel egyenlege 50 000 USD lesz, és a bróker ezen egyenleg 140%-án, azaz 70 000 USD értékű értékpapíron rendelkezik zálogjoggal. A fenti összeget meghaladóan az ügyfél tulajdonában lévő értékpapírok megnevezése „fedezeten túli értékpapírok” (a fenti példában 30 000 USD), amelyeket elkülönítetten kell kezelni, hacsak az ügyfél nem hatalmazza fel az IBKR-t, hogy kölcsönadja az ilyen értékpapírokat a Részvényhozam-növelő program keretében.

A tartozik egyenleg meghatározása úgy történik, hogy először minden nem USD-ben denominált készpénz egyenleget át kell váltani USD-re, majd ebből le kell vonni minden esetleges short részvényeladás hozamát (szükség esetén az USD-re váltást követően). Ha az eredmény negatív, akkor ennek a negatív számnak a 140%-át felszabadítjuk. Nem vesszük figyelembe továbbá az árutőzsdei illetve az azonnali fémpiaci és CFD szegmensben tartott készpénz egyenlegeket. Részletesebb információkért kérjük, kattintson ide.

1. PÉLDA: Az ügyfél 100 000 EUR értékű long pozícióval rendelkezik egy USD alapdevizájú számlán, és az EUR.USD árfolyam 1,40. Az ügyfél USD-ben denominált részvényeket vásárol 112 000 USD (azaz 80 000 EUR-nak megfelelő) értékben. Minden teljes egészében befizetettnek minősülő értékpapír figyelembe vehető a készpénz egyenlegben.

| Komponens | EUR | USD | Alap (USD) |

| Készpénz | 100 000 | (112 000) | 28 000 USD |

| Long részvény | 112 000 USD | 112 000 USD | |

| NLV | 140 000 USD |

2. PÉLDA: Az ügyfél 80 000 USD értékű long pozícióval, 100 000 USD értékű USD-ben denominált long részvénypozícióval és 100 000 USD értékű USD-ben denominált short részvény pozícióval rendelkezik. Ebben az esetben összesen 28 000 USD értékű long értékpapír minősül fedezeti értékpapírnak, és a fennmaradó 72 000 USD minősül fedezeten túli értékpapírnak. A számítás menete: a készpénz-egyenlegből levonjuk a short részvényhozamot (80 000 USD - 100 000 USD), majd a negatív eredményt megszorozzuk 140%-kal (20 000 USD x 1,4 = 28 000 USD)

| Komponens | Alap (USD) |

| Készpénz | 80 000 USD |

| Long részvény | 100 000 USD |

| Short részvény | (100 000 USD) |

| NLV | 80 000 USD |

Az IBKR minden kölcsönözhető részvényt kölcsönbe ad?

Nem garantálható, hogy egy adott számlán lévő valamennyi kölcsönözhető részvényt kölcsön fogjuk adni a Részvényhozam-növelő program keretében, mivel lehetséges, hogy (i) a piaci kamatfeltételek nem kedveznek egyes értékpapíroknak, (ii) az IBKR nem fér hozzá olyan piachoz, ahol vannak a kölcsön iránt érdeklődő szereplők, vagy (iii) az IBKR nem akarja kölcsönbe adni az Ön részvényeit.

A Részvényhozam-növelő program keretében nyújtott értékpapír-kölcsönöket kizárólag 100-as lépésekben nyújtják?

Nem. A kölcsönök tetszőleges egész számú részvényben nyújthatók, bár külső feleknek csak a 100 többszöröseinek megfelelő számú részvényt adunk kölcsön. Így lehetséges, hogy egy 100 részvényre irányuló külső kölcsönigény kielégítése érdekében egy ügyféltől 75 részvényt, egy másik ügyféltől pedig 25 részvényt adunk kölcsön.

Hogyan allokálják a kölcsönöket az ügyfelek között, amikor a kölcsönözhető részvények száma meghaladja a kölcsönigény mértékét?

Amennyiben egy adott részvény kölcsönzése iránti igény elmarad a Részvényhozam-növelő programban részt vevő ügyfelek tulajdonában lévő kölcsönözhető részvények számától, a kölcsön allokálása arányosan történik. Ha például a Részvényhozam-növelő programban összesen 20 000 db kölcsönözhető XYZ részvény áll rendelkezésre, a kölcsönzési igény pedig 10 000 XYZ részvény, akkor minden ügyfél a kölcsönözhető részvényei 50%-át fogja kölcsönadni.

A részvényeket kizárólag más IBKR ügyfeleknek, vagy harmadik feleknek is kölcsönadják?

A részvények IBKR ügyfeleknek és harmadik feleknek is kölcsönadhatók.

Eldöntheti-e a Részvényhozam-növelő programban részt vevő ügyfél, hogy melyik részvényeit adhatja kölcsön az IBKR?

Nem. a programot teljes egészében az IBKR kezeli, aki – miután meghatározza azokat az értékpapírokat, amelyeket egy fedezeti hitelzálog keretében kölcsönadhat – saját hatáskörben dönti el, hogy melyik teljes egészében befizetett vagy fedezeten túli értékpapír adható kölcsönbe.

Vonatkozik-e bármilyen korlátozás a Részvényhozam-növelő program keretében kölcsönadott értékpapírok értékesítésére?

A kölcsönbe adott részvények bármikor, korlátozás nélkül értékesíthetők. A részvényeket nem szükséges visszaszolgáltatni az értékesítés elszámolásának időpontjáig, és az értékesítésből származó bevétel a szokásos elszámolási napon kerül jóváírásra az ügyfél számláján. Emellett a kölcsön az értékpapír értékesítésének napját követő munkanapi piacnyitáskor szűnik meg.

Használhatja-e az ügyfél a Részvényhozam-növelő program keretében kölcsönbe adott részvényeket fedezett eladási opció kiírására, és részesedhet-e a fedezett eladási opció szerinti fedezeti elbánásban?

Igen. Egy részvény kölcsönbe adása nem befolyásolja az arra vonatkozó fedezeti követelményeket, mivel továbbra is a kölcsönbe adó élvezi/viseli a kölcsönbe adott pozícióval kapcsolatos nyereségeket/veszteségeket.

Mi történik egy kölcsönbe adott részvénnyel, amire később vételi vagy eladási opciót érvényesítenek?

A kölcsön a pozíciót lezáró vagy csökkentő tranzakció (kötés, lehívás, gyakorlás) napját követő napon (T+1) szűnik meg.

Mi történik egy kölcsönbe adott részvénnyel, aminek később felfüggesztik a kereskedését?

A felfüggesztés közvetlenül nem befolyásolja a részvény kölcsönözhetőségét, tehát amíg az IBKR a részvényeket kölcsönözni tudja, addig a kölcsön hatályban marad, függetlenül a kereskedése felfüggesztésétől.

Át lehet-e csoportosítani egy kölcsön biztosítékát az árupiaci szegmensbe fedezeti és/vagy változási okokból?

Nem. A kölcsön biztosítéka soha nem befolyásolja a fedezetet vagy a finanszírozást.

Mi történik, ha a program egyik résztvevője fedezeti hitelt kíván felvenni vagy megnöveli a már meglévő hitele egyenlegét?

Amennyiben egy ügyfél teljes egészében befizetett, és a Részvényhozam-növelő program keretében kölcsönadott értékpapírokat tart, majd ezt követően fedezeti hitelt vesz fel, a hitel megszüntetésre kerül, amennyiben az értékpapírok nem minősülnek fedezeten túli értékpapírnak. Hasonlóképpen, ha egy a program keretében kölcsönadott többletfedezeti értékpapírokat tartó ügyfél megnöveli a meglévő fedezeti hitele egyenlegét, a hitel ebben az esetben is megszüntetésre kerülhet, amennyiben az értékapírok már nem minősülnek fedezeten túli értékpapírnak.

Milyen esetekben szűnik meg egy részvénykölcsön?

A részvénykölcsön megszűnik az alábbi esetek bármelyikében (nem kizárólagos felsorolás):

- Ha az ügyfél úgy dönt, hogy kilép a programból

- Részvények átruházása

- Bizonyos összegű hitelfelvétel a részvények terhére

- Részvények értékesítése

- Vételi/eladási opció gyakorlása

- Számlazárás

Do participants in the Stock Yield Enhancement Program receive dividends on shares loaned?

Stock Yield Enhancement Program shares that are lent out are generally recalled from the borrower before ex-date in order to capture the dividend and avoid payments in lieu (PIL) of dividends. A részvények tulajdonosa ennek ellenére is jogosult lehet PIL-re.

Megmarad-e a Részvényhozam-növelő programban részt vevő ügyfelek szavazati joga a kölcsönadott részvények tekintetében?

Nem. Az értékpapírok kölcsönbe vevőjének joga van szavazni vagy hozzájárulást adni az értékpapírokkal kapcsolatban, ha a szavazásra, a hozzájárulás megadására vagy az egyéb intézkedések megtételére vonatkozó fordulónap vagy határidő a kölcsön futamidejére esik.

Kapnak-e jogokat, warrantokat és kiválási részvényeket a Részvényhozam-növelő programban részt vevő ügyfelek a kölcsönadott részvényeik után?

Igen. Az értékpapír kölcsönbe adója jogosult az értékpapírokkal kapcsolatos minden és bármely jogra, warrantra, kiválási részvényre és felosztásra.

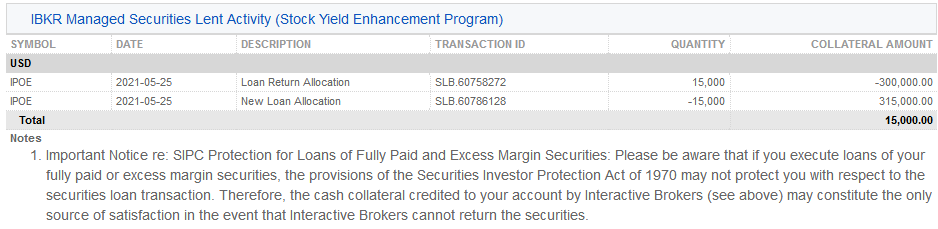

Hogyan jelenik meg a kölcsönzés az aktivitási kimutatásban?

A kölcsön biztosítéka, a kölcsönbe adott részvények, az aktivitás és a jövedelem a kimutatás alábbi 6 pontjában jelenik meg:

1. Részletes készpénz adatok – a nyitó biztosítéki (amerikai államkötvény vagy készpénz) egyenleg, a kölcsönzési tevékenységből eredő nettó változás (új kölcsön esetén pozitív, a kölcsönállomány csökkenése esetén negatív) és a záró biztosítéki egyenleg részletes adatait tartalmazza.

2. Nettó részvénypozíció összefoglaló – minden egyes részvény vonatkozásában tartalmazza az IBKR-nél tartott összes részvény, valamint a kölcsönbe vett illetve kölcsönbe adott részvények darabszámát, és a nettó részvénypozíciót (azaz: IBKR-nél tartott részvények + kölcsönbe vett részvények - kölcsönbe adott részvények).

3. Az IBKR által kezelt, kölcsönbe adott értékpapírok (Részvényhozam-növelő program) – a Részvényhozam-növelő program keretében kölcsönbe adott minden egyes részvény vonatkozásában felsorolja a részvények mennyiségét és a kamatlábat (%).

3a. Az IBKR által kezelt értékpapírok, IBSS által nyilvántartott biztosítékok (Részvényhozam-növelő program) – az IBLLC ügyfelei egy további sort is találnak a kimutatásukon, ami a biztosítékként tartott konkrét amerikai államkötvények megnevezését, mennyiségét, árfolyamát és teljes biztosítéki értékét tartalmazza.

4. Az IBKR által kezelt kölcsönbe adott értékpapírokkal folytatott műveletek (Részvényhozam-növelő program) – az egyes értékpapírok kölcsönzésének részletes adatait tartalmazza, ideértve a kölcsönzésből visszavett értékpapírok allokációját (azaz a megszűnt kölcsönöket), az új kölcsönallokációkat (azaz az újonnan létrejött kölcsönöket), a részvények mennyiségét, a nettó kamatlábat (%), az ügyfél biztosíték kamatlábát (%) és a biztosíték összegét.

5. Az IBKR által kezelt kölcsönbe adott értékpapírokkal folytatott műveletek kamatainak részletes adatai (Részvényhozam-növelő program) – az egyes kölcsönök részletes adatait tartalmazza, úgymint: az IBKR által realizált kamatláb (%), az IBKR által realizált bevétel (az IBKR által a kölcsönügyleten elért teljes bevétel, azaz {biztosíték összege x kamatláb}/360), az ügyfélbiztosíték kamatlába (ami megközelítőleg az IB által a kölcsönön realizált bevétel felét jelenti), és az ügyfélnek fizetett kamat (ami az ügyfélbiztosítékon realizált kamatbevételt jelenti)

Megjegyzés: ez a sor csak akkor jelenik meg, ha a tárgyidőszakban az ügyfél által realizált felhalmozott kamat összege meghaladja az 1 USD-t.

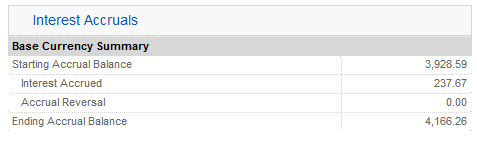

6. Elhatárolt kamatok – a kamatbevétel ezen a soron elhatárolt kamatként jelenik meg, és minden más elhatárolt kamat tétellel azonos elbánásban részesül (azaz összesítjük, de csak abban az esetben tüntetjük fel elhatárolásként, ha meghaladja az 1 USD-t, és havonta feladjuk a készpénzbe). Év végi beszámolási célokra ezt a kamatbevételt az amerikai adófizetők számára kiadott 1099-es nyomtatványon mutatjuk ki.

Allocation of Partial Fills

How are executions allocated when an order receives a partial fill because an insufficient quantity is available to complete the allocation of shares/contracts to sub-accounts?

Overview:

From time-to-time, one may experience an allocation order which is partially executed and is canceled prior to being completed (i.e. market closes, contract expires, halts due to news, prices move in an unfavorable direction, etc.). In such cases, IB determines which customers (who were originally included in the order group and/or profile) will receive the executed shares/contracts. The methodology used by IB to impartially determine who receives the shares/contacts in the event of a partial fill is described in this article.

Background:

Before placing an order CTAs and FAs are given the ability to predetermine the method by which an execution is to be allocated amongst client accounts. They can do so by first creating a group (i.e. ratio/percentage) or profile (i.e. specific amount) wherein a distinct number of shares/contracts are specified per client account (i.e. pre-trade allocation). These amounts can be prearranged based on certain account values including the clients’ Net Liquidation Total, Available Equity, etc., or indicated prior to the order execution using Ratios, Percentages, etc. Each group and/or profile is generally created with the assumption that the order will be executed in full. However, as we will see, this is not always the case. Therefore, we are providing examples that describe and demonstrate the process used to allocate partial executions with pre-defined groups and/or profiles and how the allocations are determined.

Here is the list of allocation methods with brief descriptions about how they work.

· AvailableEquity

Use sub account’ available equality value as ratio.

· NetLiq

Use subaccount’ net liquidation value as ratio

· EqualQuantity

Same ratio for each account

· PctChange1:Portion of the allocation logic is in Trader Workstation (the initial calculation of the desired quantities per account).

· Profile

The ratio is prescribed by the user

· Inline Profile

The ratio is prescribed by the user.

· Model1:

Roughly speaking, we use each account NLV in the model as the desired ratio. It is possible to dynamically add (invest) or remove (divest) accounts to/from a model, which can change allocation of the existing orders.

Basic Examples:

Details:

CTA/FA has 3-clients with a predefined profile titled “XYZ commodities” for orders of 50 contracts which (upon execution) are allocated as follows:

Account (A) = 25 contracts

Account (B) = 15 contracts

Account (C) = 10 contracts

Example #1:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 10 am (ET) the order begins to execute2but in very small portions and over a very long period of time. At 2 pm (ET) the order is canceled prior to being executed in full. As a result, only a portion of the order is filled (i.e., 7 of the 50 contracts are filled or 14%). For each account the system initially allocates by rounding fractional amounts down to whole numbers:

Account (A) = 14% of 25 = 3.5 rounded down to 3

Account (B) = 14% of 15 = 2.1 rounded down to 2

Account (C) = 14% of 10 = 1.4 rounded down to 1

To Summarize:

A: initially receives 3 contracts, which is 3/25 of desired (fill ratio = 0.12)

B: initially receives 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: initially receives 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The system then allocates the next (and final) contract to an account with the smallest ratio (i.e. Account C which currently has a ratio of 0.10).

A: final allocation of 3 contracts, which is 3/25 of desired (fill ratio = 0.12)

B: final allocation of 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: final allocation of 2 contract, which is 2/10 of desired (fill ratio = 0.20)

The execution(s) received have now been allocated in full.

Example #2:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 11 am (ET) the order begins to be filled3 but in very small portions and over a very long period of time. At 1 pm (ET) the order is canceled prior being executed in full. As a result, only a portion of the order is executed (i.e., 5 of the 50 contracts are filled or 10%).For each account, the system initially allocates by rounding fractional amounts down to whole numbers:

Account (A) = 10% of 25 = 2.5 rounded down to 2

Account (B) = 10% of 15 = 1.5 rounded down to 1

Account (C) = 10% of 10 = 1 (no rounding necessary)

To Summarize:

A: initially receives 2 contracts, which is 2/25 of desired (fill ratio = 0.08)

B: initially receives 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: initially receives 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The system then allocates the next (and final) contract to an account with the smallest ratio (i.e. to Account B which currently has a ratio of 0.067).

A: final allocation of 2 contracts, which is 2/25 of desired (fill ratio = 0.08)

B: final allocation of 2 contracts, which is 2/15 of desired (fill ratio = 0.134)

C: final allocation of 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The execution(s) received have now been allocated in full.

Example #3:

CTA/FA creates a DAY order to buy 50 Sept 2016 XYZ future contracts and specifies “XYZ commodities” as the predefined allocation profile. Upon transmission at 11 am (ET) the order begins to be executed2 but in very small portions and over a very long period of time. At 12 pm (ET) the order is canceled prior to being executed in full. As a result, only a portion of the order is filled (i.e., 3 of the 50 contracts are filled or 6%). Normally the system initially allocates by rounding fractional amounts down to whole numbers, however for a fill size of less than 4 shares/contracts, IB first allocates based on the following random allocation methodology.

In this case, since the fill size is 3, we skip the rounding fractional amounts down.

For the first share/contract, all A, B and C have the same initial fill ratio and fill quantity, so we randomly pick an account and allocate this share/contract. The system randomly chose account A for allocation of the first share/contract.

To Summarize3:

A: initially receives 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: initially receives 0 contracts, which is 0/15 of desired (fill ratio = 0.00)

C: initially receives 0 contracts, which is 0/10 of desired (fill ratio = 0.00)

Next, the system will perform a random allocation amongst the remaining accounts (in this case accounts B & C, each with an equal probability) to determine who will receive the next share/contract.

The system randomly chose account B for allocation of the second share/contract.

A: 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: 0 contracts, which is 0/10 of desired (fill ratio = 0.00)

The system then allocates the final [3] share/contract to an account(s) with the smallest ratio (i.e. Account C which currently has a ratio of 0.00).

A: final allocation of 1 contract, which is 1/25 of desired (fill ratio = 0.04)

B: final allocation of 1 contract, which is 1/15 of desired (fill ratio = 0.067)

C: final allocation of 1 contract, which is 1/10 of desired (fill ratio = 0.10)

The execution(s) received have now been allocated in full.

Available allocation Flags

Besides the allocation methods above, user can choose the following flags, which also influence the allocation:

· Strict per-account allocation.

For the initially submitted order if one or more subaccounts are rejected by the credit checking, we reject the whole order.

· “Close positions first”1.This is the default handling mode for all orders which close a position (whether or not they are also opening position on the other side or not). The calculation are slightly different and ensure that we do not start opening position for one account if another account still has a position to close, except in few more complex cases.

Other factor affects allocations:

1) Mutual Fund: the allocation has two steps. The first execution report is received before market open. We allocate based onMonetaryValue for buy order and MonetaryValueShares for sell order. Later, when second execution report which has the NetAssetValue comes, we do the final allocation based on first allocation report.

2) Allocate in Lot Size: if a user chooses (thru account config) to prefer whole-lot allocations for stocks, the calculations are more complex and will be described in the next version of this document.

3) Combo allocation1: we allocate combo trades as a unit, resulting in slightly different calculations.

4) Long/short split1: applied to orders for stocks, warrants or structured products. When allocating long sell orders, we only allocate to accounts which have long position: resulting in calculations being more complex.

5) For non-guaranteed smart combo: we do allocation by each leg instead of combo.

6) In case of trade bust or correction1: the allocations are adjusted using more complex logic.

7) Account exclusion1: Some subaccounts could be excluded from allocation for the following reasons, no trading permission, employee restriction, broker restriction, RejectIfOpening, prop account restrictions, dynamic size violation, MoneyMarketRules restriction for mutual fund. We do not allocate to excluded accountsand we cancel the order after other accounts are filled. In case of partial restriction (e.g. account is permitted to close but not to open, or account has enough excess liquidity only for a portion of the desired position).

Footnotes:

Overview of IBKR issued Share CFDs

The following article is intended to provide a general introduction to share-based Contracts for Differences (CFDs) issued by IBKR.

For Information on IBKR Index CFDs click here. For Forex CFDs click here. For Precious Metals click here.

Topics covered are as follows:

I. CFD Definition

II. Comparison Between CFDs and Underlying Shares

III. CFD Tax and Margin Advantage

IV. US ETFs

V. CFD Resources

VI. Frequently Asked Questions

Risk Warning

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage.

61% of retail investor accounts lose money when trading CFDs with IBKR.

You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

ESMA Rules for CFDs (Retail Clients of IBKRs European entities, including so-called F segments)

The European Securities and Markets Authority (ESMA) has enacted new CFD rules effective 1st August 2018.

The rules include: 1) leverage limits on the opening of a CFD position; 2) a margin close out rule on a per account basis; and 3) negative balance protection on a per account basis.

The ESMA Decision is only applicable to retail clients. Professional clients are unaffected.

Please refer to the following articles for more detail:

ESMA CFD Rules Implementation at IBKR (UK) and IBKR LLC

ESMA CFD Rules Implementation at IBIE and IBCE

I. Overview

IBKR CFDs are OTC contracts which deliver the return of the underlying stock, including dividends and corporate actions (read more about CFD corporate actions).

Said differently, it is an agreement between the buyer (you) and IBKR to exchange the difference in the current value of a share, and its value at a future time. If you hold a long position and the difference is positive, IBKR pays you. If it is negative, you pay IBKR.

Our Share CFDs offer Direct Market Access (DMA). Our Share CFD quotes are identical to the Smart-routed quotes for shares that you can observe in the Trader Workstation. Similar to shares, your non-marketable (i.e. limit) orders have the underlying hedge directly represented on the deep book of those exchanges at which it trades. This also means that you can place orders to buy the CFD at the underlying bid and sell at the offer.

To compare IBKR’s transparent CFD model to others available in the market please see our Overview of CFD Market Models.

We currently offer approximately 8500 Share CFDs covering the principal markets in the US, Europe and Asia. Eligible shares have minimum market capitalization of USD 500 million and median daily trading value of at least USD 600 thousand. Please see CFD Product Listings for more detail.

Most order types are available for CFDs, including auction orders and IBKR Algos.

CFDs on US share can also be traded during extended exchange hours and overnight. Other CFDs are traded during regular hours.

II. Comparison Between CFDs and Underlying Shares

Depending on your trading objectives and trading style, CFDs offer a number of advantages compared to stocks, but also some disadvantages:

| BENEFITS of IBKR CFDs | DRAWBACKS of IBKR CFDs |

|---|---|

| No stamp duty or financial transaction tax (UK, France, Belgium, Spain) | No ownership rights |

| Generally lower margin rates than shares* | Complex corporate actions may not always be exactly replicable |

| Tax treaty rates for dividends without need for reclaim | Taxation of gains may differ from shares (please consult your tax advisor) |

| Exemption from day trading rules | |

| US ETFs tradable as CFDs** |

*IB LLC and IB-UK accounts.

**EEA area clients cannot trade US ETFs directly, as they do not publish KIDs.

III. CFD Tax and Margin Advantage

Where stamp duty or financial transaction tax is applied, currently in the UK (0.5%), France (0.3%), Belgium (0.35%) and Spain (0.2%), it has a substantially detrimental impact on returns, particular in an active trading strategy. The taxes are levied on buy-trades, so each time you open a long, or close a short position, you will incur tax at the rates described above.

The amount of available leverage also significantly impacts returns. For European IBKR entities, margin requirements are risk-based for both stocks and CFDs, and therefore generally the same. IB-UK and IB LLC accounts however are subject to Reg T requirements, which limit available leverage to 2:1 for positions held overnight.

To illustrate, let's assume that you have 20,000 to invest and wish to leverage your investment fully. Let's also assume that you hold your positions overnight and that you trade in and out of positions 5 times in a month.

Let's finally assume that your strategy is successful and that you have earned a 5% return on your gross (fully leveraged) investment.

The table below shows the calculation in detail for a UK security. The calculations for France, Belgium and Spain are identical, except for the tax rates applied.

| UK CFD | UK Stock | UK Stock | |

|---|---|---|---|

| All Entities |

EU Account

|

IB LLC or IBUK Acct

|

|

| Tax Rate | 0% | 0.50% | 0.50% |

| Tax Basis | N/A | Buy Orders | Buy Orders |

| # of Round trips | 5 | 5 | 5 |

| Commission rate | 0.05% | 0.05% | 0.05% |

| Overnight Margin | 20% | 20% | 50% |

| Financing Rate | 1.508% | 1.508% | 1.508% |

| Days Held | 30 | 30 | 30 |

| Gross Rate of Return | 5% | 5% | 5% |

| Investment | 100,000 | 100,000 | 40,000 |

| Amount Financed | 100,000 | 80,000 | 20,000 |

| Own Capital | 20,000 | 20,000 | 20,000 |

| Tax on Purchase | 0.00 | 2,500.00 | 1,000.00 |

| Round-trip Commissions | 500.00 | 500.00 | 200.00 |

| Financing | 123.95 | 99.16 | 24.79 |

| Total Costs | 623.95 | 3099.16 | 1224.79 |

| Gross Return | 5,000 | 5,000 | 2,000 |

| Return after Costs | 4,376.05 | 1,900.84 | 775.21 |

| Difference | -57% | -82% |

The following table summarizes the reduction in return for a stock investment, by country where tax is applied, compared to a CFD investment, given the above assumptions.

| Stock Return vs cfD | Tax Rate | EU Account | IB LLC or IBUK Acct |

|---|---|---|---|

| UK | 0.50% | -57% | -82% |

| France | 0.30% | -34% | -73% |

| Belgium | 0.35% | -39% | -75% |

| Spain | 0.20% | -22% | -69% |

IV. US ETFs

EEA area residents who are retail investors must be provided with a key information document (KID) for all investment products. US ETF issuers do not generally provide KIDs, and US ETFs are therefore not available to EEA retail investors.

CFDs on such ETFs are permitted however, as they are derivatives for which KIDs are available.

Like for all share CFDs, the reference price for CFDs on ETFs is the exchange-quoted, SMART-routed price of the underlying ETF, ensuring economics that are identical to trading the underlying ETF.

V. Extended and Overnight Hours

US CFDs can be traded from 04:00 to 20:00EST, and the again overnight from 20:00 to 03:30 the following day. Trades in the overnight session are attributed to the day when the session ends, even if a trade is entered before midnight the previous day. This has implications for corporate actions and financing.

Trades entered before midnight on the day before ex-date will not have a dividend entitlement. Trades before midnight will settle as if they had been traded the following day, delaying the start of financing.

VI. CFD Resources

Below are some useful links with more detailed information on IBKR’s CFD offering:

The following video tutorial is also available:

How to Place a CFD Trade on the Trader Workstation

VII. Frequently Asked Questions

What Stocks are available as CFDs?

Large and Mid-Cap stocks in the US, Western Europe, Nordic and Japan. Liquid Small Cap stocks are also available in many markets. Please see CFD Product Listings for more detail. More countries will be added in the near future.

Do you have CFDs on other asset classes?

Yes. Please see IBKR Index CFDs - Facts and Q&A, Forex CFDs - Facts and Q&A and Metals CFDs - Facts and Q&A.

How do you determine your Share CFD quotes?

IBKR CFD quotes are identical to the Smart routed quotes for the underlying share. IBKR does not widen the spread or hold positions against you. To learn more please go to Overview of CFD Market Models.

Can I see my limit orders reflected on the exchange?

Yes. IBKR offers Direct market Access (DMA) whereby your non-marketable (i.e. limit) orders have the underlying hedges directly represented on the deep books of the exchanges on which they trade. This also means that you can place orders to buy the CFD at the underlying bid and sell at the offer. In addition, you may also receive price improvement if another client's order crosses yours at a better price than is available on public markets.

How do you determine margins for Share CFDs?

IBKR establishes risk-based margin requirements based on the historical volatility of each underlying share. The minimum margin is 10%, making CFDs more margin-efficient than trading the underlying share in many cases. Retail investors are subject to additional margin requirements mandated by the European regulators. There are no portfolio off-sets between individual CFD positions or between CFDs and exposures to the underlying share. Concentrated positions and very large positions may be subject to additional margin. Please refer to CFD Margin Requirements for more detail.

Are short Share CFDs subject to forced buy-in?

Yes. In the event the underlying stock becomes difficult or impossible to borrow, the holder of the short CFD position may become subject to buy-in.

How do you handle dividends and corporate actions?

IBKR will generally reflect the economic effect of the corporate action for CFD holders as if they had been holding the underlying security. Dividends are reflected as cash adjustments, while other actions may be reflected through either cash or position adjustments, or both. For example, where the corporate action results in a change of the number of shares (e.g. stock-split, reverse stock split), the number of CFDs will be adjusted accordingly. Where the action results in a new entity with listed shares, and IBKR decides to offer these as CFDs, then new long or short positions will be created in the appropriate amount. For an overview please CFD Corporate Actions.

*Please note that in some cases it may not be possible to accurately adjust the CFD for a complex corporate action such as some mergers. In these cases IBKR may terminate the CFD prior to the ex-date.

Can anyone trade IBKR CFDs?

All clients can trade IBKR CFDs, except residents of the USA, Canada, Hong Kong, New Zealand and Israel. There are no exemptions based on investor type to the residency based exclusions.

What do I need to do to start trading CFDs with IBKR?

You need to set up trading permission for CFDs in Client Portal, and agree to the relevant disclosures. If your account is with IBKR (UK) or with IBKR LLC, IBKR will then set up a new account segment (identified with your existing account number plus the suffix “F”). Once the set-up is confirmed you can begin to trade. You do not need to fund the F-account separately, funds will be automatically transferred to meet CFD initial margin requirements from your main account.

If your account is with another IBKR entity, only the permission is required; an additional account segment is not necessary.

Are there any market data requirements?

The market data for IBKR Share CFDs is the market data for the underlying shares. It is therefore necessary to have market data permissions for the relevant exchanges. If you already have market data permissions for an exchange for trading the shares, you do not need to do anything. If you want to trade CFDs on an exchange for which you do not currently have market data permissions, you can set up the permissions in the same way as you would if you planned to trade the underlying shares.

How are my CFD trades and positions reflected in my statements?

If you are a client of IBKR (U.K.) or IBKR LLC, your CFD positions are held in a separate account segment identified by your primary account number with the suffix “F”. You can choose to view Activity Statements for the F-segment either separately or consolidated with your main account. You can make the choice in the statement window in Client Portal.

If you are a client of other IBKR entities, there is no separate segment. You can view your positions normally alongside your non-CFD positions.

Can I transfer in CFD positions from another broker?

IBKR does not facilitate the transfer of CFD positions at this time.

Are charts available for Share CFDs?

Yes.

In what type of IBKR accounts can I trade CFDs e.g., Individual, Friends and Family, Institutional, etc.?

All margin and cash accounts are eligible for CFD trading.

What are the maximum a positions I can have in a specific CFD?

There is no pre-set limit. Bear in mind however that very large positions may be subject to increased margin requirements. Please refer to CFD Margin Requirements for more detail.

Can I trade CFDs over the phone?

No. In exceptional cases we may agree to process closing orders over the phone, but never opening orders.

IBKR Stock Yield Enhancement Program

PROGRAM OVERVIEW

The Stock Yield Enhancement Program provides the opportunity to earn extra income on the fully-paid shares of stock held in your account by allowing IBKR to borrow shares from you in exchange for collateral (either U.S. Treasuries or cash), and then lend the shares to traders who want to sell them short and are willing to pay interest to borrow them. For additional information on the Stock Yield Enhancement Program please see here or review the Frequently Asked Questions page.

HOW TO ENROLL IN THE STOCK YIELD ENHANCEMENT PROGRAM

To enroll, please login to the Client Portal. Once logged in, click the User menu (head and shoulders icon in the top right corner) followed by Settings.

In the Trading section of the Settings page, click the link for the Stock Yield Enhancement Program. Select the checkbox on the next screen and click Continue. You will then be presented with the requisite forms and disclosures needed to enroll in the program. Once you have reviewed and signed the forms, your request will be submitted for processing. Please allow 24-48 hours for enrollment to become active.

.png)

.png)

India Intra-Day Shorting Risk Disclosure

Interactive Brokers currently offers the ability to short sell stocks before taking delivery on an intra-day basis. In accordance with IB’s intra-day shorting rules, traders are required to deliver shares sold or close short stock positions prior to the end of the trading session.

Should traders establish a short stock position intra-day and still hold the position ten minutes prior to the end of the trading session at 15:20 IST, Interactive Brokers may, on a best efforts basis, close the position on your behalf. If the position is not closed by the end of the day and the shares are not delivered by the customer before settlement, the loss on account of auction will be borne by the customer. Please note that prices in the auction market are highly variable and typically not favorable compared to the normal market.

It is important to note, IB will not take into consideration any closing orders for short stock positions placed by the customer which may still be working. If your account holds a short position ten minutes prior to the end of the trading session and you have placed working orders to close those positions, there is the possibility your closing order will execute and that IB will act to close out your short position. In this situation you will be responsible for both executions and will need to manage your long position accordingly.

A fee of INR 2,000 will be charged for this manual processing in addition to any external penalties in the case of short stock positions resulting in auction trades. As such, we strongly urge customers to monitor their positions and take appropriate action themselves in order to avoid this.

When I short a stock, when will the hard to borrow interest begin accruing?

Short positions will have a borrow interest/fee associated with them.

Borrow interest will begin being charged on a short position from short settlement date to buy-to-cover settlement date.

For example, you sell XYZ on Monday, and you close the position on Tuesday. Borrow interest would start to be charged upon Wednesday's settlement date (T+2). Interest would cease to be charged on Thursday, the settlement date (T+2) of the buy-to-cover order.

Why do I receive a notice of a potential buy-in of my short position when your Short Stock Availability List is showing shares available to borrow?

As background, the short stock availability list represents the inventory of shares which IBKR has available to lend and which other brokers have indicated that they have available to lend. While it is updated on a near real-time basis throughout the day for changes to IBKR's inventory and periodically throughout the day to reflect updates to the availability lists of other brokers, many brokers provide updates only once per day.

It should be noted that the purpose of the short stock availability list is to meet the broker's regulatory obligation that they have made a reasonable determination that a security can be borrowed in time for settlement three business days later. There is no regulatory requirement, in most instances, that the broker pre-borrow shares to effect delivery on a short sale prior to settlement and the requirement which this list serves to address is completely separate from the SEC rules which require that the broker force-close any short position having a delivery obligation subject to fail with the clearinghouse on any given day.

It is these rules which we are adhering to when we review your short positions relative to our settlement obligations with the clearinghouse each day. While the shares necessary to cover your short sale may have been available as of the date your trade took place and subsequently thereafter, there can be no assurance that those shares can be borrowed indefinitely. The inventory of available shares to borrow is dynamic and subject to change throughout a given day. When we believe that there is a reasonable chance that we will not be able to maintain your borrow position on a particular day, we will make every effort to provide you with a notice of those short positions which are likely to be bought in absent preemptive action on your part.

Overview of Regulation SHO

Regulation SHO, adopted by the SEC in January 2005, sets forth the regulatory framework governing short sales. Two key provisions, intended to address problems associated with persistent fails to deliver and potentially abusive naked short selling, involve locate and close-out requirements.

Under the locate requirement, a broker-dealer must have reasonable grounds to believe that the security can be borrowed so that it can be delivered on the delivery due date before effecting a short sale order.

The close-out requirement requires that the clearing broker take immediate action to close out a fail to deliver position in a threshold security that has persisted for 13 consecutive settlement days by purchasing securities of like kind and quantity. Until the position is closed out, the broker may not effect further short sales in that threshold security without borrowing or entering into a bona fide agreement to borrow the security (known as the "pre-borrowing" requirement)

IMPORTANT NOTE:

In October 2008, the SEC amended Regulation SHO with temporary Rule 204T (in place until July 31, 2009) which requires that any broker having a fail to deliver position at NSCC on the settlement date immediately borrow or purchase securities to close out the amount of the fail to deliver position by no later than the beginning of regular trading hours on the following settlement date (the “Close-Out Date”). This close-out requirement requires that the broker take affirmative action to purchase or borrow securities and not offset the fail to deliver position with shares it will receive on the Close-Out Date. Rule 204T applies to all securities not just threshold securities.

Glossary terms:

I have an open order to sell short stock that should have been executed, but it is still on my TWS and not being filled.

Overview:

When traders attempt to sell short a stock which IBKR does not currently have in inventory to loan them, IBKR will look for these shares “on the street”, which means from other brokerage firms. This search is conducted on a best-efforts only basis. While IBKR searches for the shares, the order status box on the TWS Order Management page should be dark green and will show a small icon of a pair of binoculars, which indicates we are searching. In the WebTrader, there are no status colors or icons. The order will simply not execute as IBKR searches for the shares on the street.