Attribution d'options avant échéance

Un vendeur d'options américaines peut se voir attribuer un exercice à tout moment jusqu'à l'échéance de l'option. Cela signifie que le vendeur de l'option peut recevoir une attribution à tout moment après qu'il ou elle a vendu l'option jusqu'à l'exercice de l'option ou jusqu'à ce que le vendeur du contrat d'options clôture sa position en le rachetant à la fermeture. Un exercice anticipé peut survenir lorsque le détenteur d'une option d'achat ou de vente invoque ses droits avant l'échéance. En tant que vendeur de l'option, vous n'avez pas le contrôle de l'attribution et il est impossible de savoir exactement que cela pourrait arriver. En général, le risque d'attribution devient de plus en plus grand à l'approche de l'échéance, cependant, l'attribution peut encore arriver à tout moment lors du trading d'options américaines.

Option de vente à découvert

Lors de la vente d'un option de vente, le vendeur a l'obligation d'acheter l'action ou l'actif sous-jacent à un prix donné (prix de levée) dans un créneau donné (date d'échéance). Si le prix d'exercice de l'option est inférieur au cours actuel de l'action, le détenteur de l'option ne gagne pas en valeur en vendant l'option de vente au vendeur car la valeur de marché est supérieure au prix de levée. À l'inverse, si le prix de levée de l'option est supérieur au cours de l'action actuel, le vendeur de l'option sera confronté au risque d'attribution.

Option d'achat à découvert

Vendre une option d'achat donne le droit au propriétaire de l'option d'achat de vendre ou d'« appeler » l'action au remboursement pour le vendeur dans un créneau donné. Si le prix de marché de l'action est inférieur au prix de levée de l'option, le détenteur de l'option de vente n'a pas d'avantage à appeler l'action au remboursement à un montant plus élevé que la valeur de marché. Si la valeur de marché de l'action est supérieure au prix d'exercice, le détenteur de l'option peut appeler l'action au remboursement à un prix inférieur à la valeur de marché. Les options d'achat à découvert sont confrontées au risque d'attribution lorsqu'ils sont dans le cours ou s'il y a un dividende à venir et que la valeur intrinsèque de l'option d'achat est inférieure au dividende.

Qu'adviendra-t-il de ces options ?

Si une option d'achat à découvert est attribuée, le détenteur se verra attribuer des actions à découvert. Par exemple, si les actions de l'entreprise ABC s'échangent à 55 $ et qu'une option d'achat à découvert au prix de levée de 50 $ est attribuée, l'option d'achat à découvert serait convertie en actions à découvert à 50 $. Le détenteur de compte pourrait ensuite décider de clôture la position à découvert en rachetant les actions au prix du marché de 55 $. La perte nette serait de 500 $ pour 100 actions, moins le crédit reçu lors de la vente de l'option d'achat.

Si une option de vente est attribuée, le détenteur se verrait attribuer des actions longues au prix d'exercice de l'option de vente. Par exemple, avec les actions de XYZ s'échangeant à 90 $, le vendeur de l'option de vente se voit attribuer des actions au prix de levée de 96 $. Le vendeur de l'option de vente est responsable de l'achat d'action au-dessus du prix du marché au prix de levée de 96 $. Supposons que le détenteur de compte clôture la position longue à 90 $, la perte nette serait de 600 $ pour 100 actions, moins le crédit reçu de la vente de l'option de vente.

Déficit de marge de l'attribution d'option

Si l'attribution a lieu avant l'échéance et que la position entraîne un déficit de marge, conformément à notre politique de marge, les comptes font l'objet d'une liquidation automatique pour ramnenr le compte dans les exigences de marge. Les liquidations ne se limitent pas uniquement aux actions résultant de la position d'option.

De plus, pour les comptes qui se sont vus attribuer la jambe à découvert d'un spread d'option, IBKR n'exercera PAS les longues positions détenues dans le compte. IBKR ne peut pas deviner les intentions du détenteur de la position longue, et l'exercice de la position longue avant l'échéance fera perdre la valeur temps de l'option, qui pourrait être réalisées par la vente de l'option.

Exposition post-échéance, opérations sur titre et événements ex-dividende

Interactive Brokers prend des mesures proactives pour atténuer le risque, par rapport à certains événements liés à des échéances ou opérations sur titres. Pour plus d'informations concernant notre politique d'échéance, veuillez consulter l'article « Liquidations liées à l'échéance et aux opérations sur titres ».

Les détenteurs de compte peuvent se référer au document Characteristics and Risks of Standardized Options qui est fourni par IBKR à chaque client admissible au trading d'options lors de l'ouverture du compte et qui explique clairement les risques de l'attribution. Ce document est également disponible sur le site de l'OCC.

Comment les cours de clôture des options sur titres des États-Unis sont-ils déterminés ?

Les cours qu'IB utilise pour marquer les options sur titres cotées aux État-Unis à la clôture de chaque jour (TWS et relevés) proviennent de l'Options Clearing Corporation (OCC). En tant que seule chambre de compensation pour ces produits d'options, l'OCC génère un cours de clôture pour chaque contrat d'option pour calculer la marge requise de ses membres pour lesquels elle compense les transactions (ex. : IB) et également pour fournir les tableaux de risque utilisés par les courtiers portant des comptes de portefeuille sur marge.

Il est important de noter que les cours générés par l'OCC sont modifiés et peuvent ne pas refléter le cours de clôture tel que distribué par les Bourses participantes. Ils sont tout d'abord modifiés car il n'y a pas de cotes groupées pour les options, la plupart desquelles sont cotées plusieurs fois et fongibles sur les sept Bourses (c'est-à-dire que vous pouvez avoir à choisir entre sept cotes chaque jour). En conséquence, l'OCC crée un cours unique à la clôture, qui est théoriquement uniforme sur toutes les Bourses et vérifié pour veiller à ce qu'il n'y ait pas de conditions d'arbitrage de levée ou de temps.

Pour créer des cours, l'OCC commencera par prendre le point médian du cours acheteur le plus élevé et du cours vendeur le plus bas parmi toutes les bourses, déterminant ainsi la volatilité implicite et lissant la courbe de la volatilité implicite (pour une catégorie, un type ou une échéance d'option donné(e)) grâce à un processus itératif qui, à son tour, ajuste les cours de l'option. Il existe également des règles mises en place pour limiter la volatilité de certaines options nettement dans ou hors du cours. Le cours modifié résultant est étendu jusqu'à 6 décimales. En raison des frais généraux d'exploitation pour le calcul des cours modifiés pour l'univers entier des séries d'option, ce processus n'est réalisé qu'une fois par jour à la clôture des marchés.

Pourquoi ne suis-je pas informé(e) de l'attribution de mes positions d'options sur titres US avant le jour suivant ?

Overview:

Le traitement des avis de levée pour les options américaines sur des jours autres que la date d'échéance n'est pas réalisé en temps réel, mais dans le cadre d'un traitement de nuit par lots, par l'Options Clearing Corporation (OCC). La séquence de traitement, qui par définition résulte en un décalage de notification d'au moins un jour pour le client, est la suivante :

- L'OCC permet généralement à ses membres compensateurs de soumettre électroniquement des avis de levée au nom des clients détenant une position longue pendant la journée, mais normalement pas après le début du traitement critique du soir (Jour E).

- Dans le cadre de la séquence de traitement de position du soir, l'OCC attribue au hasard les avis de levée qu'elle a reçu aux positions ouvertes de ses membres compensateurs. Cette information est ensuite rendue disponible par l'OCC à ses membres compensateurs tôt le matin du jour suivant (Jour E+1).

- Quand l'information est disponible, les sociétés de compensation telles qu'IBKR ont déjà terminé leur traitement de l'activité du jour pour pouvoir fournir des relevés, informations de marge et de règlement en temps voulu à leurs clients. L'OCC détenant les positions des clients de ses membres compensateurs de manière omnibus (elle ne connaît pas l'identité des clients, seule la société de compensation la connaît), le membre compensateur doit, à son tour, exécuter un processus au hasard pour attribuer ces avis de levée aux clients détenant une position à découvert dans cette série d'options précise.

- Quand IBKR reçoit un avis d'attribution de la part de l'OCC et réalise son processus d'attribution au hasard, les attributions seront publiées sur la Trader Workstation des comptes impactés et apparaîtra sur le relevé d'activité journalier à la clôture de ce jour (E+1).

De plus, en raison de cette séquence de traitement et le fait qu'une option longue peut avoir une valeur temps restant, IBKR ne peut pas fournir automatiquement un avis de levée à l'OCC pour tout spread d'option longue contre l'option à découvert assignée comme moyen de compenser l'obligation de livraison en découlant.

Les détenteurs de compte peuvent se référer au document Characteristics and Risks of Standardized Options qui est fourni par IBKR à chaque client admissible au trading d'options lors de l'ouverture du compte et qui explique clairement les risques de l'attribution. Ce document est également disponible sur le site de l'OCC.

Qu'advient-il des options sur actions des États-Unis si le sous-jacent devient le sujet d'un fusion complète en espèces ?

Dans le cas d'une option sur actions associée à une fusion dans laquelle le titre sous-jacent a été converti en espèces à 100 % après le 31 décembre 2007, l'OCC accélérera son échéance. La nouvelle date d'échéance pour ces options sera accélérée à l'échéance des actions standards la plus proche, sauf si la conversion de espèces a lieu après le mardi de la semaine d'échéance, au quel cas, la date d'échéance pour tous les contrats n'ayant pas leur date d'échéance cette semaine sera repoussée à l'échéance du mois suivant.

Veuillez noter que cette accélération n'impacte pas le seuil d'exercice automatique, grâce auquel les options ayant un prix d'exercice dans le cours d'au moins 0.01 $ seront exercées automatiquement par l'OCC. Elle n'impacte pas non plus la date de réglement en espèces attribuable à l'exercice, qui reste à T+2.

Veuillez également noter que cette accélération n'impacte pas les options converties en espèces le (ou avant le) 31 décembre 2007, qui resteront valides jusqu'à ce que leur date d'échéance d'origine soit atteinte.

Si on m'attribue une jambe à découvert d'un spread d'option, la jambe longue de l'option sera-t-elle exercée automatiquement pour compenser la position d'action résultant du transfert ?

La réponse dépend de si le transfert a eu lieu à l'échéance ou avant (option américaine). À l'échéance, de nombreuses chambres de compensation vont utiliser un processus d'exercice par exception conçu pour réduire le surcoût opérationnel lié à la mise à disposition d'instructions d'exercice par les membres de la chambre de compensation. Dans le cas d'options sur action US par exemple, l'OCC exercera automatiquement toute action ou option sur indice qui est dans le cours d'au moins 0.01 $ sauf si des instructions d'exercice contraires ont été fournies par le client au membre compensateur. Ainsi, si l'option longue a la même date d'échéance que l'option à découvert et qu'à l'échéance, elle est dans le cours d'au moins le montant de l'exercice établi par seuil d'exception, la chambre de compensation exercera automatiquement, compensant réellement l'obligation d'actions du transfert. Selon les prix d'exercice de l'option, ceci peut résulter en un débit ou un crédit net sur le compte.

Si le transfert a lieu avant la date d'échéance, ni IBKR ni la chambre de compensation n'exerceront une option longue détenue dans le compte, car aucune partie ne peut deviner les intentions du détenteur de l'option longue. Ainsi, l'exercice d'une option longue avant la date d'échéance résultera en une perte de valeur temps qui pourra être résolue par la vente de l'option.

Où puis-je trouver des informations supplémentaires concernant les options ?

L'Options Clearing Corporation (OCC), la chambre de compensation principale pour toutes les options sur actions négociées en Bourses aux États-Unis, maintient un centre d'appels pour répondre aux besoins en informations des investisseurs particuliers et courtiers en titres de détail. Ce centre peut répondre aux besoins et problèmes suivants, liés aux produits d'options compensés par l'OCC :

- Informations de l'Options Industry Council concernant des séminaires, vidéos et documents pédagogiques ;

- Questions de base concernant les options comme des définitions et des informations sur les produits ;

- Réponses aux questions stratégiques et opérationnelles, notamment les positions de transactions et stratégies.

Vous pouvez joindre les centre d'appels en composant 1-800-OPTIONS. Les heures de service sont du lundi au jeudi de 8 h 00 à 17 h 00 (CST) et le vendredi de 8 h 00 à 17 h 00 (CST). Les heures pour le vendredi d'échéance du mois seront prolongées jusqu'à 17 h 00 (CST).

Bonus Certificates Tutorial

Introduction

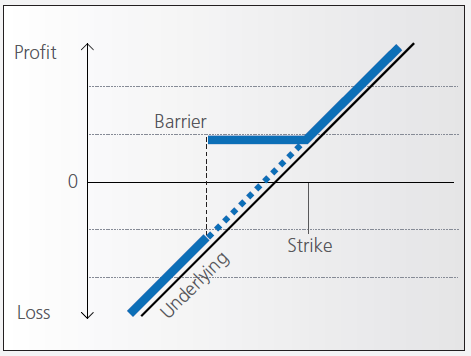

Bonus certificates are designed to provide a predictable return in sideways markets, and market returns in rising markets.

At the time they’re issued, bonus certificates normally have a term to maturity of two to four years. You will receive a specified cash pay-out (“bonus level” or “Strike”) if at maturity the price of the underlying is below or at the strike, as long as the underlying instrument has not touched or fallen below an established price level (“safety threshold” or “barrier”) during the term of the certificate.

Unless the certificate has a cap, you continue to participate in the price gains if the underlying instrument rises above the bonus level. In this case you either receive the corresponding number of shares or a cash settlement reflecting the value of the underlying instrument on the maturity date.

However, if the barrier is breached, you will no longer be entitled to the bonus payment. The value of the certificate then corresponds to the value of the underlying (times the ratio). In other words, once the barrier has been touched the certificate effectively converts to an index certificate. You will receive either the corresponding number of shares or a cash settlement reflecting the value of the underlying instrument on the maturity date.

Although there is no structured leverage, the presence of the barrier creates effective leverage. When the price of the underlying instrument approaches the barrier the probability of a breach increases, affecting the price of the certificate disproportionately.

Pay-out Profile

Example

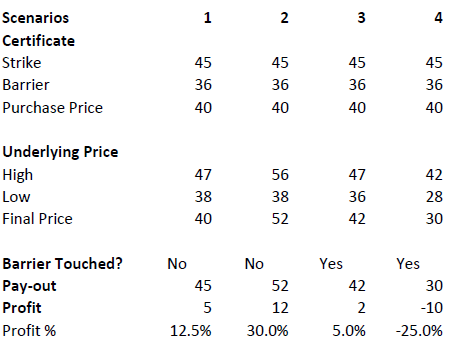

Assume a bonus certificate on ABC share. The certificate has a strike of EUR 45.00 and a barrier set at EUR 36.00. The table below shows scenarios depending on the trading range of the underlying, the final price of the underlying and whether the barrier has been touched or not.

Warrant Tutorial

Introduction

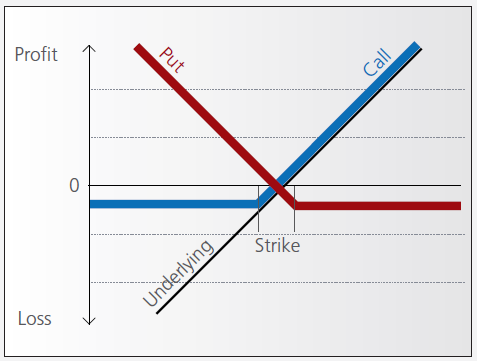

A warrant confers the right to buy (call-warrant) or sell (put-warrant) a specific quantity of a specific underlying instrument at a specific price over a specific period of time.

Pay-out Profile

With some warrants, the option right can only be exercised on the expiration date. These are referred to as “European-style” warrants. With “American-style” warrants, the option right can be exercised at any time prior to expiration. The vast majority of listed warrants are cash-exercised, meaning that you cannot exercise the warrant to obtain the underlying physical share. The exception to this rule is Switzerland, where physically settled warrants are widely available.

IBKR does allow for US and Canadian warrant exercise. Customers wishing to do so should submit a Customer Service ticket stating the name/symbol of the warrant, the quantity of shares and the intended action (i.e. exercise). The broker will pass through all associated exercise costs to the customer upon completion of the request. US or Canadian warrants are not eligible for auto-exercise at expiration. Warrants remaining in an account at expiration will be removed as worthless.

Factors that influence pricing

Not only do changes in the price of the underlying instrument influence the value of a warrant, a number of other factors are also involved. Of particular importance to investors in this regard are changes in volatility, i.e. the degree to which the price of the underlying instrument fluctuates. In addition, changes in interest rates and the anticipated dividend payments on the underlying instrument also play a role.

However, changes in implied volatility - as well as interest rates and dividends - only affect the time value of a warrant. The primary driver - intrinsic value - is solely determined by the difference between the price of the underlying instrument and the specified exercise price.

Historical and implied volatility

In addressing this topic, a differentiation has to be made between historical and implied volatility. Implied volatility reflects the volatility market participants expect to see in the financial instrument in the days and months ahead. If implied volatility for the underlying instrument increases, so does the price of the warrant.

This is because the probability of profiting from a warrant during a particular time-frame increases if the price of the underlying instrument is highly volatile. The warrant is therefore more valuable.

Conversely, if implied volatility decreases, that leads to a decline in the value of warrants and hence occasionally to nasty surprises for warrant investors who aren’t familiar with the concept and influence of volatility.

Interest rates and dividends

Issuers hedge themselves against price changes in the warrant through purchases and sales of the underlying instrument. Due to the leverage afforded by warrants, the issuer needs considerably more capital to hedge its exposure than you require to buy the warrants. The issuer’s interest expense associated with that capital is included in the price of the warrant. The amount of embedded interest reduces over time and at expiration is zero.

In the case of puts, the situation is exactly the opposite. Here, the issuer sells the underlying instrument

short to establish the necessary hedge, and in so doing receives capital that can earn interest. Thus interest reduces the price of the warrant by an amount that decreases over time.

As the issuer owns shares as a part of its hedging operations, it is entitled to receive the related dividend

payments. That additional income reduces the price of call warrants and increases the price for puts. But if the dividend expectations change, that will have an influence on the price of the warrants. Unanticipated special dividends on the underlying instrument can lead to a price decline in the related warrants.

Key valuation factors

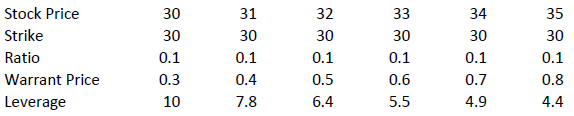

Let’s assume the following warrant:

Warrant Type: Call

Term to expiration: 2 years

Underlying : ABC Share

Share price: EUR 30.00

Strike: EUR 30.00

Exercise ratio: 0.1

Warrant’s price: EUR 0.30

Intrinsic value

Intrinsic value represents the amount you could receive if you exercised the warrant immediately and then bought (in the case of a call) or sold (put) the underlying instrument in the open market.

It’s very easy to calculate the intrinsic value of a warrant. In our example the intrinsic value is EUR 00.00

and is calculated as follows:

(price of underlying instrument – strike price) x exercise ratio

= (EUR 30.00 – EUR 30.00) x 0.1

= EUR 00.00

If the price of the ABC share increases by EUR 1, the intrinsic value becomes

= (EUR 31.00 – EUR 30.00) x 0.1

= EUR 00.10

The intrinsic value of a put warrant is calculated with this formula:

(strike price – price of underlying instrument) x exercise ratio

It’s important to note that the intrinsic value of a warrant can never be negative. By way of explanation:

if the price of the underlying instrument is at or below the exercise price, the intrinsic value of a call equals zero. In this instance, the price of the warrant consists only of “time value”. On the flipside, the intrinsic value of a put is equal to zero if the price of the underlying instrument is at or above the exercise price.

Time value

Once you’ve calculated the intrinsic value of a warrant, it’s also easy to figure out what the time value of that warrant is. You simply deduct the intrinsic value from the current market price of the warrant. In our example, the time value is equal to EUR 1.30 as you can see from the following calculation:

(warrant price – intrinsic value)

= (EUR 0.30 EUR – EUR 0.00)

= EUR 0.30

Time value gradually erodes during the term of a warrant and ultimately ends up at zero upon expiration. At that point, warrants with no intrinsic value expire worthless. Otherwise you can expect to receive payment of the intrinsic value. Take note, though: a warrant’s loss of time value accelerates during the final months of its term.

Premium

The premium indicates how much more expensive a purchase/sale of the underlying instrument would be via the purchase of a warrant and the immediate exercise of the option right as opposed to simply buying/selling the underlying instrument in the open market.

Hence the premium is a measure of how expensive a warrant actually is. It follows that, when given a choice between warrants with similar features, you should always buy the one with the lowest premium. By calculating the premium as an annualized percentage, warrants with different terms to expiry can be compared with each other.

The percentage premium for the call warrant in our example can be calculated as follows:

(strike price + warrant price / exercise ratio – share price) / share price * 100

= (EUR 30.00 + EUR 0.30 / 0.1 – EUR 30.00) / EUR 30.00 x 100

= 10 percent

Leverage

The amount of leverage is the price of the share * ratio divided by the price of the warrant. In our example 30.00*0.1/0.3 = 10. So when the price of ABC increases by 1% the value of the warrant increases by 10%.

The amount of leverage is not constant however; it varies as intrinsic and time value changes, and is particularly sensitive to changes in intrinsic value. As a rule of thumb, the higher the intrinsic value of the warrant, the lower the leverage. For example (assuming constant time value):

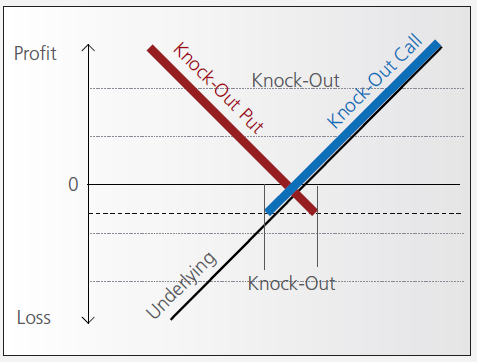

Knock-out (Turbo) Tutorial

Introduction

Knock-out warrants (turbos), like vanilla warrants, derive their value from the difference between the price of the underlying and the strike. They differ significantly however from vanilla warrants in many important respects:

- They can expire (knock-out) prematurely if the price of the underlying instrument touches or falls below (in the case of knock-out calls) or exceeds (in the case of knockout puts) a predetermined barrier-level. It expires worthless if the barrier equals the strike, or it may have a residual stop-loss value if the barrier is set higher than the strike (in the case of a call).

- Changes in implied volatility have little or no impact on knock-out products, therefore their pricing is easier for investors to comprehend than that of warrants.

- They have little or no time value (because of the presence of the knock-out barrier), and therefore have a higher degree of leverage than a warrant with the same strike. This is because the absence of time value makes the instrument “cheaper”.

Pay-out Profile

Leverage

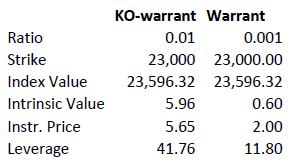

As discussed above, knock-out warrants exhibit high degrees of leverage, particularly as the price of the underlying nears the strike/barrier. Consider the following example of a long turbo on the Dow Jones Index, compared to a vanilla warrant:

Intrinsic value = (index value – strike) x ratio

Leverage = Index Value x Ratio / Instrument Price

A vanilla warrant retains significant time value even as the underlying price approaches the strike, sharply reducing its leverage compared to a knock-out warrant.

Product types

As discussed above, the barrier may either equal the strike, or be set above (calls) or below (puts). In the latter cases a small residual value remains after knock-out, corresponding to the difference between the barrier (the stop-loss level) and the strike.

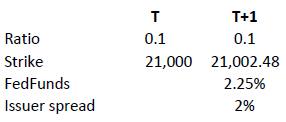

Moreover, knock-out products may either have an expiration date or may be open-ended. This makes a difference in the way interest is accounted for. If the contract has an expiration date interest is included in the premium, the amount of which reduces over time and is zero on expiration. This is analogous to a standard vanilla warrant.

in relation to an expiration date. The price of the contract therefore corresponds exactly to its intrinsic value. Interest however must be accounted for. This is done by a daily adjustment of the barrier and strike. The following example shows the daily adjustment for a long open-end turbo on the Dow Jones Index:

The adjustment = Strike T x (1+ FedFunds/360 + Issuer Spread/360).

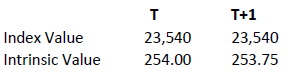

The intrinsic value of the instrument is correspondingly reduced as follows, assuming no change in the value of the DJ Index):

Intrinsic value = (index value – strike) x ratio