MiFIR取引報告義務に関する概要

背景

2018年1月3日より、新規金融商品市場指令2014/65/EC(「MiFID II」)および規制(EU)No 600/2014(「MiFIR」)が実施され、これに伴い2007年に金融商品市場指令(「MiFID I」)として作成された取引報告(「MiFIR取引報告」の骨組みに大幅な変更が導入されますを

Interactive Brokers (U.K.) Limited(「IBUK」)では、新規規制の下に直接報告義務の発生するIBUKおよびインタラクティブ・ブローカーズグループ(「IBグループ」)のお客様が新しいMiFIR基準に従って報告ができるよう、新しい取引報告システムの実施を行います。

これによる影響のあるお客様には、2018年1月3日に新規報告義務が実施される際に継続して口座から取引ができるよう、弊社に追加情報をご提供いただく必要があります。必要となる追加情報の収集にあたっては、インタラクティブ・ブローカーズよりお客様に電子リクエストをお送り致します。

該当されるお客様には2017年11月30日までに情報をご提供いただきますようお願い致します。

MiFIR取引報告義務の範囲

MiFIR取引報告はIBUKなどの欧州経済地域(「EEA」)における投資会社や、IBUKまたはその他のインタラクティブ・ブローカーズ・グループ関連会社を利用して注文の約定を行うEEA投資会社に適用されます。IBUKのお客様やIBのプラットフォームを利用される投資会社のお客様には、取引報告の正確な記録を目的として、追加情報をご提供いただく必要が発生する可能性があります。

EEA投資会社はMiFIRに含まれる金融商品の約定に関し、完全かつ正確な詳細を監督当局に翌日の終了時までに報告することを義務付けられています。

MiFIRは報告義務のある金融商品の範囲を拡大し、これによりEEA規制のある取引所、多角的取引システム(「MTF」)および取引施設(「OTF」)にて取引される商品が含められるようになります。EEA取引所で約定される取引に追加して、MiFIRは店頭取引(「OTC」)、およびNYSEで取引されるLSE上場株式などのEEA以外の取引所で約定されるEEA上場の金融商品の取引も含めるようになります。(MiFIRにカバーされる投資商品をご確認ください)。

IBを利用されるEEA投資会社のお客様への取引報告ソリューション: 強化および委任された取引報告

MiFIR取引報告義務の対象となるEEA投資会社であることを承認された弊社のお客様には、IBUKに報告義務を委任するという選択肢をご提供致します。

EEA投資会社の約定した取引の幾つかは、「強化された報告」義務の下、IBUKにより報告が行われます。こういった取引に関し、IBUKでは投資会社の詳細を自信のレポートに追加することにより、投資会社の報告義務を達成します。その他の取引は別に弊社レポートに追加され、投資会社の代理として委任される場合のみのベースで報告されます。両方のタイプのレポートに関連し、お客様にはIBUKとの同意書一通にだけご署名いただく必要があります。

強化および委任された取引報告に関する詳細は、こちらをクリックしてください。

報告義務のある情報

MiFID Iの下では23あった報告項目はMiFIR変更後、65項目になりました。今回、新しく追加された必要情報には以下が含まれます:

- 各取引の買い手と売り手に関する詳細。この規制により法人には取引主体識別(「LEI」)、また自然人には国民総背番号(国籍を所有する国に基き)の提供が必要となります。

- 第三者機関が裁量により行使する場合、買い手と売り手に関する決定権を持つ者の詳細:

- 個人またはジョイント口座の口座保有者以外の人物、または第三者である法人。

- 組織口座の場合には許可されているトレーダー以外の第三者(顧客のサブ口座用に取引をするファイナンシャル・アドバイザーなど)。

この情報は口座保有者が自身で取引する場合や、許可を持つトレーダーが自身の組織のために取引する場合には必要ではありません。

- 報告をする企業において取引決定を下すまたは取引の執行をする責任を持つ人物およびアルゴリズムの特定。弊社のレポートサービスを利用されるEEA投資会社はこの情報の提供が必要となります。詳細はこちらをクリックしてご確認ください。

- コモディティ・デリバティブ取引の場合には、そういった取引がMiFID IIの57条に則って客観的に測定可能な状況でリスクを減少するかどうかの表示。これは口座保有者が非金融法人の場合のみ機関用口座に適用されます。

新しい情報はお客様がEEA投資会社や投資会社ではない組織/個人であるか、また取引される金融商品がIBUKやその他のインタラクティブ・ブローカーズ・グループ関連会社によって持ち越されるかなど、様々な状況で弊社のお客様に影響します。

MiFIR取引報告義務の対象とならない弊社お客様への関連事項

IBUKでもまた約定される各取引に対し、これに直接関連するお客様を特定して報告することを義務化されています。報告には規制により義務とされる、新規の顧客識別子が含まれます。

このためIBUKでは以下の場合に、顧客識別子の入手および報告を行います:

- IBUKの保有する金融商品を取引するための口座を保有される、IBUK直接のお客様 ;

- インタラクティブ・ブローカーズの報告サービスをご利用されるEEA投資会社のお客様;

- インタラクティブ・ブローカーズのプラットフォームおよび報告サービスをご利用される投資会社のサブ口座となるお客様。

MiFIRによる直接の対象とならない口座保有者から必要となる情報に関する詳細はKB2976をご覧ください。

留意点: MiFIRの一般的な定義や 表現に関してましては、KB2980をご覧ください。

この情報はインタラクティブ・ブローカーズでクリアリングされるお客様のみを対象とするものであり、約定のみの口座には適用されません。

留意点: 上記の情報は包括的なガイダンスとされるものではなく、また規制に関する決定的な解釈ではなく、MiFIR取引報告義務のサマリーです。

PRIIPs Regulation

The Packaged Retail and Insurance-based Investment Products Regulation - EU No 1286/2014 (“PRIIPs Regulation” or “PRIIPs”) became applicable on 1 January 2018.

A PRIIP is defined as any investment where the amount repayable to the investor is subject to fluctuations because of exposure to reference values. PRIIPs include ETFs, options, futures, CFDs, structured products, etc.

The Regulation requires product manufacturers to create Key Information Documents (KIDs) and persons advising or selling PRIIPs to provide retail investors based in the European Economic Area (EEA) with KIDs to enable those investors to better understand and compare products. The UK Financial Conduct Authority (FCA) has equivalent requirements for UK residents.

As a broker, IBKR is required to block trading in a PRIIP if a KID is not available.

The objectives of the PRIIPs Regulation.

Since the financial crisis of 2008, one of the main objectives of the European Commission has been to increase consumer protection and rebuild confidence in financial markets.

The Regulation specifies that the Key Information Document (KID) must be prepared in a standardised format.

By defining a standard format and content for the KID, the Regulation aims to:

- Ensure that the information provided is complete and comparable between similar products in order to help investors make informed investment decisions.

- Improve transparency and increase confidence in the retail investment market.

What is a KID?

The KID is a 3-page document that contains important details of the product including general description, cost, risk reward profile and possible performance scenarios.

Who is the regulation applicable to?

The Regulation applies to both PRIIPs manufacturers and distributors. The responsibility to create and maintain the document falls to the product manufacturer. However, any distributor or financial intermediary that sells or provides advice about PRIIPs to a retail investor, or receives a buy order for a PRIIP from a retail investor, must provide the investor with a KID. This also applies to execution-only, online environments.

Who should receive a KID?

Retail investors domiciled in the EEA and the UK should receive a KID prior to investing in a PRIIP. If no KID is available from the manufacturer, the PRIIP will be restricted from trading for EEA and UK retail clients.

Generally KIDs must be provided in an official language of the country in which a client is resident.

However, clients of IBKR have agreed to receive communications in English, and therefore if a KID is available in English all EEA and UK clients can trade the product regardless of their country of residence.

If a KID is not available in English, but one is available in another language, German for example, the PRIIP can only be traded by retail clients who are citizens of, or resident in countries where that language is an official language, in this example Germany, Austria, Belgium, Luxembourg or Liechtenstein.

Special Case – US ETFs

U.S. clients are not impacted by PRIIPs, so the issuers of U.S. listed ETFs do not as a rule create KIDs. This means that EEA and UK Retail clients may not purchase the product. Clients nevertheless have several options:

- Many US ETF issuers have equivalent ETFs issued by their European entities. European-issued ETFs have KIDs and are therefore freely tradable.

- Clients can trade most large US ETFs as CFDs. The CFDs are issued by IBKRs European entities and as such meet all KID requirements.

- Clients may be eligible for re-classification as a professional client, for whom KIDs are not required.

CLIENT CATEGORISATION

We categorize all individual clients as “Retail” by default as this affords clients the broadest level of protection afforded by MiFID. Client who are categorised as “Professional” do not receive the same level of protection as “Retail” but are not subject to the KIDs requirement. As defined under MiFID II rules, “Professional” clients include regulated entities, large clients and individuals who have asked to be re-categorised as “elective professional clients” and meet the MiFID II requirements based on their knowledge, experience and financial capability.

We provide an online step-by-step process that allows “Retail” to request that their categorisation be changed to “Professional". The qualifications for re-categorisation along with the steps for requesting that one’s categorisation be considered are outlined here or, to directly apply for a change in categorisation, the questionnaire is available in the Client Portal/Account Management.

Implications for Interactive Brokers:

In order to meet the PRIIPs Regulation, where required, IB UK will provide KIDs electronically by means of a website (“PRIIPs KID Landing Page”).

Where can I find the PRIIPs KID Landing Page?

The KIDs can be accessed from our designated PRIIPs KID Landing Page. There are three different ways you can find the KIDs. They are available through the IBKR Trader Workstation (“TWS”), the IBKR website and Client Portal.

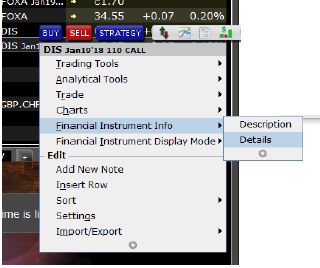

1. Find KIDs through TWS:

- Log into TWS

- Right click on the symbol of the product for which you want the KID.

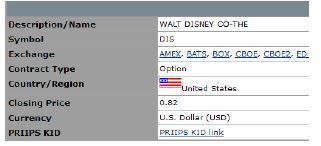

- Under Financial Instrument Info select Details.

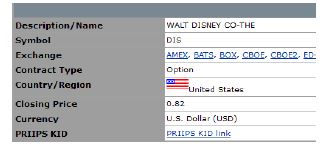

- From the Contract Details page, you can select the PRIIPs KID link. This will take you to our PRIIPs KID Landing Page in Client Portal.

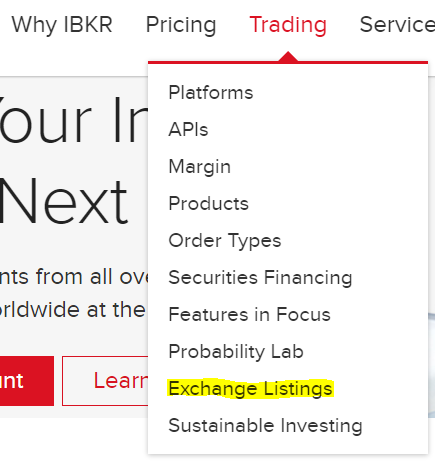

2. Find KIDs through the IBKR website:

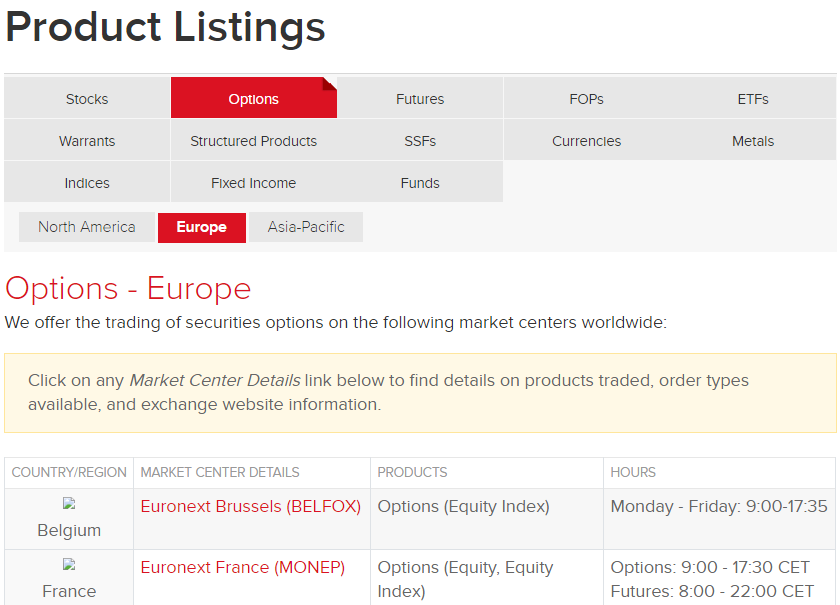

- Open the Trading tab and select Exchange Listings.

- From there, select Product Listings. Select the derivative type, region and exchange of the product for which you would like to find the contract information.

- Select the product you would like to see the KID of, which will take you to the Contract Details page.

- From the Contract Details page, as above, you can select the PRIIPs KID link, which will take you to our PRIIPs KID Landing Page in Client Portal.

3. Find KIDs through Client Portal:

- Log into Client Portal.

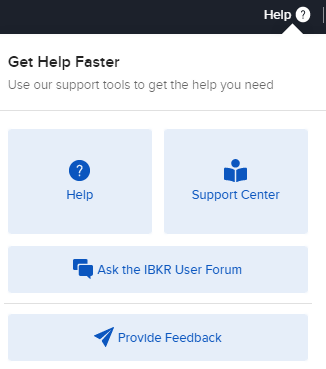

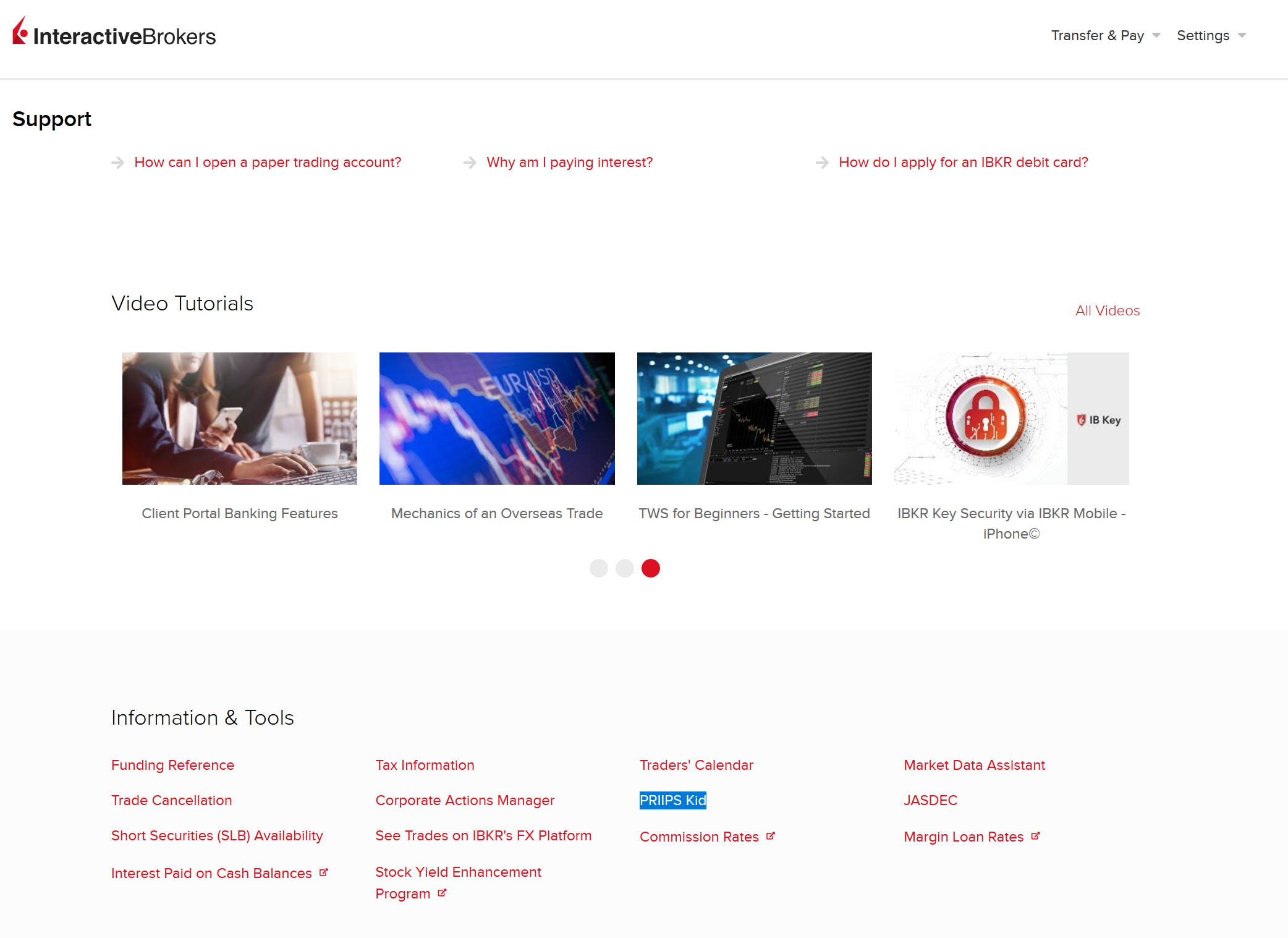

- Click the Help (?) icon followed by Support Center.

- In the Information & Tools section, select PRIIPs Kid, which will take you to our PRIIPs KID Landing Page.

Can I potentially get exposure to a US ETF/other PRIIPs restricted product through a CFD?

An investor could potentially get exposure to a U.S. ETF or other PRIIPs restricted product when trading a CFD (Contract for Difference) as some CFDs are designed to track the performance of underlying assets, including ETFs and other PRIIPs products.

If an investor trades a CFD that is designed to track the performance of a U.S. ETF or other PRIIPs product, the investor may be indirectly investing in that underlying asset. This is because the CFD's value is based on the value of the underlying asset, and any gains or losses in the value of the underlying asset will be reflected in the value of the CFD.

MiFIR Definitions & Terms

European Economic Area (EEA) - As of October 2017, the EEA consists of the following countries: Austria, Belgium, Bulgaria, Croatia, Republic of Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden and the United Kingdom.

Investment Firms - Article 4 (1) (1) of MiFID II defines investment firm as any legal person whose regular occupation or business is the provision of one or more investment services to third parties and/or the performance of one or more investment activities on a professional basis. The investment services and activities covered by the framework are listed in Section A of Annex I of MiFID II.

Transactions Executed - For the purposes of MiFIR Transaction Reporting, a transaction is the conclusion of an acquisition or disposal of one of the financial instruments covered by MiFIR. A transaction is considered to be executed when it resulted from one of the following activities performed by an Investment Firm:

- Reception or transmission of orders in relation to one or more financial instruments (exceptions apply under Article 4 of Commission Delegated Regulation (EU) 2017/590);

- Execution of orders on behalf of clients;

- Dealing on own account;

- Making an investment decision in accordance with a discretionary mandate given by a client;

- Transfer of financial instruments to or from accounts.

[Ref: Articles 2 and 3 of Commission Delegated Regulation (EU) 2017/590]

IB Broker - Accounts that trade financial instruments which are received and/or transmitted by one of the following Interactive Brokers Group entities ("IB Brokers"):

- Interactive Brokers (U.K.) Limited

- Interactive Brokers Central Europe Zrt.

- Interactive Brokers Ireland Limited

Financial Instruments Covered by MiFIR - Article 26 (2) of Regulation (EU) No 600/2014 (MiFIR) lays out the transaction reporting obligation with regard to transactions in financial instruments listed below, irrespective of whether or not such transactions are carried out on the trading venue:

- Financial instruments which are admitted to trading or traded on a trading venue or for which a request for admission to trading has been made;

- Financial instruments where the underlying is a financial instrument traded on a trading venue; and

- Financial instruments where the underlying is an index or a basket composed of financial instruments traded on a trading venue.

The financial instruments covered by this requirement are legally enumerated in Section C of MiFID II:

(1) Transferable securities;

(2) Money-market instruments;

(3) Units in collective investment undertakings;

(4) Options, futures, swaps, forward rate agreements and any other derivative contracts relating to securities, currencies, interest rates or yields, emission allowances or other derivatives instruments, financial indices or financial measures which may be settled physically or in cash;

(5) Options, futures, swaps, forwards and any other derivative contracts relating to commodities that must be settled in cash or may be settled in cash at the option of one of the parties other than by reason of default or other termination event;

(6) Options, futures, swaps, and any other derivative contract relating to commodities that can be physically settled provided that they are traded on a regulated market, a MTF, or an OTF, except for wholesale energy products traded on an OTF that must be physically settled;

(7) Options, futures, swaps, forwards and any other derivative contracts relating to commodities, that can be physically settled not otherwise mentioned in point 6 of this Section and not being for commercial purposes, which have the characteristics of other derivative financial instruments;

(8) Derivative instruments for the transfer of credit risk;

(9) Financial contracts for differences;

(10) Options, futures, swaps, forward rate agreements and any other derivative contracts relating to climatic variables, freight rates or inflation rates or other official economic statistics that must be settled in cash or may be settled in cash at the option of one of the parties other than by reason of default or other termination event, as well as any other derivative contracts relating to assets, rights, obligations, indices and measures not otherwise mentioned in this Section, which have the characteristics of other derivative financial instruments, having regard to whether, inter alia, they are traded on a regulated market, OTF, or an MTF;

(11) Emission allowances consisting of any units recognised for compliance with the requirements of Directive 2003/87/EC (Emissions Trading Scheme).

National Identifiers - Under MiFIR, natural persons must be reported by using specific national identifiers required under a priority order that depends and varies on the Country of citizenship that is identified as relevant under MiFIR. The identifier can be a passport, a national ID card, a tax or personal code or a concatenation of full name and date of birth (“CONCAT”). The IB Broker will only request clients to provide national identifiers that are not already available.

Legal Entity Identifiers (“LEI”) = 20-character unique identifier based on the ISO 17442 for the global identification of legal entities that engage in financial transactions.

Commodity Derivatives Transactions that reduce risk in an objectively measurable way - When reporting transactions in commodity derivatives, the IB Broker will have to specify whether the transaction reduces risk in an objectively measurable way in accordance with Article 57 of Directive 2014/65/EU (“Art 57”). The IB Broker will allow such transactions only from accounts held by entities that are non-financial entities using the account for trades in commodity derivatives that are intended to objectively reduce risk directly relating to their commercial activity in accordance with Art 57. (e.g. company that produces wheat that trades in such derivatives to hedge its commercial activity).

Account holders that make such a declaration in the Trading Permission section of their Account Management, agree that all the transactions executed in commodity derivatives for that account will be executed for reducing the risk under Art 57, and the IB Broker will report the relevant transactions accordingly.

Individual or algorithm responsible at the reporting firm for making the investment decision - Under MiFIR, Investment Firms are required to include in their transaction reports the identification of the individual or algorithm that was primarily responsible for making the investment decision within the firm to acquire or dispose of a financial instrument. Only one individual or algorithm can be identified as responsible with regard to a transaction, and Investment Firms must identify such individual or algorithm as specified in Article 8 of commission delegated regulation (EU) 2017/590.

In accordance with these requirements, your IB Broker has implemented a new section in Account Management and new features in the IB Trader Workstation to allow Investment Firms that report their transactions through an IB Broker to identify individuals and algorithms in compliance with the new obligations.

Individual responsible at the reporting firm for the execution of a transaction - Art 9 of Commission Delegated Regulation (EU) 2017/590 requires Investment Firms to identify individuals or algorithms responsible for determining which trading venue to access […], which firms to transmit orders to or any other condition related to the execution of an order. While this requirement applies only to IB Brokers for the majority of the transactions reports (because the IB Broker is usually the entity that executes the transaction), when an order is submitted by an Investment Firm that transaction reports through an IB Broker via the Delegated Transaction Reporting, the specific user that has submitted the order will be reported as responsible for executing the transaction.

Article 4 of commission delegated regulation (EU) 2017/590 - Transmission of an order

1. An investment firm transmitting an order pursuant to Article 26(4) of Regulation (EU) No 600/2014 (transmitting firm) shall be deemed to have transmitted that order only if the following conditions are met:

(a) the order was received from its client or results from its decision to acquire or dispose of a specific financial instrument in accordance with a discretionary mandate provided to it by one or more clients;

(b) the transmitting firm has transmitted the order details referred to in paragraph 2 to another investment firm (receiving firm);

(c) the receiving firm is subject to Article 26(1) of Regulation (EU) No 600/2014 and agrees either to report the transaction resulting from the order concerned or to transmit the order details in accordance with this Article to another investment firm.

For the purposes of point (c) of the first subparagraph the agreement shall specify the time limit for the provision of the order details by the transmitting firm to the receiving firm and provide that the receiving firm shall verify whether the order details received contain obvious errors or omissions before submitting a transaction report or transmitting the order in accordance with this Article.

2. The following order details shall be transmitted in accordance with paragraph 1, insofar as pertinent to a given order:

(a) the identification code of the financial instrument;

(b) whether the order is for the acquisition or disposal of the financial instrument;

(c) the price and quantity indicated in the order;

(d) the designation and details of the client of the transmitting firm for the purposes of the order;

(e) the designation and details of the decision maker for the client where the investment decision is made under a power of representation;

(f) a designation to identify a short sale;

(g) a designation to identify a person or algorithm responsible for the investment decision within the transmitting firm;

(h) country of the branch of the investment firm supervising the person responsible for the investment decision and country of the investment firm's branch that received the order from the client or made an investment decision for a client in accordance with a discretionary mandate given to it by the client;

(i) for an order in commodity derivatives, an indication whether the transaction is to reduce risk in an objectively measurable way in accordance with Article 57 of Directive 2014/65/EU;

(j) the code identifying the transmitting firm.

For the purposes of point (d) of the first subparagraph, where the client is a natural person, the client shall be designated in accordance with Article 6. For the purposes of point (j) of the first subparagraph, where the order transmitted was received from a prior firm that did not transmit the order in accordance with the conditions set out in this Article, the code shall be the code identifying the transmitting firm. Where the order transmitted was received from a prior transmitting firm in accordance with the conditions set out in this Article, the code provided pursuant to point (j) referred to in the first subparagraph shall be the code identifying the prior transmitting firm.

3. Where there is more than one transmitting firm in relation to a given order, the order details referred to in points (d) to (i) of the first subparagraph of paragraph 2 shall be transmitted in respect of the client of the first transmitting firm.

4. Where the order is aggregated for several clients, information referred to in paragraph 2 shall be transmitted for each client.

Also see:

Overview of MIFIR Transaction Reporting

MiFIR Enriched and Delegated Transaction Reporting for EEA Investment Firms

MiFIR Information Required from Account Holders that do not have Reporting Obligations

MiFIR Information Required from Account Holders that do not have Reporting Obligations

The MiFIR Transaction Reporting regime requires Investment Firms, like your IB Broker, to include specific client identifiers in their transaction reports.

Accounts that trade in financial instruments which are received and/or transmitted by one of the following Interactive Brokers Group entities (“IB Brokers”) will need to be identified in the IB Broker’s reports by using specific identifiers that may or may not be already available to it.

- Interactive Brokers (U.K.) Limited

- Interactive Brokers Central Europe Zrt.

- Interactive Brokers Ireland Limited

Similarly, Investment Firms that use the IB platform for their clients’ orders and have elected to transaction report through their IB Broker will have to use the same identifiers for their client orders. If you are the client of such a firm, your IB Broker may need additional information from you to complete the transaction reports.

Information Required

When additional information is necessary for this purpose, clients will be asked to provide it via the completion of an electronic form available in the Account Management.

The information requested for these accounts is:

- All countries of citizenship for natural persons that are account holders and authorised traders;

- A specific National Identifier for natural persons that are account holders and authorised traders;

- The Legal Entity Identifier for legal entities. Clients that do not have an LEI will be able to apply for one through their IB Broker.

- For organisation accounts, an indication as to whether the Legal Entity is a non-financial entity using the account for trades in Commodity Derivatives Transactions to reduce risk in an objectively measurable way in accordance with Article 57 of MiFID II.

Note: For a listing of common MiFIR definitions and terms, see KB2980

THIS INFORMATION IS GUIDANCE FOR INTERACTIVE BROKERS CLEARED CLIENTS ONLY. THIS GUIDANCE DOES NOT APPLY TO EXECUTION ONLY ACCOUNTS.

NOTE: THE INFORMATION ABOVE IS NOT INTENDED TO BE A COMPREHENSIVE OR EXHAUSTIVE GUIDANCE AND IT IS NOT A DEFINITIVE INTERPRETATION OF THE REGULATION, BUT A SUMMARY OF MiFIR TRANSACTION REPORTING OBLIGATIONS.

MiFIR Enriched and Delegated Transaction Reporting for Investment Firms

Who is Subject to the MiFIR Transaction Reporting Requirements?

All EEA and UK investment firms (collectively, "Investment Firms") are subject to the reporting requirements and will have to report all transactions executed in financial instruments covered by MiFIR within one working day from their execution.

The below entities (“IB Brokers”), will offer assistance to IB clients that are Investment Firms in complying with the new requirements:

- Interactive Brokers (U.K.) Limited

- Interactive Brokers Central Europe Zrt.

- Interactive Brokers Ireland Limited

- Interactive Brokers Luxembourg SARL

With the exception of Omnibus Introducing Brokers, where applicable, that utilise the IB platform (in which all their underlying client positions are held in one or more omnibus accounts), all IB clients that are EEA Investment Firms will be able to elect to have their IB Broker report on their behalf. The IB Broker will report for IB clients based on two distinct reporting mechanisms implemented in accordance with the Regulation: Enriched Transaction Reporting and Delegated Transaction Reporting.

ENRICHED TRANSACTION REPORTING

In compliance with Article 4 of Commission Delegated Regulation (EU) 2017/590, if an IB Broker includes details of orders submitted by clients that are Investment Firms (“the transmitting firm”) in its own transaction reports, the transmitting firm is exempt from reporting these transactions.

Enriched Transaction Reporting will only apply to transactions in financial instruments carried by an IB Broker submitted for execution by an Investment Firm for the benefit of the Investment Firm’s clients (for example, a Financial Advisor, Fund Manager or Introducing Broker Account submitting orders for its clients' subaccounts).

DELEGATED TRANSACTION REPORTING

Delegated Transaction Reporting services are provided by an IB Broker to Investment Firms for all other transactions submitted by the Investment Firm.

This includes transactions entered by the Investment Firm for its own proprietary account, transactions submitted on the basis of discretionary mandates given by their clients and transactions in Financial Instruments for which an IB Broker is not the carrying broker (i.e., any transaction in a financial instrument where another IB affiliate is the carrying broker). Delegated transaction reporting does not apply where the trades are submitted directly by clients of the Investment Firm.

These reports will be submitted to the National Competent Authority (“NCA”) of the Country of legal residence recorded in the Legal Entity Identifier of the account for which the Delegated Transaction Reporting was enabled (e.g., if the Investment Firm’s legal residence is Netherlands, transactions will be reported to the Authority for the Financial Markets (AFM)).

Clients will only need to sign one agreement with an IB Broker to cover both Enriched and Delegated Transaction Reporting.

How to Sign Up for the Enriched and Delegated Transaction Reporting Service

Investment Firms (other than Omnibus Introducing Brokers) will be prompted to complete an electronic form in the Account Management system during which it will be possible to accept to use IB’s Enriched and Delegated Transaction Reporting Service.

Investment Firms that are Omnibus Introducing Brokers on the IB platform will not have the ability to activate the Enriched and Delegated Transaction Reporting.

Investment Firms that utilise IB’s Enriched and Delegated Transaction Reporting Service will need to sign the relevant legal agreement and provide the following information:

- Legal Entity Identifier (“LEI”). Clients that do not have an LEI, will be able to apply for one through an IB Broker;

- The citizenship(s) for each authorised trader and further information as required by the national client identifier requirements for the relevant country;

- Individuals or Algorithms that can be responsible for making the investment decision within the investment firm:

- Individual active traders who have been previously selected as possible investment decision makers within the firm. Only individuals that are authorised as traders on the account will be allowed;

- Algorithm identifiers provided for algorithms that the firm may use for making investment decisions. It is the client’s responsibility to determine and provide algorithm identifiers in compliance with the regulation.

How the New Requirements Will Affect the Account Management and the IB Order Entry System

Some of the information required for the submission of a transaction report may change on an order by order basis, and may require input of the person submitting the trade. Hence, IB has amended IB Account Management and the IB Order Entry System to allow traders to provide the necessary information.

Accounts that want to use IB’s Enriched and Delegated Transaction Reporting Service shall select the authorised traders and list the Algorithm IDs that may be responsible for making an investment decision.

The traders and algorithms listed in Account Management will be displayed in a new dropdown field of the IB Trader Workstation at the time of the order submission. This field will show the default value selected in Account Management of the account. The client will be able to change this by selecting another value present in the dropdown list.

The IB Trader Workstation will allow an authorised trader on the account for which the Enriched and Delegated Transaction Reporting was activated to select one person or algorithm as responsible for the investment decision within the firm with regard to the specific order submitted.

Note: For a listing of common MiFIR definitions and terms, see KB2980

THIS INFORMATION IS GUIDANCE FOR INTERACTIVE BROKERS CLEARED CLIENTS THAT ARE INVESTMENT FIRMS ONLY. THIS GUIDANCE DOES NOT APPLY TO EXECUTION ONLY ACCOUNTS.

NOTE: THE INFORMATION ABOVE IS NOT INTENDED TO BE A COMPREHENSIVE OR EXHAUSTIVE GUIDANCE AND IT IS NOT A DEFINITIVE INTERPRETATION OF THE REGULATION, BUT A SUMMARY OF MiFIR TRANSACTION REPORTING OBLIGATIONS.

Overview of MIFIR Transaction Reporting

Background

On 3 January 2018, a new Directive 2014/65/EC (“MiFID II”) and Regulation (EU) No 600/2014 (“MiFIR”) became effective, introducing significant changes to the transaction reporting (“MiFIR Transaction Reporting”) framework that was created in 2007 with the Markets in Financial Instrument Directive (“MiFID I”).

Interactive Brokers has implemented a new transaction reporting system that will enable clients that have direct reporting obligations under the new Regulation to comply with the new MiFIR requirements.

Scope of MiFIR Transaction Reporting Obligations

MiFIR Transaction Reporting applies to European Economic Area (“EEA”) and United Kingdom ("UK") Investment Firms ("Investment Firms") and also to Investment Firms that use a broker within the IB Group ("IB Group") to execute orders. As a client of an Investment Firm that uses the IB platform, you may be required to provide additional information to allow the proper transaction reports to be filed.

Investment Firms are obliged to report complete and accurate details of transactions executed in financial instruments covered by MiFIR to the relevant National Competent Authority (“NCA”) no later than the close of the next working day.

MiFIR has widened the scope of reportable financial instruments to cover those that are traded on EEA/UK Regulated Exchanges, Multilateral Trading Facilities (“MTFs”) and Organised Trading Facilities (“OTFs”). In addition to transactions executed on EEA/UK exchanges, MiFIR will capture Over the Counter (“OTC”) transactions and transactions of EEA/UK listed financial instruments that are executed on non-EEA/UK trading venues, e.g., a stock listed on the LSE traded on NYSE. (see financial instruments covered by MiFIR).

MiFIR Transaction Reporting Solutions for IB Clients that are EEA Investment Firms: Enriched and Delegated Transaction Reporting

IB clients that have confirmed that they are an Investment Firm subject to MiFIR transaction reporting obligations will be offered the option to delegate their reporting obligations to their relevant IB Broker.

Some transactions executed by these Investment Firms will be reported under “Enriched Reporting” obligations. For these trades the IB Broker will add details about the Investment Firm to its own reports, satisfying the reporting obligations of the Investment Firm. Other transactions will only be reported on behalf of Investment Firms on a delegated basis, as separate reports in addition to the IB Broker's own reports. Clients will only need to sign one agreement with their IB Broker to cover both types of reporting.

Information to Be Reported

The reporting fields increased from 23 under the MiFID I regime to 65 under MIFIR. The new information requirements now include, among other items:

- Detailed identification of the buyer and the seller for each transaction. In particular, the Regulation requires the provision of Legal Entity Identifiers (“LEI”) for legal entities and National Identifiers for natural persons (based on their countries of citizenship).

- Identification of the Decision Maker for the buyer and the seller when a third-party exercises discretion:

- A person other than the account holder on an individual or joint account, or a third-party entity.

- A third-party other than the authorised traders on the account for an organisation account (e.g. a Financial Advisor trading for its clients’ subaccounts).

This information is not required where the account holder is self-trading or where authorised traders are trading for their own organisation.

- Identification of the person or algorithm that is responsible at the reporting firm for making the investment decision or for the execution of a transaction. This information is required for EEA Investment Firms that use our reporting services.

- For Commodity Derivatives Transactions, an indication as to whether such Commodity Derivatives Transactions reduce risk in an objectively measurable way in accordance with Article 57 of MiFID II; This is applicable to organisation accounts only when the holder is a non-financial entity.

The new information affects Interactive Brokers clients in different ways depending on whether the client is an EEA Investment Firm, or an organisation/person that is not an Investment Firm, and also depending on whether the financial instruments being traded are received and/or transmitted by their IB Broker or another Interactive Brokers Group affiliate.

Implications for IB Clients that are not Subject to MiFIR Transaction Reporting Obligations

In order to meet its own reporting obligations, each IB Broker is obliged to identify and report its immediate client for each transaction executed. The reporting must contain the new client identifiers mandated by the Regulations.

Therefore, each IB Broker will need to obtain and report a client identifier for:

- The IB Broker's direct clients that hold an account to trade financial instruments received and/or transmitted by the IB Broker;

- Clients that are EEA Investment Firms and utilise the Interactive Brokers reporting services;

- Clients that are subaccounts of an EEA Investment Firm that uses the Interactive Brokers platform and utilises our reporting services.

See KB2976 for further details on the information required from account holders that are not directly subject to MiFIR.

Note: For a listing of common MiFIR definitions and terms, see KB2980

THIS INFORMATION IS GUIDANCE FOR INTERACTIVE BROKERS CLEARED CLIENTS ONLY. THIS GUIDANCE DOES NOT APPLY TO EXECUTION ONLY ACCOUNTS.

NOTE: THE INFORMATION ABOVE IS NOT INTENDED TO BE A COMPREHENSIVE OR EXHAUSTIVE GUIDANCE AND IT IS NOT A DEFINITIVE INTERPRETATION OF THE REGULATION, BUT A SUMMARY OF MiFIR TRANSACTION REPORTING OBLIGATIONS.

プロフェッショナルに分類されるお客様の注文の優先順位

2009年第四四半期、特定の米国オプション取引所(CBOEおよびISE)において、「プロフェッショナル」(ブローカーディーラーと同じような方法で取引を行うことのできる情報および/またはテクノロジーにアクセスのある個人や機関)とみなされる一般顧客からの注文を区別する規則が実施されました。これに基づき、ブローカーディーラーではなく、特定の月に自身の口座のために毎日平均で390以上の上場オプション注文(約定したかどうかに関わらず)をすべてのオプション取引所に発注する口座は、プロフェッショナルとみなされるようになります。CBOEおよびISEによる初回の実施以降、その他ほとんどの米国オプション取引所においても、「プロフェッショナル」注文の区別が実施されるようになりました。

プロフェッショナルのお客様の代理としてこれらオプション取引所に発注される注文は約定の優先を目的とし、ブローカーディーラーとして取り扱われ、リベート($0.65)から$1.12の手数料(オプションクラスにより)の範囲内で、コントラクトあたりの手数料の対象となります。

ブローカーは暦四半期ごとにレビューを行い、この期間中の1ヶ月間に390注文の枠を超え、次の暦四半期にプロフェッショナルとして指定されるべき顧客を割り出すことが義務付けられています。この確認の際、スプレッド注文はスプレッドの各レッグを個別の注文として数えるのではなく、スプレッド注文ごとにひとつの注文として数えます。これによる影響のあるお客様には弊社よりご連絡を差し上げます。またスマートルーティング注文は、新しく発生する取引所手数料を考慮の上でルーティング先を決定するようにデザインされています。

詳細は以下のリンクをご覧ください:

Common Reporting Standard (CRS)

The Common Reporting Standard (CRS), referred to as the Standard for Automatic Exchange of Financial Account Information (AEOI), calls on countries to obtain information from their financial institutions and exchange that information with other countries automatically on an annual basis. The CRS sets out the financial account information to be exchanged, the financial institutions required to report, the different types of accounts and taxpayers covered, as well as common due diligence procedures to be followed by financial institutions. For more information about CRS, please visit the OECD website.

Interactive Brokers entities comply with the requirements of CRS as implemented in the jurisdictions where they are located, and report account information to the applicable government authorities. Clients reported by Interactive Brokers under CRS will receive a CRS Client Report in the Client Portal shortly after the reporting deadlines specified below. The CRS Client Report provides an overview of the information that was reported by Interactive Brokers.

- What information is reported under CRS:

- Account number

- Name

- Address

- Tax ID Number

- Tax residency country

- Date of birth

- Year-end account balance

- Gross proceeds (all sales)

- Interest income

- Dividend income

- Other income

- When and where is the information reported:

- Interactive Brokers Australia Pty. Ltd. reports to the Australian Taxation Office (ATO) by July 31.

- Interactive Brokers Canada Inc. reports to the Canada Revenue Agency (CRA) by May 1.

- Interactive Brokers Central Europe Zrt. reports to the National Tax and Customs Administration of Hungary (NAV) by June 30.

- Interactive Brokers Hong Kong Limited reports to the Inland Revenue Department of Hong Kong SAR (IRD) by May 31.

- Interactive Brokers India Pvt. Ltd. reports to the Reserve Bank of India/Central Board of Direct Taxes (RBI/CBDT) by May 31.

- Interactive Brokers Ireland Limited reports to the Office of the Revenue Commissioners of Ireland by June 30.

- Interactive Brokers Securities Japan Inc. reports to the National Tax Agency of Japan (NTA) by April 30.

- Interactive Brokers Singapore Pte. Ltd. reports to the Inland Revenue Authority of Singapore (IRAS) by May 31.

- Interactive Brokers U.K. Limited reports to Her Majesty's Revenue and Customs of the United Kingdom (HMRC) by May 31.

- Additional Notes:

- Information relating to clients of Introducing Brokers is not reported by Interactive Brokers. Introducing Brokers are responsible for their own reporting under CRS.

- Accounts held by Interactive Brokers LLC are not reported under CRS as the United States has not signed the CRS.

SEC Tick Size Pilot Program

Background

Effective October 3, 2016, securities exchanges registered with the SEC will operate a Tick Size Pilot Program ("Pilot") intended to determine what impact, if any, widening of the minimum price change (i.e., tick size) will have on the trading, liquidity, and market quality of small cap stocks. The Pilot will last for 2 years and it will include approximately 1,200 securities having a market capitalization of $3 billion or less, average daily trading volume of 1 million shares or less, and a volume weighted average price of at least $2.00.

For purposes of the Pilot, these securities will be organized into groups that will determine a minimum tick size for both quote display and trading purposes. For example, Test Group 1 will consist of securities to be quoted in $0.05 increments and traded in $0.01 increments and Test Group 2 will include securities both quoted and traded in $0.05 increments. Test Group 3 will include also include securities both quoted and traded in $0.05 increments, but subject to Trade-at rules (more fully explained in the Rule). In addition, there will be a Control Group of securities that will continue to be quoted and traded in increments of $0.01. Details as to the Pilot and securities groupings are available on the FINRA website.

Impact to IB Account Holders

In order to comply with the SEC Rules associated with this Pilot, IB will change the way that it accepts orders in stocks included in the Pilot. Specifically, starting October 3, 2016 and in accordance with the phase-in schedule, IB will reject the following orders associated with Pilot Securities assigned to Test Groups:

- Limit orders having an explicit limit that is not entered in an increment of $0.05;

- Stop or Stop Limit orders having an explicit limit that is not entered in an increment of $0.05; and

- Orders having a price offset that is not entered in an increment of $0.05. Note that this does not apply to offsets which are percentage based and which therefore allow IB to calculate the permissible nickel increment

Clients submitting orders via the trading platform that are subject to rejection will receive the following pop-up message:

The following order types will continue to be accepted for Pilot Program Securities:

- Market orders;

- Benchmark orders having no impermissible offsets (e.g., VWAP, TVWAP);

- Pegged orders having no impermissible offsets ;

- Retail Price Improvement Orders routed to the NASDAQ-BX and NYSE as follows:

- Test Group 1 in .001

- Test Group 2 and 3 in .005

Other Items of Note

- GTC limit and stop orders entered prior to the start of the Pilot will be adjusted as allowed (e.g., a buy limit order at $5.01 will be adjusted to $5.00 and a sell limit at $5.01 adjusted to $5.05).

- Clients generating orders via third-party software (e.g., signal provider), order management system, computer to computer interfaces (CTCI) or through the API, should contact their vendor or review their systems to ensure that all systems recognize the Pilot restrictions.

- Incoming orders to IB that are marked with TSP exception codes from other Broker Dealers will not be acted upon by IB. For example, IB will not accept incoming orders marked with the Retail Investor Order or Trade-At ISO exception codes.

- The SEC order associated with this Pilot is available via the following link: https://www.sec.gov/rules/sro/nms/2015/34-74892-exa.pdf

- For a list of Pilot Program related FAQs, please see KB2750

Please note that the contents of this article are subject to revision as further regulatory guidance or changes to the Pilot Program are issued.

Amendment Requirements for SEC 13D and 13G Filers

Introduction

The following article is intended to provide an overview of U.S. Securities and Exchange Commission (“SEC”) Sections 13(d) and 13(g) Amendment Requirements. The overview is general in nature, and readers are encouraged to review the specific regulations and/or consult with a compliance professional to determine the applicability to their particular situation.

Amendment Requirements for 13D Filers

Rule 13d-2 of the Securities Exchange Act of 1934 (the "Act") requires you to promptly, within two business days, amend Schedule 13D whenever material changes in the information disclosed on a Schedule 13D occur. A material change includes any material increase or decrease in the percentage of the class of securities you are deemed to "beneficially own." For instance, if you manage more than 5% in the shares of an issuer and the percentage managed increases or decrease by more than 1% (whether through a transaction or other event), you must amend your 13D filing.

You must continue to make appropriate amendments so long as you continue to manage more than 5% of any class of an issuer's voting shares. If you fall below the 5% threshold, you must make one (final) amendment notifying the SEC of this.

There are also other circumstances that qualify as a material change requiring an amendment. For instance, if you acquire warrants that are not exercisable within 60 days, you may still need to amend Schedule 13D to revise your discussion of your plans concerning the acquisition of additional securities and related contracts, even if the amount of voting shares you manage has not yet changed.

Amendment Requirements for 13G Filers

Qualified institutional investors, including investment advisors registered with the SEC or a state, must amend their Schedule 13G within 10 days after the end of the first time their "beneficial ownership" exceeds 10% of the class of equity securities at month end.

After that, qualified institutional investors must amend their Schedule 13G within 10 days from when their "beneficial ownership" increases or decreases by more than 5% of the class of securities over the amount held at the previous month end.

Qualified institutional investors must also file a Schedule 13D within 10 calendar days after they cease being eligible to file a Schedule 13G rather than a Schedule 13D.

In addition, passive investors beneficially owning less than 20% of an equity security must amend their Schedule 13G promptly, within two business days, after acquiring beneficial ownership of more than 10% of the class of equity securities, and after that, within two business days of increasing or decreasing their ownership by more than 5%.

You must also file an annual amendment to the 13G if there have been any changes - immaterial or material - to your filed 13G. This must be done within 45 days of year end. You do not need to file an amendment if there have been no changes to the information filed or if the only change is to the percentage of securities owned resulting solely from a change in the number of shares outstanding.

Important Notes

· You should independently review your Schedule 13D and 13G filing obligations. There are many factual determinations that may impact whether you must make a filing or amend a prior filing, which Schedule you must file (or amend), and when you must make your filing.

· Interactive Brokers will provide you with notices, on a best efforts basis, only when you cross certain thresholds (5%, 10%, 20%) or a significant change in the percentage of shares you manage occurs. There may be other situations that give rise to the need to file or amend a Schedule 13D or Schedule 13G for which you will not receive an alert from Interactive Brokers.

· You should monitor holdings of specific classes of issuer equity securities in the accounts you manage to ensure compliance with your Schedule 13D or 13G filing and amendment obligations.

· Notices do not cover (nor will they take into account) certain securities not commonly traded through Interactive Brokers, namely equities in:

a. an insurance company that would have to be registered except for the exemption from registration in Section 12(g)(2)(G) of the Act;

b. a closed-end investment company registered under the Investment Company Act of 1940; or

c. a Native Corporation pursuant to Section 1639c(d)(6) of title 43.

You should therefore separately account for and analyze any holdings of such equity securities you may have to comply with Section 13(d) of the Act.

· Alerts sent are based exclusively on the beneficial ownership of relevant securities of the specific advisor identified. It does not account for any group aggregation rules that may apply when two or more persons agree to act together for the purpose of acquiring, holding, voting or disposing of the equity securities of an issuer.

· Alerts sent relate solely to holdings in accounts maintained at Interactive Brokers and not any accounts maintained elsewhere. But you should take any accounts you maintain elsewhere into consideration when determining whether you must file or amend a Schedule 13D or 13G and what information to include in those schedules.

· Alerts sent will not take into consideration your Schedule 13D or 13G filing obligations arising prior to the date of Interactive Broker's implementation of this alert program.

· The data we receive about US Micro-Cap securities—generally OTC listed stocks, as well as Nasdaq or NYSE American stocks with a market cap of less than $300MM that trade under $5 per share--from our data provider is not consistently reliable so we have removed those securities from this program. As a result, you will not receive Schedule 13D/13G alerts when you come close to crossing or cross thresholds triggering filing obligations regarding U.S. Micro-Cap securities. You should separately review your holdings in US Micro-Cap stocks to determine your related filing obligations for those holdings.

For Additional Information

For more information on Schedules 13D and 13G, please visit the SEC website at

http://www.sec.gov/answers/sched13.htm and

https://www.sec.gov/divisions/corpfin/guidance/reg13d-interp.htm